Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1440552

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1440552

Africa Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2028)

PUBLISHED:

PAGES: 80 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

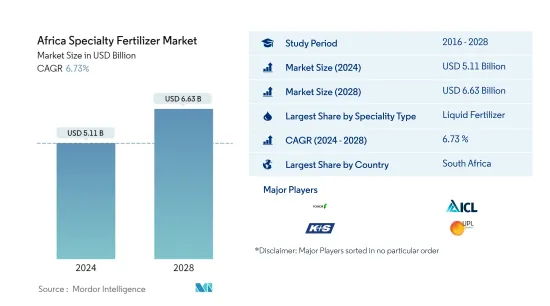

The Africa Specialty Fertilizer Market size is estimated at USD 5.11 billion in 2024, and is expected to reach USD 6.63 billion by 2028, growing at a CAGR of 6.73% during the forecast period (2024-2028).

Key Highlights

- Largest segment by Speciality Type - Liquid Fertilizer : The demand for liquid fertilizer in the Africa region keeps up, as the soils in the region are dry and liquid fertilizers ensures that easy absorbtion by the plants.

- Fastest growing by Speciality Type - Water Soluble : The watersoluble fertilizer absorption rate is more than double compared to conventional fertilizers reaching an efficiency of about 80-90% and reducing total fertilizer use.

- Largest Segment by Crop Type - Horticultural Crops : horticulture crops are cultivated year-round and have better irrigation systems like sprinkler and drip irrigation, which continue to require specialty fertilizers.

- Largest segment by Country - South Africa : Nigeria has large agricultural area in the region, it acccounts for about 35% of the total crop area in the region and has some of the largest fertilizer production units.

Africa Specialty Fertilizer Market Trends

Liquid Fertilizer is the largest segment by Speciality Type.

- Specialty fertilizers accounted for 42% of the total African fertilizer market value, which was valued at USD 20.17 billion in 2021. There is an increasing trend observed in the adoption of specialty fertilizers due to their higher efficiency. However, specialty fertilizers are higher priced compared to conventional fertilizers.

- Water-soluble fertilizers dominated the specialty fertilizers segment in the region and accounted for 46% of the total specialty fertilizer market value, valued at USD 9.41 billion in 2021. Water-soluble fertilizers can be applied through foliar, fertigation, and soil method of application based on the requirement.

- Liquid fertilizers occupied the second-largest market share in the specialty fertilizer market value. It accounted for 43.77% of the total African specialty fertilizer market value, valued at USD 8.82 billion in 2021. It is observed that liquid fertilizers have had constant growth in consumption volume since 2017.

- Controlled-release fertilizers accounted for 6.81% of the total specialty fertilizer market value, valued at USD 1.37 billion in 2021. Field crops dominated the controlled-release fertilizers market and accounted for 92% of the total market value in 2021.

- Slow-release fertilizer market accounted for 2.73% of the total African specialty fertilizer market value in 2021, and it is a highly fragmented market in the region.

- The advantages of using specialty fertilizers, like a reduced rate of application, the precise release of nutrients, and other economic benefits to the farmer, are anticipated to drive the specialty fertilizer market in the region during the forecast period.

South Africa is the largest segment by Country.

- Rest of Africa accounted for 90% of the value of the African specialty fertilizer market. Rest of Africa's specialty fertilizer market is dominated by water-soluble fertilizers contributing to 46.51%, followed by liquid fertilizers at 43.12%, controlled-release fertilizers at 7.34%, and slow-release fertilizers contributing to 3.01% of total value in 2021. The coated-type controlled-release fertilizers market is anticipated to grow faster with increased awareness among farmers.

- Subsistence farming is practiced throughout the rest of Africa. Micronutrient insufficiency is frequently misdiagnosed or disregarded because of a lack of resources, particularly fertilizers. The supply of fertilizer is growing, and commercial planting is expanding as a result of farmers' rising affordability. In 2021, the micronutrient value in the other African nations totaled USD 906 million. Therefore, it is anticipated that during the forecast period, the region will increase.

- In Nigeria, specialty fertilizers market liquid fertilizers accounted for 49.56%, followed by water-soluble fertilizers at 48.40%, controlled-release fertilizers at 1.78%, and slow-release fertilizers contributed 0.24% to the total value of specialty fertilizers in 2021.

- Field crops accounted for 79.27% of the specialty fertilizers market in South Africa, followed by turf and ornamental crops at 17.48% and horticulture crops at 3.24% in 2021. South Africa's major field crops include corn, soybeans, wheat, and rapeseed/canola.

- Due to repeated cropping without sufficient time for the soil to regain its fertility, African soils are becoming unsuitable for cultivation. The market will be driven by specialty fertilizers that provide timely nutrition while having a low environmental impact.

Africa Specialty Fertilizer Industry Overview

The Africa Specialty Fertilizer Market is fragmented, with the top five companies occupying 34.19%. The major players in this market are Foskor, ICL GROUP LTD, K+S AKTIENGESELLSCHAFT, UPL Limited and Yara International ASA, (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92604

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.2 Average Nutrient Application Rates

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Nigeria

- 5.4.2 South Africa

- 5.4.3 Rest Of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Foskor

- 6.4.2 Gavilon South Africa

- 6.4.3 Haifa Group Ltd

- 6.4.4 ICL GROUP LTD

- 6.4.5 K+S AKTIENGESELLSCHAFT

- 6.4.6 Kynoch Fertilizer

- 6.4.7 Omnia Nutriology

- 6.4.8 UPL Limited

- 6.4.9 Yara International ASA,

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.