PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642093

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642093

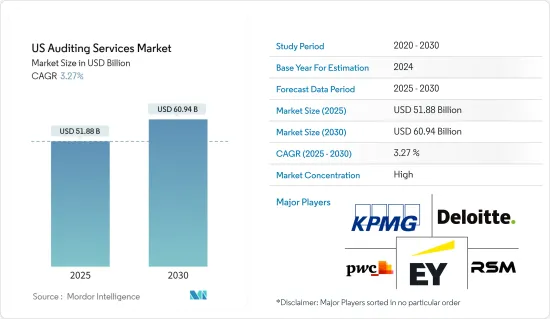

US Auditing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The US Auditing Services Market size is estimated at USD 51.88 billion in 2025, and is expected to reach USD 60.94 billion by 2030, at a CAGR of 3.27% during the forecast period (2025-2030).

In recent decades, market consolidation has become a prominent trend, as auditing firms strategically acquire global accounting entities to broaden their service offerings and improve existing auditing services. This trend has led to a notable decrease in the number of global audit firms, consolidating major players into what is commonly referred to as the Big Four.

In the United States, this consolidation is particularly pronounced, where the Big Four accounting firms collectively audit nearly 97% of the total US S&P 500 market capitalization. The concentration is even more pronounced in specific industries, with one or two firms dominating certain sectors. For instance, the leading auditing service provider in the US telecommunications services sector encompasses nearly 92% of the S&P 500 market capitalization. Similar scenarios exist in industries such as energy, materials, and information technology, where the top two service providers control at least 75% of the S&P 500 market capitalization. Recent market drivers and opportunities encompass technological advancements, regulatory changes, and increasing demand for specialized audit services, driving the evolution of the US Auditing Services Market.

US Audit Market Trends

Declining Quality of Auditing from the Big 4

Considering the high concentration of the audit service market in the US, investors raised issues with the probability of a lower concentration of audits, which can also result in lesser protection for investors. A ban or suspension on any of the firms could include a catastrophic effect on the market as it would create a huge void that the rest of the markets cannot handle. And considering the same, these firms are reasonably assured about their position from audit regulators. Auditors are fast becoming complacent and are already eliminating certain audit procedures to reduce costs, taking on riskier clients, consenting to the demands of management, and aggressively expanding their riskier non-audit service line under the trusted audit firm brand, which would only increase the auditing standards.

The major factor for this can be how the Big 4 firms and their subsidiaries work. These subsidiaries act as legally distinct business affiliates more than subsidiaries of the global networks, which share the same ethos. Unless regulators take firm action, the quality of the audits is expected to decline further.

Big 4 firms Increase the Auditing Fee as the Tenure Grows

One significant evidence of why the big four firms are monetizing on the lack of competition or regulation is the increased auditing fees for tenured companies. While convention dictates that firms should charge less to their tenured clients who provided the business for a long time, the same doesn't hold for the big four firms in the US.

The justification firms give for such a hike is the increasing workload as the business grows, and the changing corporate structure resulted in its toll on auditing. However, the same doesn't hold for non-big 4 firms whose fees remain flat and marginally decreasing. Big 4 firms, on average, charge their customers 32% higher fees in the 14th year compared to a 6% decline in fees by non-big 4 auditing firms in the same period. The fee increase is a direct consequence of these companies' power in the auditing space. Considering the list of bans imposed in other countries, it is only a matter of time before these companies are asked to follow stricter regulations.

US Audit Industry Overview

A complete background analysis of the US audit services market, including the assessment of the economy and contribution of the sectors in the economy, market overview, market size estimation for key segments and emerging trends in the market segments, market dynamics and insights, along with key health statistics, is covered in the report. Players including Deloitte, KPMG, EY, PwC, and RSM US, among others have been profiled in the report.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights on Technological Advancements in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Internal Audit

- 5.1.2 External Audit

- 5.2 Service line

- 5.2.1 Operational Audits

- 5.2.2 Financial Audits

- 5.2.3 Advisory and Consulting

- 5.2.4 Investigation Audit

- 5.2.5 Information System Audit

- 5.2.6 Compliance Audit

- 5.2.7 Other

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Deloitte

- 6.2.2 EY

- 6.2.3 KPMG

- 6.2.4 PwC

- 6.2.5 RSM US

- 6.2.6 Grant Thornton LLP

- 6.2.7 A.T Kearney

- 6.2.8 BDO USA

- 6.2.9 CBIZ & Mayer Hoffman McCann

- 6.2.10 Crowe Horwath*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS