PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644634

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644634

System Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

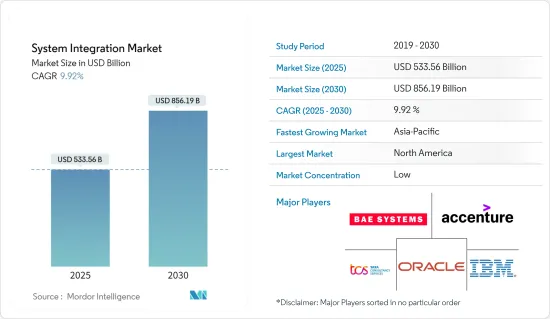

The System Integration Market size is estimated at USD 533.56 billion in 2025, and is expected to reach USD 856.19 billion by 2030, at a CAGR of 9.92% during the forecast period (2025-2030).

The system integration market is driven by the ongoing advancement and adoption of cloud technologies and increased demand from end-use industries because of increased productivity and less cost.

Key Highlights

- System Integration refers to combining multiple individual subsystems or sub-components into one more extensive system, allowing the subsystems to function together. Furthermore, system integration connects the organization with third parties, including customers, suppliers, and shareholders.

- The growing usage of cloud computing and the rapid growth of small and medium-sized organizations (SMEs) are propelling the global system integration market forward. Furthermore, the desire for low-cost and energy-efficient manufacturing processes is favorably impacting the growth of the system integration market.

- Furthermore, Cloud Integration has grown in popularity as the demand for the Software as a Service (SaaS) solution continues to increase. Cloud integration tools have opened new opportunities for organizations to connect disparate systems. The advantages of cloud integration include utility-style costing, the absence of a single point of failure, scalability, geographical independence, and the lack of hardware support, all contributing to cloud integration solutions and services being accepted and implemented. As a result, various businesses, including financial services and Software companies, use cloud computing.

- Several industry participants are partnering with small cloud providers in order to increase cloud usage. For instance, In April 2022, Google launched a Data Cloud Alliance in partnership with Accenture, Confluent, Databricks, Deloitte, Mongo DB, etc., to make data more portable and accessible across disparate business systems, platforms, and environments. Members of the alliance will provide infrastructure, APIs, and integration support to ensure data portability and accessibility between multiple platforms and products across various domains. To help enterprises migrate their databases, Google Cloud has partnered with system integrators and consulting firms such as TCS, Deloitte, Kyndryl, HCL, Wipro, Infosys, Cognizant, and Capgemini.

- System integration allows more intelligent organizational operations by bringing together different processes. As enterprise complexity has an impact on an organization's capacity to compete and generate profit, businesses are beginning to recognize the significance of system integration. Technologies for system integration offer businesses centralized, integrated, and cost-effective solutions for their IT infrastructure. One of the major factors propelling the expansion of the system integration market is the rise in information technology users. The U.S. Bureau of Labor Statistics predicts that employment in computer-related occupations will rise by 15% by 2031.

- However, a lack of client knowledge and business budgetary restraints are impeding the growth of the system integration industry. Also, The high cost associated with system integration makes it difficult for small and medium enterprises to switch to system integration, restraining market growth. On the contrary, technological advancements such as the integration of edge computing, the internet of things (IoT), and artificial intelligence are likely to provide lucrative prospects for system integration market expansion throughout the forecast period.

System Integration Market Trends

Software/Application Integration to have a Significant Growth

- Software integration is bringing together various types of software sub-systems to create a single unified system. Software integration can be required for several reasons, including setting up a data warehouse where data needs to be moved through an ETL process and linking various databases and file-based systems. Major organizations use software-as-a-service (SaaS) cloud-based solutions, enabling them to manage particular business processes without a hassle.

- The increasing need for automation technologies, cloud computing usage, and expanding broadband infrastructure are some of the key factors driving the growth of the software integration segment in the system integration market.

- Due to system integration, organizations can access and visualize data simultaneously for better decision-making. As a result, the adoption of cloud computing technology, the growth of broadband infrastructure, and the rising demand from businesses to improve the efficiency of their current systems are some of the key factors driving the market growth of the global integration software market. Also boosting industry expansion is growing consumer interest in virtualization.

- In March 2022, Cisco Systems, Inc. revealed that its new Cisco Intersight platform integrations with public cloud integration would enable Kubernetes clusters and virtual machines to be observable across several clouds. In addition, Cisco HyperFlex Hyper-Converged Infrastructure was introduced to increase edge computing and expand users' hybrid cloud capabilities. This would allow the organization to offer infrastructure and apps for cloud integrations more quickly.

- Sonata Software was also chosen in May 2023 to serve as the system integration partner for Bayer's new cloud-based agri-food solution. A company that specializes in implementing, planning, coordinating, scheduling, testing, and upgrading technological solutions is considered a System Integration partner. It essentially controls the complex IT solution's deployment to operation lifecycle.

North America to Hold Major Market Share

- North America held the largest market as a result of the expanding use of cloud-based services by large enterprises and the expanding use of IoT in industrial automation. The BFSI sector of the region has also embraced modern technology, which has enormous growth potential for the North American system integration market. In order to accomplish this, banks are working very hard to ensure that they meet every customer's needs.

- Also, the rising scalability among businesses and the widespread adoption of advanced technologies, such as big data, cloud-based services, and Software-as-a-Service (SaaS), have increased the complexity of operations in different organizations in the North American region.

- Consequently, there is a rise in demand for distributed information technology (IT) solutions, such as system integration, for streamlining different systems. Additionally, integrating Integration Platform as a Service (iPaaS) solutions expands system integration applications in the transportation and oil and gas industries. It allows sharing of integrated resources across multiple applications.

- Moreover, In June 2023, PortX, a provider of financial infrastructure and integration technology that offers Integration-Platform-as-a-Service (iPaaS), will release version 2.0 of its Integration Manager product. This is a significant update that is jam-packed with cutting-edge features made to improve control over digital core integration and streamline business processes. The API-driven process automation offered by Integration Manager 2.0 to FIs minimizes the stress on internal staff and offers a wide range of solutions not offered by core providers.

- Also, 70% of Bank of America's clients use digital services for their financial needs, the bank claims. It can aid the bank in expanding its clientele and maintaining its competitiveness in the market. During the projected period, there will be an increase in the demand for system integration services in the region as a result of organizations switching to these services.

- The region is witnessing various partnerships and collaborations as industries look to switch to system integration to increase productivity. For instance, In May 2022, Red Hat announced a partnership with General Motors to expand the development of software-defined vehicles at the edge and lay the foundation for broader electric vehicle adoption. This partnership will support various in-vehicle safety and non-safety-related applications, including driver assistance programs, infotainment, connectivity, and body control.

System Integration Industry Overview

The system integration market is significantly competitive, with several local and international players operating. With the market expected to broaden and yield more opportunities, more players are expected to enter the market gradually. The key players in the market studied include Accenture, IBM Corporation, and Wipro Limited. These players have adopted various growth strategies, such as mergers and acquisitions, new product launches, expansions, joint ventures, partnerships, and others, to strengthen their position in this market.

- April 2022 - Bruker Corporation announced the acquisition of Optimal Industrial Automation and Technologies, a software and system integration company. The Optimal biopharma tools acquisition strengthens Bruker as a key software and solutions provider for small molecule, biologics, and new drug modalities pharma companies.

- February 2022 - Ansys and AWS announced a strategic partnership. The collaboration will enable the deployment of Ansys products on AWS - making simulation workloads more user-friendly while offering scalability and flexibility with easy access to software and storage solutions from anywhere with a web browser.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the impact of COVID-19 on the Market

- 4.5 Market Drivers

- 4.5.1 Advancements and adoption of cloud-technologies

- 4.5.2 Benefits of increasing productivity while reducing IT Management cost

- 4.6 Market Challenges

- 4.6.1 High cost associated with system integration

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Infrastructure Integration

- 5.1.2 Software/Application Integration

- 5.1.3 Consulting

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 IT and Telecom

- 5.2.4 BFSI

- 5.2.5 Healthcare

- 5.2.6 Oil and Gas

- 5.2.7 Others (Energy, Chemical, Mining etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.3 Asia

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Accenture

- 6.1.2 IBM Corporation

- 6.1.3 Tata Consultancy Services Limited

- 6.1.4 Oracle Corporation

- 6.1.5 BAE systems

- 6.1.6 Wipro Limited

- 6.1.7 Cognizant

- 6.1.8 Deloitte Touche Tohmatsu Limited

- 6.1.9 Infosys Limited

- 6.1.10 MDS Systems Integration (MDS SI)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS