PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437908

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1437908

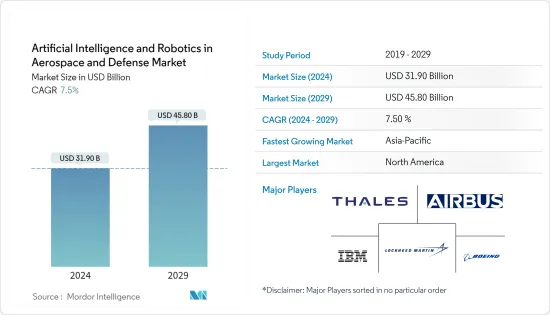

Artificial Intelligence and Robotics in Aerospace and Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Artificial Intelligence and Robotics in Aerospace and Defense Market size is estimated at USD 31.90 billion in 2024, and is expected to reach USD 45.80 billion by 2029, growing at a CAGR of 7.5% during the forecast period (2024-2029).

The global aerospace and defense manufacturing sector is undergoing an unprecedented disruption due to the COVID-19 pandemic. Also, in the commercial airline industry, the revenue of airport operators and airlines decreased in 2020 and 2021 due to the restrictions on domestic and international travel to attenuate the spread of COVID-19. Consequently, the market for artificial intelligence and robotics in aerospace and defense witnessed a slight decline as the revenues of end users declined.

Nevertheless, some of the major airlines and airport authorities have invested in the implementation of artificial intelligence in various passenger processes at airports to enhance their safety and efficiency during the COVID-19 pandemic.

The ever-increasing application of AI-based technologies in the A&D sector and increasing investments being funneled to develop and integrate AI and machine learning (ML) into the end-user sectors are anticipated to drive the market in focus during the forecast period. However, the associated technical and operational challenges that are often observed during the initial stages of development and adoption of a nascent technology are hindering the adoption of AI-based technologies.

AI and Robotics in Aerospace and Defense Market Trends

The Military Application Segment is Expected to Dominate During the Forecast Period

The plethora of applications of AI within the military segment, such as big data analytics for better decision-making, automated logistics through the integration of unmanned ground vehicles (UGV) and unmanned aerial vehicles (UAV), bioinspired robots (swarm AI and deep neural networks), underwater mines location through neural networks, and object location are expected to promote the market growth during the forecast period. The rise in investments in the development and integration of AI and robotics and the enhanced defense budget allocation toward the R&D and acquisition of AI-based equipment are also anticipated to augment market prospects. For instance, out of 21,000 equipment contracts published by the People's Liberation Army (PLA) China in 2020, approximately 350 records were aligned to AI systems and equipment. In October 2021, NATO announced plans to launch an innovation fund worth USD 1 billion as its initial strategy to stay ahead of the competition within the AI vertical. In June 2021, Pentagon announced plans to spend USD 874 million on AI and machine learning technologies under the DOD budget 2022, signifying a Y-o-Y increase of 50% in budget allocation toward AI-based technologies. Such investments are expected to drive the growth of the military segment of the market during the forecast period.

Asia-Pacific is Expected to Witness the Highest Growth During the Forecast Period

Asia-Pacific is slated to witness the highest growth in the adoption of artificial intelligence and machine learning technologies as OEMs and operators alike are envisioned to enhance their investment in AI integration processes across the supply chain. Countries such as Japan, South Korea, and China have emerged as the leading innovators in the field of AI development and integration. Many institutes in the region are involved in research activities pertaining to advanced applications of AI in the aviation industry. Numerous aircraft and associated component manufacturing units in Asia-Pacific have witnessed steady benefits from the incorporation of AI technologies. For instance, the use of adaptive machining and cutting-edge automated inspection systems at the Pratt & Whitney facility in Singapore has caused steady growth in output volumes at the facility in recent years. China envisions to use AI technologies to strengthen the People's Liberation Army (PLA) by enabling it to engage in intelligent warfare, defined by strategists as the operationalization of AI and its enabling technologies, such as cloud computing, big data analytics, quantum information, and unmanned systems, for military applications. The PLA aims to achieve full modernization by 2035 and at par with the US military by 2050. China's New Generation Artificial Intelligence Development Plan outlines its strategy for the development of AI for defense applications such as providing support for command and decision-making, military deductions, defense equipment, and other applications. Such developments are anticipated to have a profound positive effect on the market in focus during the forecast period.

AI and Robotics in Aerospace and Defense Industry Overview

The market for artificial intelligence and robotics in aerospace and defense is highly fragmented, with the presence of several players, including robot manufacturers and OEMs that offer products and solutions incorporating AI hardware and software for aerospace and defense end users. In addition, the market comprises AI and robotic technology providers for OEMs. Some of the leading players in the artificial intelligence and robotics in aerospace and defense market are The Boeing Company, Lockheed Martin Corporation, Airbus SE, IBM Corporation, and Thales Group. To expand their presence in the market, companies are partnering with aerospace and defense OEMs to develop new and advanced AI-based solutions that will enhance the safety and efficiency of operations by streamlining mission effectiveness. On this note, in October 2021, IBM and Raytheon Technologies signed a partnership agreement to develop advanced AI, cryptographic, and quantum solutions for the aerospace, defense, and intelligence industries. The systems integrated with AI and quantum technologies are expected to have better-secured communication networks and improved decision-making processes for aerospace and government customers. Also, defense OEMs are collaborating on developing autonomous features and sophisticated acoustic and imaging sensors (like cameras, radar, sonar, GPS, etc.) to decrease the pilot involvement operation of systems in complex, variable, and communication-limited environments. Such partnerships and developments are anticipated to support the growth of the players in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by Offering, 2021

- 3.3 Market Share by Application, 2021

- 3.4 Market Share by Geography, 2021

- 3.5 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD billion)

- 5.1 Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Service

- 5.2 Application

- 5.2.1 Military

- 5.2.2 Commercial Aviation

- 5.2.3 Space

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Airbus SE

- 6.2.2 IBM Corporation

- 6.2.3 The Boeing Comapny

- 6.2.4 Nvidia Corporation

- 6.2.5 GE Aviation

- 6.2.6 Thales Group

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Intel Corporation

- 6.2.9 Iris Automation Inc.

- 6.2.10 SITA

- 6.2.11 Raytheon Technologies Corporation

- 6.2.12 General Dynamics Corporation

- 6.2.13 Northrop Grumman Corporation

- 6.2.14 Microsoft

- 6.2.15 Spark Cognition

- 6.2.16 Honeywell International Inc.

- 6.2.17 Indra Sistemas SA

- 6.2.18 T-Systems International GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS