PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432785

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432785

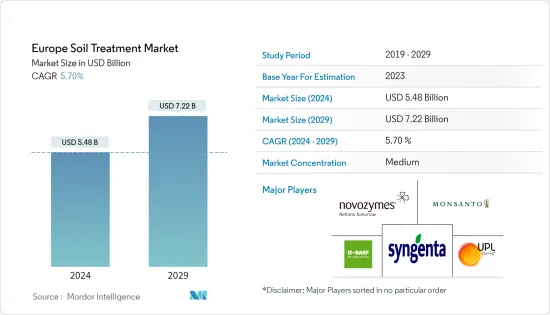

Europe Soil Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Europe Soil Treatment Market size is estimated at USD 5.48 billion in 2024, and is expected to reach USD 7.22 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

Key Highlights

- The demand for high-quality food, the export-based agriculture sector, and the highly mechanized agriculture propels farmers to opt for soil treatment products in order to maintain soil conditions. Stringent regulatory structures pertaining to the environment may hinder market growth in Europe.

- The market studied is dominated by countries, like Spain, the United Kingdom, and France. Countries, like Germany and Italy, would grow effectively as they embrace the application of soil treatment products in their fields.

Europe Soil Treatment Market Trends

International Demand for Agricultural Produce

The region exports a good amount of cereals to international markets and therefore there is a growing need to address soil nutrition owing to excessive cultivation. Moreover, environmental concerns and greater adaptability of organic farming may help the biological soil treatment market to grow. As France dominates the export market for cereals, the country is highly concerned about correcting its soil quality levels. Therefore, to address this, the country has been depending on soil treatment products. According to the data by ITC Trade, France exported USD 6,233,259 thousand of cereals in 2016 which increased to USD 7,415,294 thousand in 2019 to countries, such as, Belgium, Algeria, the Netherlands, Spain, and Germany. Thus, to fulfill the demand for cereals in the region and within the country itself, it is necessary to maintain the soil quality index in order to produce and export quality cereals. This, in turn, may drive the soil treatment market over the forecast period.

Spain Dominates the Market

Spain covers a major share of the soil treatment market followed by the United Kingdom, France, and Italy. Various organizations, such as SENGEOS in Spain, a consultancy firm specialized in providing EHS & Soil service and LITOCLEAN, an expert company in the execution of soil investigation and decontamination, have initiated projects that aim at improvising soil health through GIS(geographical information systems) and building Soil Information Systems (SIS) in Spain. Moreover, in 2018, Agricultural Industries Confederation has formed initiative through voluntary actions to approach growers to pass on the importance of soil health soil treatment chemicals under agricultural management. France, which is one of the largest agricultural countries and the biggest producer of agricultural goods in Europe, has been consuming a lot of soil treatment products, making itself one of the major consumers of soil treatment chemicals. Therefore, the market for soil treatment products is fairly distributed across European countries.

Europe Soil Treatment Industry Overview

In the European soil treatment market, the companies not only compete on the basis of product quality or product promotion but also focus on strategic moves to acquire greater market share. The major players are BASF SE, Syngenta, Amvac Chemical Corporation, Bayer AG, and Arysta Lifescience Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Market Definition

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Technnology

- 5.1.1 Physiochemical Treatment

- 5.1.2 Biological Treatment

- 5.1.3 Thermal Treatment

- 5.2 By Type

- 5.2.1 Organic Amendments

- 5.2.2 pH Adjusters

- 5.2.3 Soil Protection

- 5.3 Geography

- 5.3.1 Europe

- 5.3.1.1 Spain

- 5.3.1.2 United Kingdom

- 5.3.1.3 Germany

- 5.3.1.4 France

- 5.3.1.5 Italy

- 5.3.1.6 Rest of Europe

- 5.3.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Monsanto

- 6.3.3 Novozymes

- 6.3.4 Syngenta AG

- 6.3.5 UPL

- 6.3.6 Biosoil EU BV

- 6.3.7 Savaterra

- 6.3.8 Fertagon

7 MARKET OPPORTUNITIES AND FUTURE TRENDS