PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851633

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851633

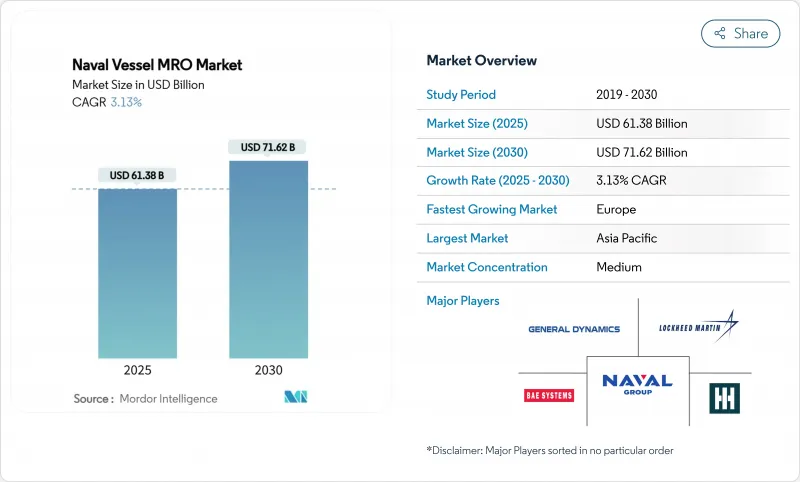

Naval Vessel MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The naval vessel MRO market size stands at USD 61.38 billion in 2025. It is forecasted to reach USD 71.62 billion by 2030 at a 3.13% CAGR, underscoring steady growth driven by government defense priorities more than commercial dynamics.

Sustained modernization programs, higher operational tempos in contested waters, and shifting toward performance-based logistics (PBL) contracts continue to anchor demand. Nuclear-powered vessel upkeep and dry-dock overhauls remain the most lucrative niches as they require specialized infrastructure and deep technical expertise, locking in premium pricing. Asia-Pacific accounts for the largest regional spend, propelled by China's rapid fleet expansion and allied counter-responses, while Europe is accelerating fastest on the back of renewed NATO commitments. Supply-chain fragility and skilled-labor shortages pose measurable headwinds, yet digital twin analytics and additive manufacturing mitigate downtime and unlock incremental savings.

Global Naval Vessel MRO Market Trends and Insights

Fleet-Modernization Programs

Nationwide upgrade plans are reshaping the naval vessel MRO market demand as governments aim to stretch capability rather than merely expand fleet count. The Philippines' USD 35 billion modernization drive and Turkey's three-year fleet enhancement initiative earmark sizable shares for maintenance infrastructure and platform upgrades rather than for acquisition only. Similar strategies in Denmark and Australia show that mid-tier navies can secure disproportionate capability gains by funding refits, overhauls, and modular upgrades. Submarine hull-life extensions add 10-15 years of service at near one-quarter of new-build cost, generating durable MRO revenue. Predictability improves because phased work packages allow contractors to plan labor and inventory well in advance, narrowing schedule slippage.

Life-Extension of Legacy Fleets

Keeping older ships battle-ready has moved from thrift to necessity as next-generation hulls arrive late. The US Navy cruiser overhaul program and the Royal Navy Type 23 frigate life-extension effort illustrate how navies capture 70-80% of modern capability for only 15-25% of replacement cost. Enhanced coatings, structural health monitoring, and mid-life combat-system swaps tackle fatigue and obsolescence while predictive analytics tighten inspection intervals. Growing reliance on legacy vessels stabilizes demand for depot-level refits that independent yards cannot easily replicate, bolstering premium pricing for incumbent contractors.

Dry-Dock Slot Overruns and Costs

Aging facilities and project creep push overhaul budgets well above plan. Pearl Harbor's dry-dock modernization ballooned from USD 6.1 billion to USD 16 billion, while Portsmouth Naval Shipyard costs quadrupled, blocking capacity for other urgent work. The Shipyard Infrastructure Optimization Program injects USD 21 billion, yet it cannot eliminate near-term gaps that delay submarine refits by 12-18 months. Commercial yards often refuse naval contracts because overruns jeopardize profitability, further tightening the bottleneck.

Other drivers and restraints analyzed in the detailed report include:

- Rising Maritime-Security Tensions

- Adoption of PBL Contracts

- Skilled-Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Submarines accounted for 33.88% of the 2024 naval vessel MRO market, reflecting their nuclear-propulsion complexity and deterrence value that anchor multi-year service contracts. High regulatory barriers restrict competition and support premium rates. Frigates represent the fastest-growing slice at 5.26% CAGR thanks to their role in distributed surface operations and relatively quicker build cycles that soon enter sustainment phases. Destroyers and corvettes sit mid-pack; the former benefit from Aegis-system maintenance, while the latter attract emerging littoral navies seeking budget-friendly patrol craft.

Subsurface platforms require extensive reactor refueling, acoustic signature checks, hull pressure tests, and lock-in depot-level workloads. Frigate programs leverage modular combat-system blocks, simplifying mid-life upgrades and enticing navies to invest in incremental capability paths instead of fresh hulls. Digital twin pilots under Spain's ISOPRENE project have demonstrated 15-20% cuts in unscheduled downtime for both vessel classes, pointing toward broader adoption over the forecast period.

Dry-dock work held 39.22% of the naval vessel MRO market in 2024 due to statutory hull inspections, shaft-line replacements, and propulsion-system overhauls that mandate docking. The segment enjoys steady visibility because mandatory periodicity supports multi-year master schedules. Modification and upgrade services are growing 3.71% annually as navies retrofit sensors, weapons, and electronic-warfare suites rather than wait for new builds.

Additive manufacturing is reshaping component repair economics. Metal 3D printers on the USS Bataan already produce certified spares at sea, cutting logistics lag and freeing dock space for heavier tasks. PBL frameworks incentivize suppliers to invest further in this capability, as faster part turnarounds boost contract performance metrics.

The Naval Vessel MRO Market Report is Segmented by Vessel Type (Aircraft Carriers, Destroyers, Frigates, Corvettes, and More), MRO Type (Engine MRO, Dry-Dock MRO, Component MRO, and More), Maintenance Level (Organizational/Operational, Depot, and More), Propulsion Type (Nuclear-Powered Vessels, Conventional), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.59% of the 2024 naval vessel MRO market spending, anchored by China's fleet growth toward 435 ships by 2030 and allied counter-moves such as Australia's plan to double its surface force. Shipbuilding powerhouses South Korea and Japan offer overflow dock capacity; Hanwha Ocean became the first Korean yard to win US Navy repair work, underscoring deeper allied collaboration.

Europe is the fastest-growing region at 4.00% CAGR as NATO members lift defense outlays to at least 2% of GDP. Denmark's large-scale fleet expansion, France's Tourville submarine commissioning, and Greece's USD 27 billion rearmament funnel fresh hulls into sustainment pipelines. Turkey's EUR 350 million Aksaz Naval Base upgrade further broadens regional maintenance options and reflects wider Mediterranean security concerns.

North America sustains robust but stable demand as the US Navy balances modernization with aging-yard constraints. Emergency supplements of USD 5.7 billion for submarine labor and a USD 40.1 billion annual shipbuilding budget highlight fiscal commitment, yet projected force levels drop to 283 ships by 2027 before rebuilding toward 381 by 2054. South America and the Middle East/Africa remain smaller contributors, though programs like ZAR 1.4 billion (USD 78.90 million) submarine refit point to gradual upticks.

- General Dynamics Corporation

- Huntington Ingalls Industries, Inc.

- Lockheed Martin Corporation

- NAVANTIA, S.A., SME

- thyssenkrupp AG

- BAE Systems plc

- Naval Group

- Rolls-Royce plc

- Rhoads Industries, Inc.

- Abu Dhabi Ship Building Company PJSC

- Larsen & Toubro Limited

- Damen Shipyards Group

- Singapore Technologies Engineering Ltd.

- FINCANTIERI S.p.A.

- HD Hyundai Heavy Industries Co., Ltd.

- Saab AB

- Austal Limited

- Mitsubishi Heavy Industries, Ltd.

- Kongsberg Gruppen ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet-modernization programs

- 4.2.2 Life-extension of legacy fleets

- 4.2.3 Rising maritime-security tensions

- 4.2.4 Adoption of PBL contracts

- 4.2.5 Digital-twin based predictive MRO

- 4.2.6 Additive-manufactured spares

- 4.3 Market Restraints

- 4.3.1 Dry-dock slot overruns and costs

- 4.3.2 Skilled-labor shortages

- 4.3.3 Cyber-risk to connected shipyards

- 4.3.4 Green-compliance waste-disposal cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vessel Type

- 5.1.1 Aircraft Carriers

- 5.1.2 Destroyers

- 5.1.3 Frigates

- 5.1.4 Corvettes

- 5.1.5 Submarines

- 5.1.6 Other Vessel Types (Support and Auxiliary Vessels, Unmanned Surface, and Underwater Vessels)

- 5.2 By MRO Type

- 5.2.1 Engine MRO

- 5.2.2 Dry-Dock MRO

- 5.2.3 Component MRO

- 5.2.4 Modification and Upgrade

- 5.3 By Maintenance Level

- 5.3.1 Organizational/Operational

- 5.3.2 Intermediate/Field

- 5.3.3 Depot

- 5.4 By Propulsion Type

- 5.4.1 Nuclear-Powered Vessels

- 5.4.2 Conventional (Diesel/Gas Turbine)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Egypt

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Dynamics Corporation

- 6.4.2 Huntington Ingalls Industries, Inc.

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 NAVANTIA, S.A., SME

- 6.4.5 thyssenkrupp AG

- 6.4.6 BAE Systems plc

- 6.4.7 Naval Group

- 6.4.8 Rolls-Royce plc

- 6.4.9 Rhoads Industries, Inc.

- 6.4.10 Abu Dhabi Ship Building Company PJSC

- 6.4.11 Larsen & Toubro Limited

- 6.4.12 Damen Shipyards Group

- 6.4.13 Singapore Technologies Engineering Ltd.

- 6.4.14 FINCANTIERI S.p.A.

- 6.4.15 HD Hyundai Heavy Industries Co., Ltd.

- 6.4.16 Saab AB

- 6.4.17 Austal Limited

- 6.4.18 Mitsubishi Heavy Industries, Ltd.

- 6.4.19 Kongsberg Gruppen ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment