Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687193

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687193

Clinical Data Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 120 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

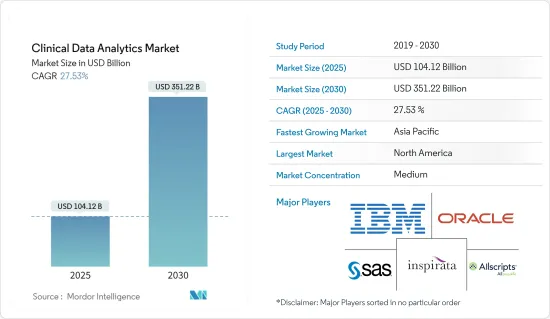

The Clinical Data Analytics Market size is estimated at USD 104.12 billion in 2025, and is expected to reach USD 351.22 billion by 2030, at a CAGR of 27.53% during the forecast period (2025-2030).

Key Highlights

- Clinical data analytics within the healthcare industry is crucial for the treatment and prediction of illnesses, enhancing the level of care, and reducing avoidable deaths caused by the oversight of certain chronic conditions. Information provided by users, measurements from task-based devices, and data from passive sensing all contribute to the gathering of data utilized for clinical data analysis, ultimately aiding in the expansion of the market.

- Clinical data analytics play a vital role in clinical research, involving the storage, collection, and analysis of data to enhance its utilization. This enables healthcare facilities to deliver personalized and preventive care efficiently. The advancements in clinical, healthcare, and data analytics technologies have significantly impacted the industry. Moreover, the ever-changing regulations in the industry contribute to market dynamics, pushing for cost reduction in drug development and the need for innovative therapies.

- Clinical data analysts are also tasked with the development and management of healthcare databases, as well as providing training for software and technical programs. They design secure systems for data storage and keep abreast of regulations to ensure compliance with ethical standards. Clinical data analysts play a key role in ensuring the smooth operation of networks and overseeing necessary upgrades. The growing demand in the healthcare industry is anticipated to boost market demand.

- Over the last few years, there has been a growing emphasis on managing diabetes. A recent study by Rensselaer Polytechnic Institute utilized artificial intelligence (AI) and big data analytics to analyze data from numerous continuous glucose monitors and insulin pumps. The findings from this research can help enhance the algorithms governing these devices, ultimately benefiting individuals with type 1 diabetes. By incorporating technology into diabetes management, there is a possibility of delivering superior diabetes care, reducing expenses and administrative complexities, and empowering individuals with diabetes and their caregivers.

- The increasing need for customized medical treatments and diagnostic tests has resulted in a significant rise in clinical trials. These trials produce large amounts of data, requiring sophisticated clinical data analytics solutions to extract valuable insights. Additionally, factors such as government support, global investments, and advancements in the healthcare industry by major players across various countries like India, Japan, the United States, and the EU States will create numerous opportunities for market growth.

- Anticipated advancements from industry vendors are projected to boost the market's growth prospects in the upcoming years. In June 2024, Medidata, a brand under Dassault Systemes and a prominent supplier of clinical trial solutions to the life sciences industry, introduced Medidata Clinical Data Studio. This innovative platform offers a cohesive interface that unleashes the full potential of clinical research data. Through this cutting-edge technology, stakeholders are empowered with enhanced data quality control and the capability to expedite the delivery of safer trials to patients.

- As a result, the increasing quantity of clinical trials is driving the need for more sophisticated clinical trial solutions. Nonetheless, a prevalent issue faced by data analysts is poor data quality, which can impede analysis and decision-making, potentially impacting market growth.

- The COVID-19 pandemic accelerated the integration of digitalization into the market, leading to an increased emphasis on remote patient care, consultations, and diagnoses. Additionally, the pandemic caused a substantial surge in the market as a result of digitalization. However, the growing prevalence of cardiac diseases during the pandemic, influenced by various external factors, is also expected to fuel the growth of the clinical data analytics market in the forecast period.

Clinical Data Analytics Market Trends

Cloud Deployment Model to Hold a Dominant Position in the Market

- The rising utilization of electronic records in numerous healthcare facilities has led to the increased utilization of cloud-based solutions due to their primary benefits, including their ability to allow for the storage and convenient utilization and examination of patient records, data, and medical history. Doctors prefer cloud solutions as they facilitate secure communication between patients and other hospital staff, and these solutions are compatible with mobile devices, web platforms, and data retrieval from various sites.

- Additionally, cloud-based solutions provide remote access, promoting collaboration among healthcare researchers across different geographic areas. This access helps streamline decision-making and patient care schedules. Moreover, cloud platforms enable the incorporation of advanced analytics and machine learning algorithms, enhancing the depth and precision of clinical data analysis and for extensive clinical research. The increasing recognition of these benefits is anticipated to drive market growth over the coming years.

- By utilizing knowledge gained from cutting-edge analytics tools in the cloud, leaders can enhance their strategic decision-making, streamline resource distribution, and boost operational effectiveness. The use of healthcare analytics enables the detection of patterns and trends in patient information, resulting in improved patient engagement and results. Through predictive and prescriptive analytics on cloud platforms, healthcare professionals can predict potential health concerns, tailor treatment strategies, and take proactive measures. This approach also supports the advancement of preventive and personalized healthcare practices.

- Healthcare institutions are increasingly turning to cloud-based solutions, propelled by the widespread adoption of electronic records. These solutions offer an intuitive advantage, simplifying the archiving, retrieval, and analysis of patient data and medical histories. Cloud platforms, compatible with mobile devices and accessible from diverse locations, have become the favored choice for physicians. Moreover, the cloud's versatility extends beyond local data, enabling seamless collaboration across global data repositories.

- As genomic medicine progresses, the influx of patient data is outpacing the capacity of traditional on-premise data warehouses. To cope with this data deluge, health systems are turning to cloud-based solutions. This shift is crucial as R&D investments and government research budgets rise, heightening the need for data solutions that offer not just power but also precision in their insights. Companies are thus using big data to achieve this accuracy; however, this necessitates advanced computing power, which can be accessed via the cloud.

- For instance, in January 2023, Saama, a leading provider of AI- and ML-driven solutions for expediting clinical development and commercialization, unveiled its latest offering: a unified platform of SaaS-based products. This launch complements Saama's established lineup of tailored solutions and services. By leveraging Saama's cutting-edge tools, sponsors and CROs in clinical trials can slash query identification and generation times by a staggering 90% per query. Additionally, they stand to achieve up to a 50% reduction in studying data transformation timelines, cut the time from data entry to analysis by over 35%, and other benefits.

North America Expected to Contribute a Significant Market Share

- During the forecast period, North America's market is poised for significant growth, with the United States leading the charge. This surge in the US market can be attributed to the implementation of federal healthcare mandates aimed at curbing escalating costs, a push for wider adoption of electronic health records (EHR), and an emphasis on initiatives such as personalized medicine, value-based reimbursements, and population health management.

- The region's healthcare industry has witnessed a decrease in drug errors, improvement in population health, and cost savings for numerous organizations due to the implementation of clinical analytics. The market is experiencing a surge in demand driven by the need for high-quality services and reduced healthcare expenses. With the increasing emphasis on security in digital platforms and channels, the utilization of statistical data is expected to remain high, supported by significant investments in cybersecurity and healthcare by key market players in the region.

- Moreover, the United States is expected to dominate the market in the region due to its extensive healthcare industry and growing clinical research activities. The US government has introduced new rules for Medicare, which will impose financial penalties on hospitals and doctors who do not use EHRs. Despite the country's reputation for pioneering advanced medical technologies, there is a need for healthcare providers to transition from paper records to electronic ones more quickly. These measures are aimed at maximizing the effectiveness of EHRs. The implementation of these regulations is expected to increase the demand for clinical data analytics solutions in the region.

- In June 2024, IQVIA unveiled One Home for Sites, an advanced technology platform that serves as a centralized hub for clinical research sites. This platform offers a single sign-on and dashboard, simplifying the management of key systems and tasks necessary for conducting clinical trials. By reducing the complexity of managing multiple usernames and passwords across various software applications, One Home for Sites aims to improve operational efficiency and productivity. These developments are poised to drive growth and create new market opportunities in the region.

- Moreover, the clinical data analytics industry has grown in recent years due to the rising utilization of clinical data analytics solutions in healthcare facilities to handle large volumes of COVID-19 data. Additionally, healthcare organizations are leveraging technological progress, such as clinical trial management systems, clinical decision support systems, and data mining. This trend is driven by the swift uptake of cutting-edge real-time, patient-focused record technologies and the significant presence of major clinical data analytics solutions providers, such as IBM and IQVIA, in the market.

- The region's robust healthcare infrastructure and widespread adoption of advanced technologies are anticipated to drive substantial market growth during the forecast period. Healthcare institutions in the area are increasingly turning to analytics solutions due to the growing prevalence of chronic diseases and an aging population. According to the National Health Council, chronic diseases, which are generally incurable and ongoing, impact around 133 million Americans, making up over 40% of the total population. Additionally, the market is bolstered by the presence of key industry players.

Clinical Data Analytics Industry Overview

The clinical data analytics market is semi-consolidated and has gained a competitive edge in recent years. In terms of market share, a few significant players currently dominate the market. These market leaders are focusing on expanding their customer base in foreign countries. These businesses leverage strategic collaborative initiatives to increase their market share and profitability.

- July 2024 - EQT announced that the EQT Healthcare Growth Strategy and the EQT Growth Fund had reached an agreement to purchase a controlling interest in CluePoints. CluePoints is a cloud-based software platform for Risk-Based Quality Management ("RBQM") and data quality oversight in clinical trials, aimed at facilitating safer and more effective processes and enhancing data integrity and risk compliance. This recent investment arrives as CluePoints experiences rapid growth, supported by the rising utilization of RBQM software in nearly all clinical trial stages.

- October 2023 - Holmusk and Veradigm announced a new phase of strategic investment to fuel innovation and close the evidence gap in behavioral health. The collaboration seeks to draw on the strengths of each company to fuel innovation in behavioral health and create the evidence needed to move the field forward. In this new phase of the collaboration, cohorts of millions of behavioral health patients and related de-identified clinical data from Veradigm will be added to Holmusk's NeuroBlu Database, a leading source for real-world data that shows how behavioral health care is delivered.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 56259

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Focus on Population Health Management

- 5.1.2 Government Healthcare Policies

- 5.1.3 Clinical Data Analytics Enabling Personalized Patient Care

- 5.1.4 Growing Need to Contain Healthcare Expenditure

- 5.2 Market Challenges

- 5.2.1 Lack of Infrastructural Facilities in Various Government and Private Hospitals

- 5.2.2 Low Internet Penetration in Emerging Economies

- 5.3 Market Opportunities

- 5.3.1 Increasing Adoption of Electronic Data Recording Systems

- 5.4 Research Activity by Therapeutic Area

- 5.4.1 Cardiovascular

- 5.4.2 Central Nervous System (CNS)

- 5.4.3 Oncology

- 5.4.4 Infectious Diseases

- 5.4.5 Other Therapeutic Areas

- 5.5 Industry Value Chain Analysis

- 5.6 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 By Deployment Model

- 6.1.1 Cloud

- 6.1.2 On-premise

- 6.2 By Application

- 6.2.1 Quality Improvement and Clinical Benchmarking

- 6.2.2 Clinical Decision Support

- 6.2.3 Regulatory Reporting and Compliance

- 6.2.4 Comparative Analytics/Comparative Effectiveness

- 6.2.5 Precision Health

- 6.3 By End-user Vertical

- 6.3.1 Payers

- 6.3.2 Providers

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United KIngdom

- 6.4.2.3 Italy

- 6.4.2.4 France

- 6.4.2.5 Spain

- 6.4.2.6 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.3.4 South Korea

- 6.4.3.5 Australia

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 GCC

- 6.4.5.2 South Africa

- 6.4.5.3 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Allscripts Health Solution

- 7.1.2 Inspirata Inc.

- 7.1.3 CareEvolution Inc.

- 7.1.4 SAS Institute Inc.

- 7.1.5 Health Catalyst Inc.

- 7.1.6 IBM Corporation

- 7.1.7 Koninklijke Philips NV

- 7.1.8 McKesson Corporation

- 7.1.9 Optum Inc.

- 7.1.10 Oracle Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.