PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066589

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066589

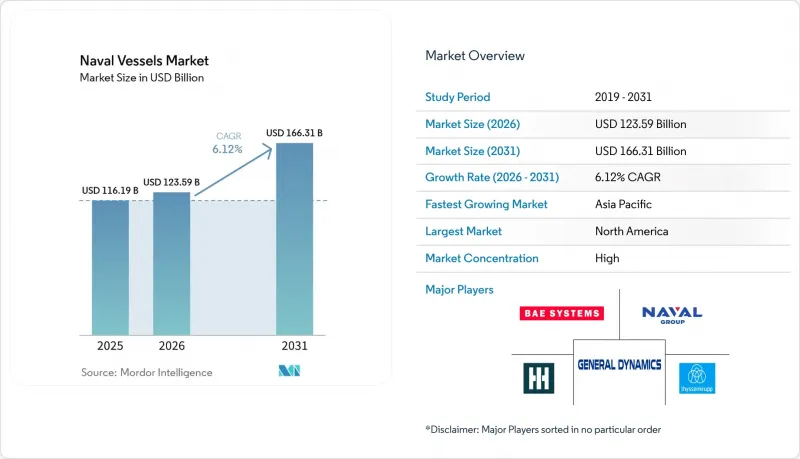

Naval Vessels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the naval vessels market size is expected to grow from USD 116.19 billion in 2025 to USD 123.59 billion in 2026 and is forecasted to reach USD 166.31 billion by 2031 at a 6.12% CAGR over 2026-2031.

This report is Segmented by Vessel Type (Destroyers, Frigates, Submarines, Corvettes, Aircraft Carriers, and Others), System (Marine Engine, Weapon Launch, Sensor, Navigation and Control, and More), Solution (Linefit and Retrofit), Application (Search and Rescue, Combat, MCM, Coastal, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Naval Vessels Market Trends and Insights

SSN/SSBN Recapitalization and AUKUS Accelerate Undersea Procurement

Subsurface fleets anchor the procurement momentum as allied governments lock multiyear spending on nuclear-powered attack and ballistic-missile submarines. In the US, recent awards for Virginia-class boats and Columbia-class advance procurement reinforce a durable undersea backlog that stabilizes supply chains and schedules for core components and specialized trades across the naval vessels market. AUKUS-related planning and infrastructure steps continue to shape industrial capacity decisions, while US policy initiatives to rebuild maritime strength underscore the priority given to high-end shipbuilding and workforce development that supports undersea programs. The scale of deterrent recapitalization, combined with allied interoperability requirements, sustains investment in design, construction, testing, and sustainment pipelines that extend beyond 2031 for the naval vessels market. These long-horizon commitments help offset schedule risk by enabling earlier material buys and supplier agreements, while aligning training and certification pathways for critical trades needed to execute submarine production.

Multi-Mission Surface Combatant Upgrades (AAW/BMD, VLS, Sensors)

Surface combatants are shifting from platform-centric to capability-centric concepts, where radar aperture, missile defense integration, and cooperative target engagement deliver the decisive edge. The rapid adoption of active electronically scanned array radars and software-defined sensor suites, exemplified by new SPY-6 family awards, strengthens layered air and missile defense across current and future classes, accelerating the role of sensors in value creation within the naval vessels market. As navies expand vertical launch density and refine combat-system software, they pursue modularity that allows faster drops of new capability with less time in the yard and fewer intrusive structural changes. The emphasis on integrated air and missile defense raises requirements for power, cooling, and electromagnetic compatibility, which in turn increases the complexity and timeline for integration, but reduces costly rework post-delivery. These choices elevate sensors and software to budget priorities and position upgrade programs as central to fleet readiness, a pattern consistent with the growing sustainment awards visible in the naval vessels market. The net effect is a tilt toward multi-mission fit across new builds and backfits, with interoperability and digital architecture considered as crucial as hull count.

Cost Overruns and Long Build Cycles Constrain New Starts

Cost growth and schedule slippage pressure new starts and force budget reallocation toward priority programs and sustainment. Independent government reviews highlight persistent budget challenges across major classes and delayed schedules that compress planned fleet capacity, which complicates near-term readiness planning in the naval vessels market. Program baselines for large combatants and carriers continue to be revised, and oversight bodies cite the need for stronger controls on design maturity, testing, and supplier readiness to curb rework and avoid compounding delays. The effect is a constrained pipeline for new platform starts and a heavier emphasis on extending the life of existing hulls where feasible. These dynamics also raise the importance of modular systems and incremental capability insertions that can be delivered without the costs and risks of full-ship replacement, which influences how navies set priorities in the naval vessels market. As the most capital-intensive projects take longer to complete, program managers lean on multiyear procurement when justified to stabilize supplier bases and lower unit costs over time.

Other drivers and restraints analyzed in the detailed report include:

- Grey-Zone/Coastal Security Boosts OPV, Corvette, Auxiliary Demand

- Rapid Integration of USV/UUV into Hybrid Fleet Concepts

- Workforce and Tier-2/3 Supplier Fragility Delays Deliveries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Submarines accounted for 33.26% of the 2025 naval vessels market share and are forecast to expand at a 7.81% CAGR through 2031, reflecting undersea recapitalization across allied fleets and long-dated deterrence programs that anchor production slots and supplier contracts. US awards for Virginia-class attack submarines and Columbia-class ballistic-missile submarines provide substantial backlog visibility, strengthening the supply base and supporting multi-year hiring plans essential to executing increased throughput within the naval vessels market. Surface combatants remain essential, yet capability is increasingly concentrated in fewer multi-mission platforms that rely more on integrated sensors and software-defined weapons than on incremental increases in hull count. Carriers progress on long schedules and continue to absorb significant capital, which keeps near-term growth led by submarines and advanced surface combatants. The strategic framing is that stealth, survivability, and magazine depth continue to dominate investment decisions, which align design and procurement with operational needs that extend beyond the current planning window for the naval vessels market.

The mix of vessel types is evolving as navies balance high-end deterrence with routine constabulary operations. Submarines benefit from multi-year contracts and specialized industrial capabilities, while surface fleets are optimized around fewer but more capable hulls that are designed for consistent upgrades. This approach allows navies to protect critical undersea advantages and still respond to day-to-day presence missions with more economical platforms where appropriate. The naval vessels market for submarines is supported by allied cooperation programs and industrial policy actions that seek to expand yard capacity and skilled labor pipelines, which underpin confidence in delivering planned boats to the fleet. Undersea modernization also catalyzes investment in sensors, communications, and power systems that spill over into surface combatant programs, which spreads the benefit across the platform ecosystem.

Marine engine platforms captured 28.55% of 2025 revenue, while sensor suites are projected to grow at an 8.17% CAGR through 2031 as navies focus on detection, tracking, and integrated fire control. Advanced radar systems are expanding the installed base, emphasizing digital beamforming, open architectures, and integrated combat-system software to enhance readiness and survivability. Increased demand for vertical launch capacity and communication upgrades supports cooperative engagement and distributed lethality. Command and control (C2) software, networked radios, and data links are becoming critical as they enhance the operational value of existing sensors and weapons, creating a durable aftermarket driven by recurring updates.

As software cadence accelerates, primes and integrators are adopting modular designs that reduce yard time and risk for retrofit programs. The market for advanced sensors is growing through both new ship installations and retrofits that replace legacy systems with active arrays and integrate new modes via software updates. Navies are also investing in cyber hardening and test environments to ensure new capabilities are deployed without compromising mission assurance. This shift reallocates budgets from heavy equipment to software and integration services, increasing the importance of sustainment contracts tied to availability and performance metrics.

Geography Analysis

North America retained 32.22% of the 2025 naval vessels market share, supported by large submarine programs and sustained modernization funding that prioritize undersea deterrence and high-end capability. The recent US contract awards for Virginia-class attack submarines and Columbia-class ballistic-missile submarines illustrate the magnitude and stability of the region's undersea investment footprint in the naval vessels market. As policymakers emphasize rebuilding shipbuilding capacity and maritime strength, new initiatives aim to expand industrial throughput, workforce pipelines, and financing tools that support yard modernization and supply chain resilience. These actions, combined with a focus on lifecycle sustainment and capability refresh, help offset schedule pressure on the largest programs and sustain overall demand for integration and aftermarket services in the naval vessels market.

Asia-Pacific is projected to deliver the fastest regional expansion, with a 7.54% CAGR to 2031, as allies reinforce undersea and surface capabilities to address evolving maritime security needs. The naval vessels market in Asia-Pacific benefits from allied cooperation frameworks and domestic industrial investment, which together support technology transfer, workforce training, and sustainment models tailored to local requirements. Regional buyers increasingly emphasize multi-mission surface ships and submarine acquisition or modernization to balance high-end deterrence with sovereignty patrols and constabulary tasks. Offset and co-production terms factor into awards and timelines, as governments seek to localize manufacturing and build long-term maintenance capability tied to domestic industry development. These requirements can lengthen first-article schedules but also add durable aftermarket and upgrade demand, strengthening the long-run outlook for the naval vessels market.

Europe continues to invest in next-generation frigates and submarine programs while coordinating across multiple national priorities, which can introduce schedule complexity but also share risk and deepen interoperability. Sanctions and export-control regimes affect supply chains and component sourcing for specific participants, which encourages diversification and enhanced compliance processes across cross-border programs in the naval vessels market. Major European primes maintain strong export positions in corvettes and OPVs, supported by product families designed for modular payloads and tailored combat systems that meet buyer cost and capability targets. Across the Middle East, Africa, and South America, procurement is more selective, with emphasis on patrol and surface combatant classes that address immediate security tasks and on sustainment partnerships that ensure availability within constrained budgets. The combined effect is continued regional diversity in vessel type mix and procurement pacing that sustains multi-year order visibility for the naval vessels market.

- General Dynamics Corporation

- ThyssenKrupp AG

- BAE Systems plc

- Naval Group

- EDGE Group PJSC

- Damen Holding B.V.

- HD Korea Shipbuilding & Offshore Engineering Co., Ltd.

- Huntington Ingalls Industries, Inc.

- Lockheed Martin Corporation

- Austal Limited

- FINCANTIERI S.p.A.

- Hanwha Ocean

- Larsen & Toubro Limited

- PT PAL Indonesia

- Navantia SA

- Kalashnikov Group

- Lurssen Werft GmbH & Co. KG

- China Shipbuilding Corporation Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 SSN/SSBN recapitalization and AUKUS accelerate undersea procurement

- 4.2.2 Grey-zone/coastal security boosts OPV, corvette, auxiliary demand

- 4.2.3 Multi-mission surface combatant upgrades (AAW/BMD, VLS, sensors)

- 4.2.4 Rapid integration of USV/UUV into hybrid fleet concepts

- 4.2.5 Lifecycle and digital sustainment contracts expand aftermarket

- 4.2.6 Co-production/local-content offsets unlock deals in emerging navies

- 4.3 Market Restraints

- 4.3.1 Cost overruns and long build cycles constrain new starts

- 4.3.2 Workforce and tier-2/3 supplier fragility delays deliveries

- 4.3.3 Export controls/sanctions complicate cross-border programs

- 4.3.4 Shipyard and dry-dock capacity bottlenecks cap throughput

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vessel Type

- 5.1.1 Destroyers

- 5.1.2 Frigates

- 5.1.3 Submarines

- 5.1.4 Corvettes

- 5.1.5 Aircraft Carriers

- 5.1.6 Other Vessel Types

- 5.2 By System

- 5.2.1 Marine Engine

- 5.2.2 Weapon Launch

- 5.2.3 Sensors

- 5.2.4 Navigation and Control

- 5.2.5 Communication

- 5.2.6 Others (Electrical, Auxiliary)

- 5.3 By Solution

- 5.3.1 Linefit

- 5.3.2 Retrofit

- 5.4 By Application

- 5.4.1 Search and Rescue

- 5.4.2 Combat

- 5.4.3 Mine Countermeasure (MCM)

- 5.4.4 Coastal

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Dynamics Corporation

- 6.4.2 ThyssenKrupp AG

- 6.4.3 BAE Systems plc

- 6.4.4 Naval Group

- 6.4.5 EDGE Group PJSC

- 6.4.6 Damen Holding B.V.

- 6.4.7 HD Korea Shipbuilding & Offshore Engineering Co., Ltd.

- 6.4.8 Huntington Ingalls Industries, Inc.

- 6.4.9 Lockheed Martin Corporation

- 6.4.10 Austal Limited

- 6.4.11 FINCANTIERI S.p.A.

- 6.4.12 Hanwha Ocean

- 6.4.13 Larsen & Toubro Limited

- 6.4.14 PT PAL Indonesia

- 6.4.15 Navantia SA

- 6.4.16 Kalashnikov Group

- 6.4.17 Lurssen Werft GmbH & Co. KG

- 6.4.18 China Shipbuilding Corporation Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment