PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692537

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692537

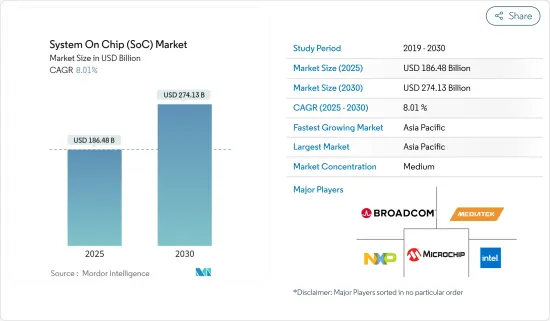

System On Chip (SoC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The System On Chip Market size is estimated at USD 186.48 billion in 2025, and is expected to reach USD 274.13 billion by 2030, at a CAGR of 8.01% during the forecast period (2025-2030).

System-on-chip (SoC) technology has become an integral part of modern technology, revolutionizing the way electronic devices are designed and manufactured. Basically, a system-on-a-chip, or SoC, integrates all the components of a computer onto a single chip, including CPU, memory, input and output ports, and secondary storage.

Key Highlights

- Rapidly evolving technologies, including 5G and 6G, software-packed vehicles, non-terrestrial networks (NTN), and digital healthcare, endless imagination, and invention across industries have been significantly paving the way for SoC to enter the consumer market rapidly. SoCs have long been incorporated into electronic devices such as tablets and mobile phones because they are compact and power-efficient.

- Today, SoCs are increasingly being used in the Internet of Things devices and other devices. The rising demand for smart and power-efficient devices by consumers and exponential adoptions of IoT by various industry verticals are expected to be driving factors for the players in the semiconductor market, thus boosting the growth of the SoC market.

- Another important trend in the electronics industry is the increase of the Internet of Things (IoT). With the rise in demand for smart devices, IoT has become an essential part of everyday life. Thus, businesses are primarily using this technology to develop new products and services. SoCs will also play a pivotal role in the advancement of flexible electronics, enabling new form factors for wearable and implantable devices.

- As technology continues to evolve, several industries are adopting automation and digitization, thereby bringing new opportunities to the key players for entering new markets but with high initial research and development costs associated with the system on a chip (SoC). Owing to the increasing customization of SoC for various products, the players need to focus on various R&D projects simultaneously, increasing their project costs. Such factors are expected to hamper the market growth over the forecast period.

- While COVID-19 changed consumer spending patterns by increasing the demand for consumer electronics, the automotive industry's move toward electric vehicles is also boosting the need for chips. For instance, a typical gasoline engine car uses about 50 to 150 semiconductor chips, but an electric vehicle can use up to 3,000 semiconductor chips. The growing emphasis on electric vehicle manufacturing is certain to consume vastly more semiconductor chips in the future, thus driving the role of SoC in the global market.

System On Chip Market Trends

Consumer Electronics Segment to Occupy a Significant Share

- The incorporation of SoCs facilitates improved efficiency, decreased energy usage, and compactness, rendering SoCs essential for numerous consumer electronics applications ranging from smartphones to various interconnected devices. Consumer electronics is projected to witness a significant demand for SoCs based on their application. This is primarily attributed to the increasing adoption of smartphones due to the growing disposable incomes of consumers.

- Consumer electronics such as premium smartphones, intelligent speakers, tablets, wearables, and other devices extensively employ edge AI chips. These chips are specifically crafted to augment the computational capabilities and effectiveness of AI algorithms at the network's edge, enabling quicker and real-time decision-making capabilities. The rising demand for AI chip technology is anticipated to propel market expansion throughout the projected timeframe. Furthermore, the escalating adoption of AI technology and the proliferation of IoT-connected consumer devices are poised to amplify the growth of the market.

- Moreover, the market growth is primarily driven by the expanding presence of the internet and smartphone users, the widespread utilization of cloud computing and IoT-enabled platforms, and the extensive deployment of wireless sensors in smart infrastructure. As the market continues to witness a rise in the number of IoT and smart devices, the demand for SoC chips is also anticipated to grow at a comparable rate due to their diverse applications in these devices. As a result, several vendors in the market are constantly investing in introducing significant products catering to the rising demand for connectivity in consumer electronics.

- The increasing investments in the consumer electronics industry across several countries are expected to enhance the market opportunities. Several governments across the world are constantly encouraging new investments into the country to set up electronics manufacturing facilities and aiming to enhance their production capabilities. The increasing mobile penetration, increasing internet connectivity, and the growing popularity of connected devices are expected to drive the growth of consumer electronics. Such significant capabilities preferred in several consumer electronics devices such as Mobile devices, PCs, Tablets, Audio Devices, and others are expected to drive the market.

- As stated by Ericsson, the worldwide tally of smartphone mobile network subscriptions came close to 6.4 billion in 2022 and is estimated to exceed 7.7 billion by 2028. It is worth mentioning that China, India, and the United States emerge as the countries with the most significant number of smartphone mobile network subscriptions. Ericsson's report emphasizes that although the sales reached a plateau in 2022, the increasing average selling price of smartphones is expected to strengthen the market in the coming years. These remarkable developments are set to enhance the market's prospects.

Asia-Pacific Expected to Dominate the Market

- The Asia-Pacific region is anticipated to dominate the market studied because it currently dominates the global semiconductor market, which is further supported by government policies. According to SIA, China, Japan, Taiwan, and South Korea account for about 75% of the world's semiconductor production collectively, and other countries like Vietnam, Thailand, Malaysia, and Singapore also make significant contributions to the region's market dominance.

- With the increasing demand for technologically advanced devices in every industry, the demand for SoC devices in the market is expected to increase further. Furthermore, the increasing applications of a wide range of sensors in the automotive and smartphone market are expected to increase the demand for sensors further.

- Furthermore, the government's Made in China 2025 initiative is helping to expand the power electronics market. Additionally, the industry is bringing in fresh funding for power electronics in the area. For instance, a significant manufacturer of wide-bandgap compound semiconductors, IIVI Incorporated, increased the size of its SiC wafer finishing manufacturing facility in China.

- In line with this launch, the company aims to power its next-generation products for 5G build-out, including the next-generation 5G Compact Macro, baseband units, and Massive MIMO radios.

System On Chip Industry Overview

The system-on-chip (SoC) market is semi-consolidated due to the presence of domestic and global players. Major players use various strategies, such as product launches, agreements, and acquisitions, to increase their footprints in the market. The key players in the market are Broadcom Inc., Intel Corporation, MediaTek Inc., Microchip Technology Inc., and NXP Semiconductors NV.

- In September 2023, GlobalFoundries and Microchip Technology, through Microchip's subsidiary Silicon Storage Technology (SST), have recently unveiled the SST ESF3 third-generation embedded SuperFlash technology NVM solution. This cutting-edge solution is now available for production in the GF 28SLPe foundry process. Customers of GF have expressed their satisfaction with the remarkable performance, exceptional reliability, wide range of IP options, and cost efficiency offered by this solution. It has proven to be the perfect fit for advanced MCUs, intricate smart cards, and IoT chips used in both consumer and industrial applications.

- In May 2023, STM launched single-chip ICs with antenna matching for STM32 MCUs and BLE SoCs. STMicroelectronics revealed its latest line of single-chip antenna-matching ICs that facilitate innovation speed for Bluetooth LE System of Chips and two STM32 microcontrollers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of Emerging Technologies Like IoT and AI

- 5.1.2 Increasing Investments in 5G and Growing Demand for 5G Smartphones

- 5.2 Market Restraints

- 5.2.1 High Initial Costs of R&D

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Analog

- 6.1.2 Digital

- 6.1.3 Mixed

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Communications

- 6.2.3 Automotive

- 6.2.4 Computing and Data Storage

- 6.2.5 Industrial

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Intel Corporation

- 7.1.3 Mediatek Inc.

- 7.1.4 Microchip Technology Inc.

- 7.1.5 NXP Semiconductors NV

- 7.1.6 Qualcomm Incorporated

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 STMicroelectronics NV

- 7.1.9 Toshiba Corporation

- 7.1.10 Apple Inc.

- 7.1.11 Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- 7.1.12 Texas Instruments Incorporated

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS