Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686564

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686564

Europe Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 100 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

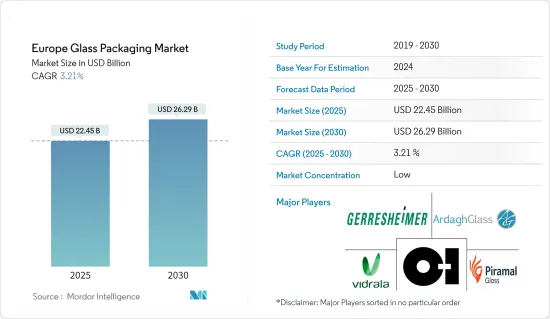

The Europe Glass Packaging Market size is estimated at USD 22.45 billion in 2025, and is expected to reach USD 26.29 billion by 2030, at a CAGR of 3.21% during the forecast period (2025-2030).

Key Highlights

- The European glass industry offers glass packaging products for the food and beverage, cosmetics, pharmacy, and perfumery industries. The compatibility of glass as a packaging material is a significant factor propelling the market's growth. The growing inclination toward using environment-friendly packaging material is another driver for the glass packaging market.

- Increasing consumer demand for safe and healthier packaging is helping glass packaging grow in different categories. Innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. Furthermore, factors such as the increasing demand for eco-friendly products and the rising demand from the food and beverage industry are stimulating the market's growth.

- The new rules for sustainability and recyclability in the region are also prominent factors pushing the growth of glass packaging. The European Union's Packaging and Packaging Waste Regulation (PPWR) proposals outline that each EU Member State could be required to reduce its packaging waste per capita by as much as 5% by 2030, 10% by 2035, and 15% by 2040, which is further driving the demand for recycled glass.

- Glass continues to be the reference packaging material for leading alcoholic beverages such as wines, spirits, and beer. It is gaining a prominent share in the food, water, and dairy industries. This is due to new consumption trends for local, organic, and natural food, the positive image of glass packaging, and strong consumer trust in glass as the preferred packaging for environmental, health, and taste preservation reasons.

- One of the primary challenges facing the glass packaging industry in the region is the surge in energy prices, which is hindering market growth. The energy-intensive nature of glass production makes it difficult for manufacturers to absorb these rising costs. Additionally, the ongoing conflict between Russia and Ukraine has intensified the situation for glass packaging producers in the United Kingdom, leading to soaring energy expenses. As a result, these escalating energy prices have driven up production costs, thereby increasing the price of glass.

- Furthermore, several wine manufacturers have switched to plastic as an alternative due to disrupted supply chains and inactive furnaces. For instance, the trend of alcoholic beverage companies in the United Kingdom replacing glass packaging with bottles made of paper has picked up pace. Recently, Aldi, a leading retailer, recently introduced wine in bottles made from 94% recycled paperboard, featuring a food-grade pouch.

Europe Glass Packaging Market Trends

Beverages Segment to Hold a Significant Market Share

- The European beverages market is poised for robust growth and is expected to secure a significant market share. As demand for sustainable and convenient beverage packaging increases, industry experts anticipate an expansion in the European beverages market. Continuous advancements in Europe's packaging production and manufacturing processes are enhancing the industry's environmental friendliness. Packaging companies are increasingly focusing on sustainable practices by producing products from recycled materials, which consume less energy and water while reducing carbon emissions.

- Creating innovative, lightweight products with appealing designs and appealing color schemes at lower production costs has continued to be a key growth facilitator. Prominent beverage companies are also raising the adoption of glass packaging, which adds to the beverage segment's share in Europe. For instance, in September 2023, Coca-Cola HBC established a new, high-speed returnable glass bottling line (RGB) at the Edelstal plant in Austria. An investment of EUR 12 million (USD 12.99 million) from Coca-Cola HBC was supported by a grant of EUR 4 million (USD 4.33 million) from the Austrian government as part of its fund for beverage companies and retailers to enable an actual circular economy for packaging.

- The growth in the production of alcoholic beverages, such as wine, along with a rise in exports, is further boosting demand for glass packaging. For instance, according to the European Commission, wine production in the European Union reached 159 million hectoliters in 2023 from 152.9 million hectoliters in 2022. As per the UN Comtrade, France and Italy were the largest exporters of wine in Europe in 2023, with values of USD 12,789.4 million and USD 8,403.2 million, respectively.

- In response to the escalating plastic pollution, beverage manufacturers in the region are increasingly transitioning to refillable glass bottles due to the rapidly growing demand for beverage products. For instance, in August 2023, to fulfill its commitment to reducing plastic pollution, Coca-Cola launched a new system for delivering, collecting, and reusing glass bottles of Coke Zero directly with customers. The beverage is being distributed to homes in the United Kingdom in partnership with delivery service Milk & More. The trial began on June 5, 2023, and was to continue throughout the summer in south London and central southern England.

Poland Expected to Witness Significant Market Growth

- Poland is anticipated to experience the most significant growth in packaging in Eastern Europe during the forecast period. The development of glass bottles is expected to be fueled by bottled water, juice, energy drinks, and premium beverages.

- The rising mergers and acquisitions in the Polish glass packaging market indicate a consolidation trend among companies to enhance competitiveness and market share. This consolidation is likely to lead to increased efficiency, innovation, and potential pricing dynamics, shaping the landscape of the Polish glass packaging market. For instance, in April 2024, CANPACK Group and BA Glass announced the finalization of the sale of CANPACK's Glass operations in Poland to BA Glass. Consequently, the glass plant in Orzesze was transferred to BA Glass and became part of its operations in Poland.

- The Polish glass industry has diversified its manufacturing capabilities. In the Polish glass industry, significant amounts of glass sand are used to produce container glass. To initiate the country's transition to such a system, the Polish government began preparing the introduction of a mandatory deposit for glass and plastic bottles in 2022. The deposit system included reusable glass bottles of up to 1.5 liters. Poland is expected to remain a strong performer in the beverages industry, where glass bottles may be the primary packaging material, with a small share held by other packaging types.

- Companies operating in the industry are focused on innovating new solutions through expansions in the country. For instance, in January 2023, Ardagh Glass Packaging designed a sustainable glass furnace in Poland. The new furnace can gain and maintain lower emission levels while gas, electricity, and water usage will be minimized via multiple sustainable methods. According to the firm, gas, electricity, and water usage will be minimized via heat recovery, turbo compressors, water recovery, and a closed-loop cooling procedure. The glass manufacturer stated that reducing emissions and enhancing the effect on the environment is a crucial goal for the glass industry. Such technological innovations by major companies are expected to fuel market growth during the forecast period.

- Moreover, the country has witnessed significant growth in the export of beverages and other products that use glass packaging. For instance, according to UN Comtrade, in 2023, the value generated from the export of beverages, spirits, and vinegar in Poland remained nearly unchanged at around EUR 1.6 billion. This growth in exports is anticipated to further create demand for glass packaging products in Poland.

Europe Glass Packaging Industry Overview

The European glass packaging market is highly competitive, with many regional players holding significant shares in the market. These companies are leveraging strategic initiatives to increase market share and profitability.

- In July 2024, Verallia, a prominent producer of glass packaging for food and beverage products, acquired Vidrala's glass business in Italy. The transaction, valued at an enterprise value of EUR 230 million (USD 248.9 million), included a Corsico-based plant. This facility, equipped with two recently renovated furnaces, features modern production capabilities with an annual capacity of 225 kilotons. It actively operates in the food, beer, and spirits markets.

- In May 2024, Gerresheimer Glas, an indirect subsidiary of Gerresheimer AG, signed an agreement to acquire Blitz LuxCo Sarl, the holding company of Bormioli Pharma Group. This acquisition enhances Gerresheimer's European footprint with additional production sites, particularly in Southern Europe. It also strengthens its market position as a leading full-service provider and global partner for the pharmaceutical and biotech industries.

- In September 2023, O-I launched an advanced, embossed, customized packaging offering. With its O-I: Expressions Signature, O-I became the first glass manufacturer to produce decorated glass bottles using variable data printing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 52667

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of Microeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Shift Toward Sustainable Packaging Due to Stringent Regulations

- 5.1.2 Growing Adoption of Premium Glass Packaging in End-user Industries, such as Beverages and Cosmetics

- 5.2 Market Challenge

- 5.2.1 Alternative Forms of Packaging Challenging the Market's Growth

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bottles

- 6.1.2 Ampoules

- 6.1.3 Vials

- 6.1.4 Syringes

- 6.1.5 Jars

- 6.2 By End-user Industry

- 6.2.1 Beverage

- 6.2.1.1 Liquor

- 6.2.1.2 Beer

- 6.2.1.3 Soft Drinks

- 6.2.1.4 Other Beverages

- 6.2.2 Food

- 6.2.3 Cosmetics

- 6.2.4 Pharmaceuticals

- 6.2.1 Beverage

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Poland

- 6.3.7 Netherlands

- 6.3.8 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Owens-Illinois Inc.

- 7.1.2 Origin Pharma Packaging

- 7.1.3 Verallia

- 7.1.4 Vidrala SA

- 7.1.5 Vetropack Holding Ltd

- 7.1.6 Vitro SAB de CV

- 7.1.7 APG Europe

- 7.1.8 Saverglass Group

- 7.1.9 Wiegand-Glass GmBH

- 7.1.10 Crestani SRL

- 7.1.11 Verescene France SASU

- 7.1.12 Stolzle Glass Group

- 7.1.13 Ardagh Packaging Group PLC

- 7.1.14 SGD Pharma SA

- 7.1.15 Beatson Clark PLC

- 7.1.16 Stevanato Group

- 7.1.17 Gerresheimer AG

- 7.1.18 BA Vidro SA (BA Glass BV)

- 7.1.19 Glassworks International Limited

- 7.1.20 Gaasch Packaging (UK) Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.