PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851079

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851079

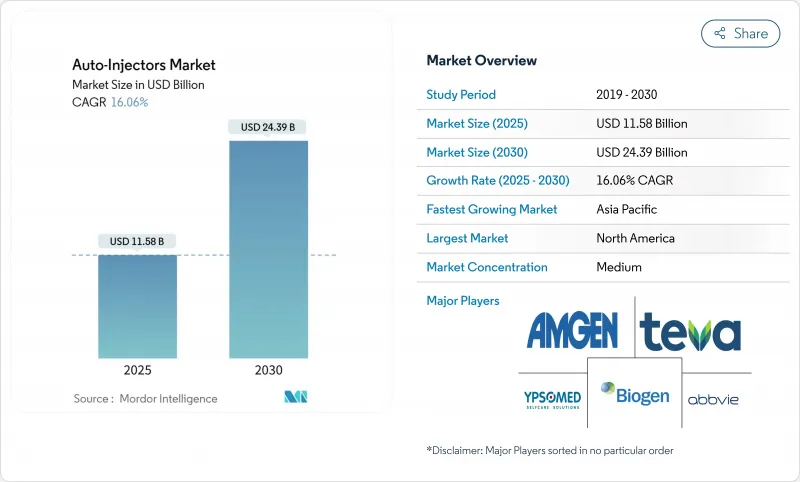

Auto-Injectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The auto-injectors market size stands at USD 11.58 billion in 2025 and is on course to reach USD 24.39 billion by 2030, reflecting a firm 16.06% CAGR.

Rising biologic drug launches, a larger chronic disease population and a decisive shift toward self-administration are synchronizing to propel demand. Regulatory agencies are clearing novel formats at a faster clip, illustrated by the first needle-free epinephrine alternative in more than three decades approved in 2024. Emergency-preparedness stock-piles, multi-billion-dollar capacity additions from leading manufacturers and sustained payer support for home-care therapies amplify momentum. Even so, specialty-component shortages and stricter combination-device rules underline the need for resilient supply chains and robust quality controls.

Global Auto-Injectors Market Trends and Insights

Growth Of Biologic Drugs Requiring Self-Injection

Large-volume subcutaneous biologics already account for close to 15% of all biopharmaceuticals and their share is climbing. Manufacturers are increasingly re-formulating intravenous therapies as self-injectable options to relieve infusion-center congestion, demonstrated by the 2025 approval of a self-injection version of Vyvgart Hytrulo. Autoimmune regimens built around B-cell-targeting biologics show similar transitions that place precision delivery demands on devices. High viscosity and varied dose volumes are steering engineers toward tighter tolerances, advanced materials and intuitive user interfaces. The result is a pipeline of sophisticated platforms that favour the auto-injectors market over traditional syringes.

Rising Incidence Of Chronic Autoimmune Diseases

Enhanced diagnostic capabilities and ageing populations are pushing autoimmune prevalence upward, reinforcing steady device uptake. World Health Organization data links unsafe care to millions of deaths, underscoring the value of reliable self-administration solutions. In multiple sclerosis therapy, 70% of patients rate the latest RebiSmart model as appealing, and almost 90% of specialist nurses call it very good or excellent. Wider biosimilar availability - now offered at up to 65% discounts - also expands access. Yet adherence gaps persist, with research showing that 41% of adrenal-insufficiency patients cannot self-inject during crises, so simplified design and structured training remain priorities.

Patient Preference For Alternative Drug-Delivery Modes

Needle anxiety continues to deter certain users, fuelling demand for nasal, oral or microneedle solutions. ARS Pharmaceuticals booked USD 7.8 million in Q1 2025 sales of neffy after only a few months on the market, with over 5,000 prescriptions written. Capital inflows into dissolvable microarray start-ups confirm investors see lasting potential in needle-free formats. The challenge is achieving pharmacokinetic parity across indications, and emergency settings require especially clear patient instructions. Notably, 99% of subjects in SIMLANDI trials found the device easy to use, which suggests user-centred design can mitigate needle aversion.

Other drivers and restraints analyzed in the detailed report include:

- Shift To Home-Based Care/Self-Administration

- Connectivity & Adherence-Analytics Integration

- Stringent Combination-Device Regulatory Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rheumatoid arthritis retained 36.23% of the auto-injectors market share in 2024 on the back of mature biologic protocols and well-established self-injection routines. Conversely, anaphylaxis is the quickest climber, advancing at 19.24% CAGR to 2030 as food allergy diagnoses rise and school-stock mandates spread. Multiple sclerosis treatments continue to benefit from device upgrades such as RebiSmart 3.0, which 70% of patients find appealing. Diabetes-related use is changing through artificial-intelligence-enabled predictive analytics that support tighter glucose control. Migraine, psoriasis and cardiovascular indications round out the therapeutic spread, each commanding custom engineering from single-dose simplicity to large-volume precision.

Patient expectations now extend beyond reliable drug delivery to encompass connectivity, discretion and minimal pain. Emergency products must remain intuitive under stress, while chronic-disease devices gain traction when adherence data integrate seamlessly with digital health portals. These differing priorities encourage platform diversification and sustain innovation activity across the auto-injectors market.

Disposable units still generated 69.54% of revenue in 2024 because of convenience and proven manufacturing economies. Connected smart formats, however, are soaring at a 20.23% CAGR to 2030 as payers recognise the clinical and economic value of validated adherence. Nine in ten payers now agree that connectivity closes therapeutic gaps, and more than four in five are open to modest price premiums. Re-usable devices keep a foothold in cost-sensitive settings and for drugs that need flexible dosing, yet infection-control protocols increasingly favour single-use disposables.

Adoption remains gated by data-security obligations and clinician workflow integration. Even so, iterative firmware upgrades and user-experience refinements are resolving early-generation shortcomings. This dynamic positions smart platforms as a core growth driver for the auto-injectors market and a differentiator for entrants seeking to bypass incumbent scale advantages.

Autoinjectors Market Report is Segmented by Application (Rheumatoid Arthritis, Multiple Sclerosis, and More), Usability/ Type (Disposable Autoinjectors, Reusable Autoinjectors and More), Device Technology (Spring Loaded, Gas Propelled and More), Route of Administration (Subcuatenous, Intramuscular and More), End User (Home Care Settings, Hospitals and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the auto-injectors market with 44.32% share in 2024, thanks to mature reimbursement frameworks, strong biologics pipelines and proactive emergency-preparedness programs. Recent capacity expansions, including a USD 4.1 billion facility in North Carolina and parallel projects by other majors, reinforce supply for regional demand. The Health Resources Priorities and Allocations System also guarantees allocation priority during crises, providing an additional safety net for public health. Still, the FDA's warning letter to BD reminds stakeholders that quality-system diligence is non-negotiable.

Asia-Pacific is the fastest-growing region, advancing at 18.30% CAGR through 2030. Regulatory harmonisation initiatives are easing cross-border submissions, and governments are investing heavily in healthcare infrastructure. Japan exhibits strong emergency-anaphylaxis adoption yet low school-administration rates signal latent upside. China's evolving innovation framework and India's cost-efficient manufacturing expand the regional value chain. Demographic shifts toward higher chronic-disease incidence present a durable demand base that is converting into tangible device volumes for the auto-injectors market.

Europe records steady growth underpinned by clear EMA guidance on drug-device combinations and receptive biosimilar policies that compress treatment costs. Recent approvals of nasal epinephrine and continued capital outlays for medical-system production bolster supply security. Article 117 conformity requirements elevate compliance workloads, but industry stakeholders view the long-term payoff as greater patient confidence. Taken together, these dynamics position Europe as a stable, innovation-friendly arena within the global auto-injectors market.

- Abbvie

- Amgen

- AstraZeneca

- Bayer

- Beckton Dickinson

- Biogen

- Eli Lilly and Company

- Novartis

- Teva Pharmaceutical Industries

- Ypsomed

- Antares Pharma

- Mylan (Viatris)

- Sanofi

- Pfizer

- Johnson & Johnson

- Novo Nordisk

- Medtronic

- Gerresheimer

- Insulet

- B. Braun

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth Of Biologic Drugs Requiring Self-Injection

- 4.2.2 Rising Incidence Of Chronic Autoimmune Diseases

- 4.2.3 Shift To Home-Based Care/Self-Administration

- 4.2.4 Connectivity & Adherence-Analytics Integration

- 4.2.5 Government Stock-Piling Of Epinephrine Devices

- 4.2.6 Expansion Of Micro-Needle, Needle-Free Platforms

- 4.3 Market Restraints

- 4.3.1 Patient Preference For Alternative Drug-Delivery Modes

- 4.3.2 Stringent Combination-Device Regulatory Pathways

- 4.3.3 Supply-Chain Fragility For Specialty Plastics & Springs

- 4.3.4 Cyber-Security & Data-Privacy Concerns In Smart Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Application

- 5.1.1 Rheumatoid Arthritis

- 5.1.2 Multiple Sclerosis

- 5.1.3 Anaphylaxis

- 5.1.4 Diabetes

- 5.1.5 Migraine

- 5.1.6 Psoriasis

- 5.1.7 Cardiovascular Diseases

- 5.1.8 Others

- 5.2 By Usability / Type

- 5.2.1 Disposable Auto-Injectors

- 5.2.2 Re-usable Auto-Injectors

- 5.2.3 Connected / Smart Auto-Injectors

- 5.3 By Device Technology

- 5.3.1 Spring-Loaded

- 5.3.2 Gas-Propelled

- 5.3.3 Electromechanical

- 5.3.4 Needle-Free / Micro-Needle

- 5.3.5 Wearable On-Body Injectors

- 5.4 By Route of Administration

- 5.4.1 Subcutaneous

- 5.4.2 Intramuscular

- 5.4.3 Intradermal

- 5.5 By End-User

- 5.5.1 Home-Care Settings

- 5.5.2 Hospitals & Clinics

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 Amgen

- 6.3.3 AstraZeneca

- 6.3.4 Bayer

- 6.3.5 Becton, Dickinson & Company

- 6.3.6 Biogen

- 6.3.7 Eli Lilly

- 6.3.8 Novartis

- 6.3.9 Teva Pharmaceutical

- 6.3.10 Ypsomed

- 6.3.11 Antares Pharma

- 6.3.12 Mylan (Viatris)

- 6.3.13 Sanofi

- 6.3.14 Pfizer

- 6.3.15 Johnson & Johnson

- 6.3.16 Novo Nordisk

- 6.3.17 Medtronic

- 6.3.18 Gerresheimer

- 6.3.19 Insulet Corporation

- 6.3.20 B. Braun Melsungen

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment