PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687384

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687384

Artillery Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

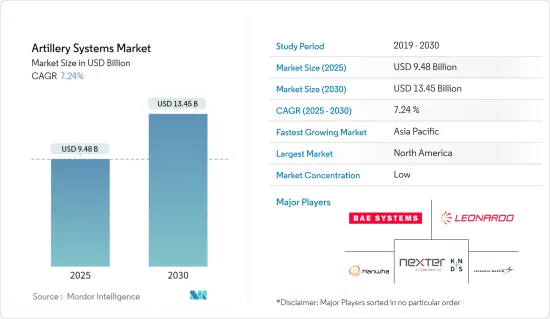

The Artillery Systems Market size is estimated at USD 9.48 billion in 2025, and is expected to reach USD 13.45 billion by 2030, at a CAGR of 7.24% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic affected the market in two key ways. Firstly, disruptions in global supply chains and manufacturing facilities may have caused delays in the production and delivery of artillery systems, impacting procurement timelines for various countries. Secondly, with governments allocating significant resources to address the pandemic's immediate challenges, defense budgets might have been reallocated or constrained, potentially affecting investments in new artillery systems.

- The increasing military spending of emerging countries is helping them to invest in the development of new and advanced artillery systems. The initiation of weapon modernization programs to develop sophisticated artillery is anticipated to bolster the adoption of newer generation artillery, thus bolstering the market prospects in the coming years. Escalating regional conflicts and geopolitical tensions have led to a growing demand for sophisticated artillery systems capable of precision strikes and quick response times. Also, the changing nature of warfare and the growing demand for high-precision arms and ammunition to support friendly troops while minimizing collateral damage has bolstered the demand for the artillery systems market.

Artillery Systems Market Trends

Increasing Defense Expenditure Supporting the Growth of the Artillery Systems Market

- On account of the profound changes in the international strategic landscape, the configuration of the international security system has been undermined by the growing hegemonism, unilateralism, and power politics that have fueled several ongoing global conflicts. Uncertainties in territorial rights between many countries, like the Saudi-Iran cold war in the Middle East, are among the major causes disturbing the geopolitical climate.

- The most common reaction of governments, in this regard, is to increase military spending to improve security in their respective countries. Military powerhouses, such as the United States, the United Kingdom, China, and India, have been focused on augmenting their military firepower and warfare capabilities. To ensure combat readiness of existing defense systems, development and procurement programs are currently underway to modernize the weapon systems used by the armed forces. A simultaneous push for indigenization is also driving several countries' local development of such systems. The increase in defense budgets currently supports these programs.

- The invasion of Ukraine had an immediate impact on military spending decisions in Central and Western Europe. This included multi-year plans to boost spending from several governments. World military spending grew for the eighth consecutive year in 2022 to an all-time high of USD 2240 billion. By far, the sharpest rise in spending (+13 percent) was seen in Europe and was largely accounted for by Russian and Ukrainian spending. However, military aid to Ukraine and concerns about a heightened threat from Russia strongly influenced many other states' spending decisions, as did tensions in East Asia.

- The United States remains by far the world's biggest military spender. US military spending reached USD 877 billion in 2022, which was 39 percent of total global military spending and three times more than the amount spent by China, the world's second-largest spender.

- Countries' significant investments to modernize their military may support the artillery systems market growth during the forecast period. Countries are focused on developing long-range fire capabilities to achieve a tactical advantage on the battlefield. To develop long-range precision fire capabilities, countries like the United States are initiating the procurement of artillery systems.

- For instance, in December 2022, Lithuania's Defense Ministry signed a contract with the French group Nexter for the purchase of 18 Caesar artillery guns.

Asia-Pacific is Expected to Witness the Highest CAGR During the forecast period

- Asia-Pacific is expected to register a high CAGR during the forecast period. The escalated tensions between the countries in this region have encouraged the rapid modernization of the armed forces. Countries like China, India, Australia, Japan, and South Korea are significantly investing in the development, building, and procurement of artillery systems.

- For instance, in November 2022, Kalyani Strategic Systems Limited (India) signed a deal to export 155mm artillery guns to a friendly nation in a non-conflict zone. The deal is worth USD 155 million, and the arms are to be exported by 2025. The Kalyani Group is also reported to establish the world's largest artillery factory in India. In May 2023, The People's Liberation Army-Strategic Support Force (PLA-SSF) of China gave a contract to PLA-SSF Northwest Institute of Nuclear Technology (NINT) to produce 203-millimeter artillery guns.

Artillery Systems Industry Overview

The artillery systems market is fragmented, with many global and local players contributing significantly to the growth of the market through competitive pricing and innovation. Some of the major companies in the artillery systems market include BAE Systems plc, Lockheed Martin Corporation, Hanwha Group, Leonardo S.p.A, Elbit Systems Ltd., and Nexter Group. The companies are mainly focusing on enhancing the capabilities of their artillery systems portfolio to increase their market share.

Foreign players are competing with local players to gain multi-billion long-term contracts. Some players have also partnered with local companies to expand their customer base and share technical expertise. Tensions across Eastern Europe, the Middle East, and Asia-Pacific are generating the demand for new artillery systems. The demand is also higher in the US, which is trying to fill in the gaps to strengthen its land forces by replacing the aging systems with new artillery systems. Also, a growing focus on strengthening naval capabilities over the past decade has resulted in significant new orders for frigates, corvettes, aircraft carriers, destroyers, and offshore vessels, thereby generating the need for new artillery guns.

For instance, in May 2023, Elbit Systems announced that as part of an agreement between the Israeli Ministry of Defense and the Netherlands Ministry of Defense, it was awarded a contract worth USD 305 million to supply Precise & Universal Launching System (PULS) artillery rocket systems to the Royal Netherlands Army.

Likewise, In November 2022, JPEO A&A and ACC-Rock Island awarded a new task order to General Dynamics Ordnance and Tactical Systems to build a new 155 mm artillery metal parts production line in Texas that will utilize free-flow forming technology, which delivers flexible, cost-effective, and precise metal forming with higher machine speeds and more accurate, uniform products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2031)

- 5.1 Type

- 5.1.1 Howitzer

- 5.1.2 Mortar

- 5.1.3 Anti-air Artillery

- 5.1.4 Rocket Artillery

- 5.1.5 Other Types (Naval and Coastal Artillery)

- 5.2 Range

- 5.2.1 Short Range (5-30 kilometers)

- 5.2.2 Medium Range (31-60 kilometers)

- 5.2.3 Long Range (Above 60 kilometers)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Hanwha Group

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 Rostec

- 6.2.5 Lockheed Martin Corporation

- 6.2.6 Avibras Industria Aeroespacial SA

- 6.2.7 Nexter Group

- 6.2.8 Denel SOC Ltd

- 6.2.9 Leonardo S.p.A

- 6.2.10 Singapore Technologies Engineering Ltd

- 6.2.11 RUAG Group

- 6.2.12 Norinco International Cooperation Ltd.

- 6.2.13 THALES

- 6.2.14 Rheinmetall AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS