PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044193

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044193

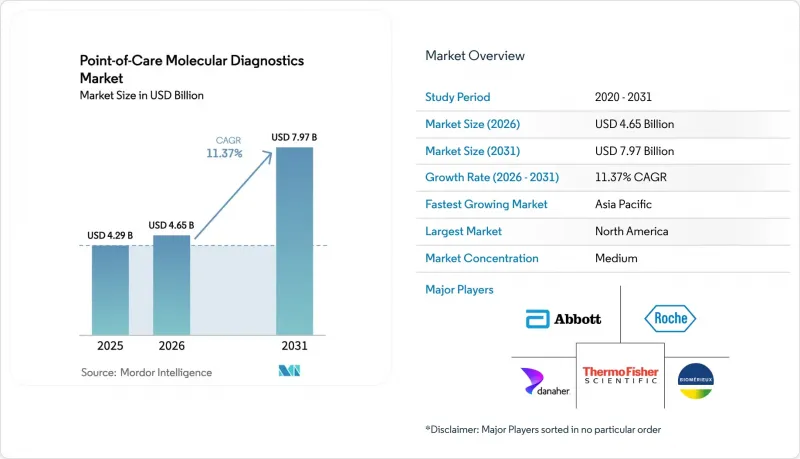

Point-of-Care Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The point-of-care molecular diagnostics market size was valued at USD 4.29 billion in 2025 and is estimated to grow from USD 4.65 billion in 2026 to reach USD 7.97 billion by 2031, at a CAGR of 11.37% during the forecast period (2026-2031).

The growing deployment of sample-to-answer instruments in emergency departments, pharmacies, and physician offices shortens result times from days to minutes, underpinning this outlook. Public-sector stockpiling initiatives, led by the U.S. Biomedical Advanced Research and Development Authority, are shifting procurement toward decentralized platforms that can be field-deployed within 72 hours of a public-health threat. Technology maturation from lyophilized reagents that tolerate room-temperature shipping to AI-enabled cloud dashboards that monitor instrument health continues to reduce ownership costs, opening the door for small clinics and remote facilities. In parallel, regulatory bodies in the United States, Europe, and Japan have expanded CLIA waiver, IVDR, and reimbursement pathways, respectively, providing physicians with new financial incentives to order molecular panels at the point of care rather than outsourcing samples to centralized laboratories.

Global Point-of-Care Molecular Diagnostics Market Trends and Insights

Growing Burden of Infectious Diseases and Need for Rapid Diagnosis

Delayed pathogen identification drives empiric antibiotic use, accelerates the development of resistance, and increases hospital costs. The World Health Organization documented a 12% year-over-year increase in drug-resistant tuberculosis cases across Southeast Asia in 2024, prompting ministries of health to mandate four-hour turnaround molecular susceptibility testing at district hospitals. Visby Medical's 30-minute PCR panel for the three most common sexually transmitted infections cut loss-to-follow-up from 28% to under 5% in U.S. pilot clinics. During the 2024-2025 season, infant hospitalizations for respiratory syncytial virus (RSV) exceeded the 2019 baseline by 18%, thereby increasing demand for multiplex panels that can simultaneously separate RSV, influenza, and SARS-CoV-2 in a single run. The Centers for Disease Control and Prevention added 120 community hospitals to its Laboratory Response Network in 2025, each equipped with sample-to-answer instruments to bypass reference-lab bottlenecks during outbreaks.

Government Funding and Pandemic Preparedness Programs

Federal agencies committed USD 1.2 billion during 2024-2025 to stockpile instruments and cartridges after centralized capacity collapsed under COVID-19 surges. Europe's HERA earmarked EUR 400 million (USD 430 million) to co-fund platform roll-outs in rural hospitals with fewer than 50,000 residents. Japan increased reimbursement to JPY 15,000 (approximately USD 100) per POC molecular test when results guide isolation within two hours, tripling prior rates and shifting emergency departments toward on-site testing. The NIH Rapid Acceleration of Diagnostics Technology program allocated USD 85 million across 12 consortia to compress sample collection, extraction, amplification, and detection into single-use cartridges.

Fragmented Reimbursement and Regulatory Hurdles

Reimbursement rates vary from USD 25 to USD 90 per test among U.S. private insurers, fostering price opacity that deters physician office adoption despite proven clinical value. Europe's IVDR requires third-party conformity assessments; however, only 12 notified bodies are accredited for Class C devices, which stretches review timelines beyond 18 months. India requires imported POC molecular platforms to undergo local clinical validation, which adds approximately USD 200,000 to launch costs and extends timelines by one year. A 2025 Health Affairs analysis quantified 35% lower utilization of POC molecular tests in U.S. ambulatory settings owing to reimbursement uncertainty compared with send-out PCR.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Sample-To-Answer PCR Platforms

- Expansion of CLIA-Waived Multiplex Panels in Physician Offices

- High Cost of Consumables and Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America generated 43.64% of 2025 revenue, thanks to reimbursement parity with central-lab PCR under the Clinical Laboratory Fee Schedule and to ASPR contracts that embedded 5,000 FilmArray systems in the Strategic National Stockpile. Canada's CAD 180 million initiative equipped remote Indigenous facilities with sample-to-answer instruments, trimming tuberculosis diagnosis from 14 days to four hours and reinforcing regional momentum. Yet private-payer fragmentation keeps ambulatory uptake uneven, with test prices swinging nearly fourfold across insurers for identical assays.

The Asia-Pacific is the fastest-growing region, with a 13.29% CAGR, driven by China's CNY 12 billion township-hospital modernization and India's public-private rollout of tier-2 POC hubs that bypass cold-chain deficits. Japan's reimbursement tripling to JPY 15,000 (USD 100) for two-hour isolation decisions accelerated emergency department adoption. At the same time, Southeast Asian governments work with World Bank loans to localize cartridge production after export bottlenecks during COVID-19. Australia harmonized approvals with FDA timelines, clearing 15 devices in 2024 and attracting multinational entrants.

Europe, the Middle East & Africa, along with South America, complete the global picture. Europe's full enforcement of the IVDR consolidates the market share of quality-system-strong incumbents but creates 18-month backlogs that deter start-ups. Germany's updated payer schedules now cover POC sexual-health tests across 40,000 GP clinics, while Global Fund grants subsidize HIV and hepatitis cartridges in Sub-Saharan Africa. Brazil piloted dengue and Zika panels in 50 primary-care clinics, recording training completion rates of only 15%, which highlights the workforce deficit that still limits decentralized adoption.

- Abbott Laboratories

- Beckton Dickinson

- Binx Health, Inc.

- bioMerieux

- Co-Diagnostics

- Danaher

- Roche

- Genedrive plc

- Hologic

- Meridian Bioscience

- Orasure Technologies

- Pfizer

- QIAGEN

- QuidelOrtho

- Siemens Healthineers

- T2 Biosystems

- Thermo Fisher Scientific

- Visby Medical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Infectious Diseases and Need for Rapid Diagnosis

- 4.2.2 Government Funding and Pandemic Preparedness Programs

- 4.2.3 Technological Advancements in Sample-to-Answer PCR Platforms

- 4.2.4 Expansion of CLIA-Waived Multiplex Panels in Physician Offices

- 4.2.5 Integration of AI-Driven Cloud Connectivity for Decentralized Testing

- 4.2.6 Shift Toward Home-Based Molecular Self-Testing Kits

- 4.3 Market Restraints

- 4.3.1 Fragmented Reimbursement and Regulatory Hurdles

- 4.3.2 High Cost of Consumables and Instruments

- 4.3.3 Supply-Chain Vulnerability of Microfluidic Cartridges

- 4.3.4 Data Privacy Concerns with Cloud-Connected POC Devices

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Assays & Kits

- 5.1.2 Instruments / Analyzers

- 5.1.3 Software & Digital Services

- 5.2 By Application

- 5.2.1 Infectious Diseases

- 5.2.2 Oncology

- 5.2.3 Hematology

- 5.2.4 Prenatal & Neonatal Testing

- 5.2.5 Endocrinology

- 5.2.6 Pharmacogenomics & Companion Dx

- 5.2.7 Other Applications

- 5.3 By Technology

- 5.3.1 PCR-Based

- 5.3.2 INAAT

- 5.3.3 Other Technologies

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Homecare Settings

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East And Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East And Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products And Services, And Analysis Of Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Binx Health, Inc.

- 6.3.4 BioMerieux SA

- 6.3.5 Co-Diagnostics Inc.

- 6.3.6 Danaher

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 Genedrive plc

- 6.3.9 Hologic Inc.

- 6.3.10 Meridian Bioscience Inc.

- 6.3.11 OraSure Technologies Inc.

- 6.3.12 Pfizer Inc.

- 6.3.13 Qiagen N.V.

- 6.3.14 QuidelOrtho Corporation

- 6.3.15 Siemens Healthineers AG

- 6.3.16 T2 Biosystems Inc.

- 6.3.17 Thermo Fisher Scientific Inc.

- 6.3.18 Visby Medical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment