Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693449

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693449

Alfalfa Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 415 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

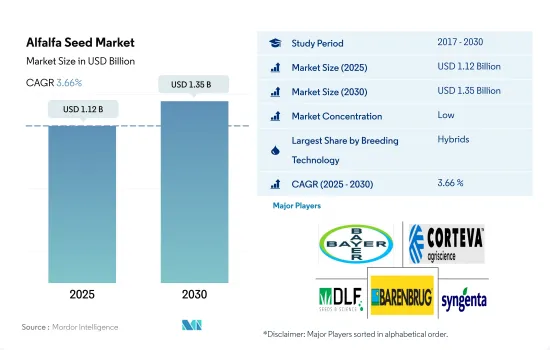

The Alfalfa Seed Market size is estimated at 1.12 billion USD in 2025, and is expected to reach 1.35 billion USD by 2030, growing at a CAGR of 3.66% during the forecast period (2025-2030).

The increased adoption of hybrid seeds due to their improved traits such as disease resistance are driving the market.

- The livestock population is increasing across various regions around the world. The increase in livestock population needs an expansion of the area under forages, and alfalfa offers easily digestible fiber content. These are some of the major factors leading to the growth of the hybrid and open-pollinated alfalfa seed market.

- The hybrid segment tops the alfalfa seed market due to the increased adoption of hybrid varieties and increasing awareness about their benefits. The hybrid alfalfa seed market value is projected to increase by about 35.9% and reach USD 1.1 billion by the end of the forecast period. This is due to the rise in the seed replacement rate and the availability of improved varieties in the market.

- Increasing acceptance of advanced hybrid technology by growers, such as drought tolerance and disease resistance, is projected to contribute to hybrid alfalfa seed market growth in the coming years. For instance, in the United States, hybrids occupied 99% of the area under commercial seeds in 2022, which is attributed to the availability of high-yielding hybrid varieties and the development of transgenic alfalfa varieties from popular companies such as Allied Seed LLC, Bayer AG, and DLF.

- Africa is forecasted to be the fastest growing market in the OPVs segment at a CAGR of 3.2% because a small group of farmers in the country is projected to use OPVs over hybrids as they require fewer inputs, such as fertilizer and pesticides and are less expensive and more affordable for small holding and low-income farmers.

- Therefore, an increase in the cultivation area under commercial seeds and the demand from cattle growers for quality forage with more protein and digestible fiber content is projected to boost the market for hybrid seeds during the forecast period.

The increasing demand for alfalfa from livestock industry combined with growing cultivation area driving the market.

- Europe is the largest alfalfa seed market in the world. It accounted for about 41.1% of the global alfalfa seed market in 2022, with 3.2 million hectares under alfalfa cultivation. Italy was the largest producer and occupied a large area of alfalfa production in Europe. As there is a significant demand for better-quality meat, increased livestock production is likely to create a demand for better forage crops such as alfalfa, driving the market for alfalfa forage seeds in the region.

- In 2022, North America was the largest market in the global alfalfa seed market, with a share of about 29.0% of the global market due to the highest production, globally, weather conditions, and increased demand by dairy farmers. Canada has the greatest demand in the region because of the increase in demand for crops as feed, the increase in cultivation area, and high profitability.

- In Asia-Pacific, alfalfa is an important forage crop as the weather is favourable and demand for high protein feed is more from the livestock and cattle rearers in the region. The market share of the region was 16.5% in 2022, which is expected to increase at a CAGR of 2.4% during the forecast period as the adoption of alfalfa is increasing among farmers.

- South America accounted for about 6.5% of the global alfalfa seed market in 2022. The area cultivated has increased from 3.9 million hectares in 2017 to 4.4 million hectares in 2022. This increase in cultivation area is anticipated to drive the market at a CAGR of 3.0% during the forecast period.

- The increasing area under cultivation and rising demand for forage are the major factors anticipated to help in the growth of the alfalfa seed market.

Global Alfalfa Seed Market Trends

North America and Asia Pacific dominated the area under cultivation of alfalfa with increased livestock population

- Alfalfa is one of the major crops cultivated globally due to the high demand from the feed processing industry to feed livestock, especially cattle. To meet this high demand for alfalfa-based feed, the area cultivated for alfalfa was 31.5 million hectares in 2022, which increased by 4.5% during 2017-2022. Moreover, the crop accounted for 39.2% of the area under cultivation of forage crops in 2022.

- North America has a higher area under cultivation of alfalfa in 2022, with 11.5 million hectares, which increased by 5.5% during 2017-2022. The increase in area is attributed to the increasing investments and support from the Canadian government to increase the region's feed production and livestock population. For instance, ruminant population increased by 1.9% from 2017 to 2022, with the number of buffaloes and cattle rising from 155.1 million to 158.6 million during the same period.

- In Asia-Pacific, the area under alfalfa cultivation was 6.4 million hectares in 2022. Major Alfalfa growing countries in the region are China, Australia, and India. Among these, China held the major market share, which accounted for 76.8% of the area under Asia-Pacific alfalfa cultivation in 2022.

- The government developed an action plan in China to enhance dairy and alfalfa production. It provided USD 71.3 million in support programs to develop 33.0 thousand hectares of alfalfa alongside a subsidy of USD 86.11 per square meter for alfalfa farms over 200 hectares. Thus, these measures increase the cultivation of alfalfa in the region.

- Due to an increase in livestock population and rising demand for dairy products, the cultivation area has been increasing.

Rising adoption of disease resistant, wider adaptability, and drought resistant alfalfa seeds for high yield during adverse climatic conditions

- Globally, alfalfa is a majorly cultivated forage crop. The high-demand traits of the crop are disease-resistant, insect-resistant, and wider adaptability for improving the quality of the feed/silage for the livestock industry. Furthermore, other traits such as increasing protein content, growing throughout the seasons, and reducing lignin content are expected to gain popularity in the future for increasing forage quality.

- Wider adaptability is the most adopted trait in the global market, especially South America, as it accounted for 35.4% in 2022 in the region. It was most adopted because of the changing agro-climatic conditions, field stress, and growing crops in different regions. Companies such as Bayer, DLF, and Barenbrug have developed different alfalfa varieties in the United Kingdom, such as DKC 3218, DKC 3204, Debalto, and Marcamo. These varieties can withstand diverse environmental conditions, adapt to various soil types, and withstand field stress and heat conditions. Furthermore, the EU Commission's REFORMA project (2016-2020) aims to develop advanced breeding techniques and introduce new alfalfa cultivars.

- Disease tolerance, high starch content, and drought tolerance are other traits in high demand. Ampac Seed Company (Attention II), Land O'Lakes (Round-up Ready), KWS SAAT SE & Co. KGaG (HarvXtra, Standfast), Bayer Crop Science (DEKALB), Syngenta AG (NEXGROW), and DLF (Fortune) are companies proving seed varieties that have resistance to diseases such as Colletotrichum trifolii, and verticillium wilt. Factors such as the increased demand for improving animal feed, many benefits such as disease resistance, and increasing yield are expected to drive the market's growth during the forecast period.

Alfalfa Seed Industry Overview

The Alfalfa Seed Market is fragmented, with the top five companies occupying 39.27%. The major players in this market are Bayer AG, Corteva Agriscience, DLF, Royal Barenbrug Group and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92511

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Ghana

- 5.2.1.2.4 Kenya

- 5.2.1.2.5 Nigeria

- 5.2.1.2.6 South Africa

- 5.2.1.2.7 Tanzania

- 5.2.1.2.8 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Japan

- 5.2.2.2.6 Myanmar

- 5.2.2.2.7 Pakistan

- 5.2.2.2.8 Philippines

- 5.2.2.2.9 Vietnam

- 5.2.2.2.10 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Saudi Arabia

- 5.2.4.2.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.5.2.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ampac Seed Company

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 DLF

- 6.4.5 KWS SAAT SE & Co. KGaA

- 6.4.6 Land O'Lakes Inc.

- 6.4.7 RAGT Group

- 6.4.8 Royal Barenbrug Group

- 6.4.9 S&W Seed Co.

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.