PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437387

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437387

India Diabetes Care Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

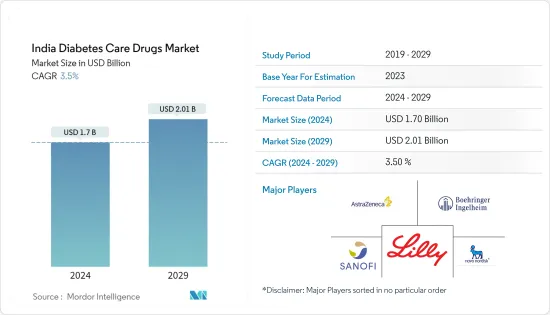

The India Diabetes Care Drugs Market size is estimated at USD 1.7 billion in 2024, and is expected to reach USD 2.01 billion by 2029, growing at a CAGR of 3.5% during the forecast period (2024-2029).

In India, COVID-19 infections, which began around two years ago, have contributed to a nearly 25% increase. With Over 80 million diabetics, India is commonly referred to be the diabetes capital. COVID, a viral infection that generates a variety of inflammatory reactions, has been linked to several recurring and new health problems, including hypoxia, weakness, weight loss, hair loss, myocarditis, and thyroid problems. However, diabetes is said to be one of the most prevalent side effects of the infectious condition. According to Dr. Anoop Misra, a senior endocrinologist from Delhi, the prevalence of new-onset diabetes and thyroid dysfunction in Covid-19 patients has been observed across countries. He speculated that the explanations may be "severe impacts of cytokine surge" (a strong immunological reaction reported in certain Covid patients) and/or "some unfurling of autoimmunity" (when the body's immune system mistakes and targets the body's own tissues and organs).

Insulin has a substantial market share in the pharmaceutical industry. Insulin is used by around 100 million people globally, including all patients with Type 1 diabetes and 10% to 25% of people with Type 2 diabetes. Insulin manufacturing is highly complicated, with just a few insulin producers on the market. As a result, there is tremendous competition among these companies, which are always seeking to meet patient requests by offering the highest-quality insulin.

India Diabetes Care Drugs Market Trends

Oral-Anti Diabetes Drugs Segment is Having the Highest Market Share in the Current Year

The Oral-Anti Diabetes Drugs segment is expected to increase with a CAGR of over 3% during the forecast period, mainly due to the demand from the diabetes population, which was more than 85 million by the end of the current year.

Diabetes is a disorder for which there is no cure. With the present arsenal, it is an illness that impacts us for the rest of patients' lives. Individuals face a significant financial, social, and emotional burden beginning at 30 and continuing into their 90s. According to all current guidelines in India, metformin should be the first option among oral antidiabetic medicines at the outset of diabetes.

However, a review of the literature from around the world finds that metformin is used in various ways in the early stages of diabetes. Sharma et al. found a changing trend in 55% of metformin-treated individuals. The fraction of individuals on metformin remains stable from 0 to 20 years of diabetes. The proportion of sulfonylurea and dipeptidyl peptidase-4 inhibitors (DPP4i) increases from 23.12% and 22.5% in 0-5 years of diabetes to 70.77% and 60% in 10-15 years of diabetes. Following that, the proportion of sulfonylurea and DPP4i remains constant. As the use of sulfonylureas and DPP4i reaches a plateau, the use of insulin and sodium/glucose cotransporter 2 inhibitors increases. From 5 to 10 years of diabetes duration to 20+ years of diabetes duration, the proportion of alpha-glucosidase inhibitors increases somewhat. Thiazolidinediones and glucagon-like peptide-1 receptor agonists have a small proportion in contemporary practice and the given patient population.

Through the Indian government's encouragement, the usage of drugs increased over the forecast period.

The rising prevalence of diabetes in India is boosting the country's diabetes drugs market.

In India, it is anticipated to exceed 134 million by 2045. Approximately 57% of these people are still undiagnosed. Type 2 diabetes accounts for most behavioral behaviors and can result in multiorgan problems, roughly classified as microvascular and macrovascular complications. These problems are a key cause of increased early morbidity and death in diabetics, resulting in decreased life expectancy and a huge financial load on the Indian healthcare system. Diabetes risk factors include race, age, obesity, physical inactivity, a poor diet, behavioral behaviors, genetics, and family history. Controlling blood sugar, blood pressure, and lipid levels can help behavioral behaviors void or postpone the onset of diabetic complications. Diabetes prevention and management pose a significant challenge in India due to several issues and barriers, including a lack of a multisectoral approach, surveillance data, awareness of diabetes, its risk factors and complications, access to health care settings, access to affordable medicines, and so on.

People living in cities and metropolitan regions in India are more likely than ever before to get diabetes, according to the 2021 assessment. This is due, in part, to cities encouraging a lifestyle that might raise a person's BMI (BMI). A greater BMI is a risk factor for diabetes. Rural India is also seeing an increase in type 2 diabetes occurrences. Diabetes is perceived as a "new" ailment in rural places, and public understanding of the condition is poor.

Diabetes cases are several as the country undergoes urbanization, so more people are migrating to larger cities for work. Sedentary living habits are promoted in urbanized regions and cities, which is a risk factor for rising obesity and diabetes. South Asian ancestors' bodies respond differently to sugary and fatty diets than European ancestors' bodies, and as processed Western foods become more popular in India, so does the risk of diabetes.

Thus, the above factors are expected to drive the market growth over the forecast period.

India Diabetes Care Drugs Industry Overview

The India Diabetes Drugs Market is moderately fragmented, with few significant and generic players. The insulin drugs and Sglt-2 drugs market are dominated by a few major players, like Novo-Nordisk, Sanofi, AstraZeneca, and Bristol Myers Squibb. The market for oral drugs, like Sulfonylureas and Meglitinides, comprises more generic players. The intensity of competition among the players is high, as each player is striving to develop new drugs and offer them at competitive pricing. Furthermore, to increase their market shares, players are tapping into new markets, especially emerging economies where the demand is very high compared to the supply.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Oral Anti-diabetic drugs

- 5.1.1 Biguanides

- 5.1.1.1 Metformin

- 5.1.2 Alpha-Glucosidase Inhibitors

- 5.1.2.1 Alpha-Glucosidase Inhibitors

- 5.1.3 Dopamine D2 receptor agonist

- 5.1.3.1 Bromocriptin

- 5.1.4 SGLT-2 inhibitors

- 5.1.4.1 Invokana (Canagliflozin)

- 5.1.4.2 Jardiance (Empagliflozin)

- 5.1.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.1.4.4 Suglat (Ipragliflozin)

- 5.1.5 DPP-4 inhibitors

- 5.1.5.1 Onglyza (Saxagliptin)

- 5.1.5.2 Tradjenta (Linagliptin)

- 5.1.5.3 Vipidia/Nesina(Alogliptin)

- 5.1.5.4 Galvus (Vildagliptin)

- 5.1.6 Sulfonylureas

- 5.1.6.1 Sulfonylureas

- 5.1.7 Meglitinides

- 5.1.7.1 Meglitinides

- 5.1.1 Biguanides

- 5.2 Insulins

- 5.2.1 Basal or Long Acting Insulins

- 5.2.1.1 Lantus (Insulin Glargine)

- 5.2.1.2 Levemir (Insulin Detemir)

- 5.2.1.3 Toujeo (Insulin Glargine)

- 5.2.1.4 Tresiba (Insulin Degludec)

- 5.2.1.5 Basaglar (Insulin Glargine)

- 5.2.2 Bolus or Fast Acting Insulins

- 5.2.2.1 NovoRapid/Novolog (Insulin Aspart)

- 5.2.2.2 Humalog (Insulin Lispro)

- 5.2.2.3 Apidra (Insulin Glulisine)

- 5.2.3 Traditional Human Insulins

- 5.2.3.1 Novolin/Actrapid/Insulatard

- 5.2.3.2 Humulin

- 5.2.3.3 Insuman

- 5.2.4 Biosimilar Insulins

- 5.2.4.1 Insulin Glargine Biosimilars

- 5.2.4.2 Human Insulin Biosimilars

- 5.2.1 Basal or Long Acting Insulins

- 5.3 Combination drugs

- 5.3.1 Insulin combinations

- 5.3.1.1 NovoMix (Biphasic Insulin Aspart)

- 5.3.1.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

- 5.3.1.3 Xultophy (Insulin Degludec and Liraglutide)

- 5.3.2 Oral Combinations

- 5.3.2.1 Janumet (Sitagliptin and Metformin)

- 5.3.1 Insulin combinations

- 5.4 Non-Insulin Injectable drugs

- 5.4.1 GLP-1 receptor agonists

- 5.4.1.1 Victoza (Liraglutide)

- 5.4.1.2 Byetta (Exenatide)

- 5.4.1.3 Bydureon (Exenatide)

- 5.4.1.4 Trulicity (Dulaglutide)

- 5.4.1.5 Lyxumia (Lixisenatide)

- 5.4.2 Amylin Analogue

- 5.4.2.1 Symlin (Pramlintide)

- 5.4.1 GLP-1 receptor agonists

6 MARKET INDICATORS

- 6.1 Type-1 Diabetic Population

- 6.2 Type-2 Diabetic Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Takeda

- 7.1.2 Novo Nordisk

- 7.1.3 Pfizer

- 7.1.4 Eli Lilly

- 7.1.5 Janssen Pharmaceuticals

- 7.1.6 Astellas

- 7.1.7 Boehringer Ingelheim

- 7.1.8 Merck And Co.

- 7.1.9 AstraZeneca

- 7.1.10 Bristol Myers Squibb

- 7.1.11 Novartis

- 7.1.12 Sanofi

- 7.2 COMPANY SHARE ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS