PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907280

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907280

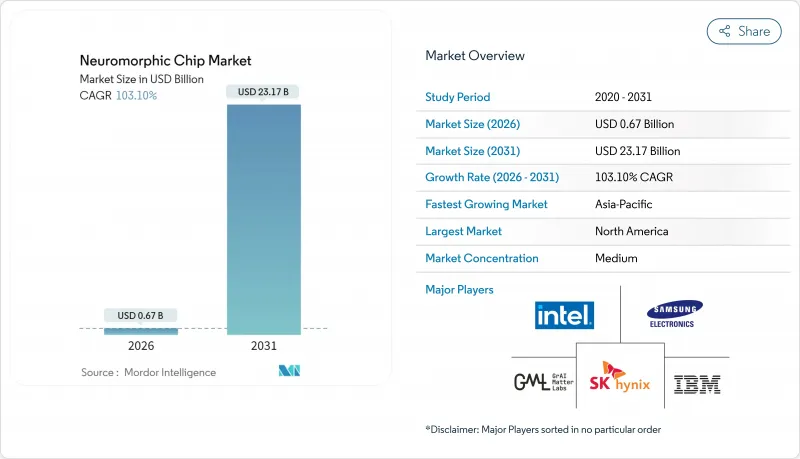

Neuromorphic Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The neuromorphic chip market was valued at USD 0.33 billion in 2025 and estimated to grow from USD 0.67 billion in 2026 to reach USD 23.17 billion by 2031, at a CAGR of 103.1% during the forecast period (2026-2031).

The neuromorphic chip market is accelerating because brain-inspired processors overcome the von Neumann bottleneck, unlock extreme energy efficiency, and enable real-time decision-making at the network edge. Edge artificial intelligence in smartphones and vehicles, mounting data-center electricity costs, and rising government funding for brain-inspired R&D collectively create a flywheel that keeps capital and talent flowing into new product launches. Automotive advanced driver-assistance systems (ADAS) currently absorb the largest commercial volumes, while healthcare, industrial IoT, and aerospace applications provide additional demand diversity. Competition remains intense because no single architecture, analog, digital, or mixed-signal, has emerged as a de facto standard, pushing vendors to differentiate through proprietary memory technologies, software stacks, and domain-specific optimizations.

Global Neuromorphic Chip Market Trends and Insights

Rising Edge-AI Demand in Consumer and Automotive

Smartphones built on Qualcomm's Snapdragon 8 Gen 3 now perform 45 TOPS on-device, eliminating cloud latency and inspiring similar architectures for in-car perception systems. Automotive OEMs adopt neuromorphic processors to meet millisecond response targets and stringent thermal envelopes, a shift that lowers battery drain by double-digit margins during ADAS operation.

Data-Center Energy Crisis Favoring Ultra-Low-Power Compute

Global data centers consumed 176 TWh in 2023, and AI inference workloads threaten to double electricity demand by 2028. IBM's NorthPole chip proves neuromorphic hardware can deliver 25-fold energy savings over GPUs while sustaining similar accuracy. Hyperscalers now pilot hybrid racks that pair Loihi 2 clusters with conventional accelerators to curb spiraling utility bills.

Immature Software and Toolchain Ecosystem

Developers juggle Nengo, Lava, and MetaTF because no unified compiler spans every hardware platform, inflating project timelines and integration costs. Enterprise IT teams hesitate until a CUDA-like standard emerges, dampening short-term procurement.

Other drivers and restraints analyzed in the detailed report include:

- Government Brain-Inspired R&D Programs

- Event-Driven Sensor-SoC Integration Wave

- Fabrication Variability of Analog NVM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mixed-signal devices, though representing a smaller base, will compound at 105.2% to become the principal growth engine for the neuromorphic chip market. Their hybrid analog-digital topology captures continuous synaptic dynamics more naturally than purely digital logic, yet still leverages CMOS toolflows for scale. Digital chips preserved a 43.62% neuromorphic chip market share in 2025, owing to mature EDA support and easier software portability. The neuromorphic chip market size allocated to digital products is projected to expand, but its relative weight will slip as mixed-signal gains traction. Vendors such as Samsung pursue mixed-signal for mobile AI inference, while start-ups refine analog blocks for micro-watt sensor nodes. Investment gravitates toward process-compatible resistive memory arrays that shrink synapse footprints and cut refresh overhead.

Mixed-signal's momentum reflects its capacity to deliver real-time edge intelligence at sub-100 mW levels, enabling autonomous drones, smart ear buds, and implantable medical devices. Carbon-based ternary logic prototypes unveiled in 2025 illustrate how material innovation could further compress area and energy envelopes. Digital incumbents respond by integrating on-chip SRAM to reduce data shuttling penalties, yet must match analog's dynamic range and locality advantages. As foundries refine process recipes, mixed-signal yield headwinds will abate, positioning the category to erode digital's dominance through 2031.

Spiking neural networks commanded 36.35% of 2025 revenue thanks to software familiarity, but ReRAM crossbars are on track for a 104.8% CAGR, the fastest within the neuromorphic chip market. Crossbar arrays store multi-bit weights in-memory, fusing compute and storage to minimize data movement. Proof-of-concept systems achieved 94.6% MNIST accuracy while consuming single-digit milliwatts. The neuromorphic chip market size tied to spiking neurons will still expand in absolute terms, though its share slides as resistive devices scale. Phase-change memory holds a supporting role for endurance-critical workloads.

The architecture shift also signals a broader move from neuron-centric to memory-centric design; DenRAM diagrams encode temporal dynamics directly in resistive states, improving sequence learning. Spiking networks, however, retain an edge in sparse event processing, keeping them attractive for vision sensors and radar. Industry roadmaps increasingly propose heterogeneous chips that combine these paradigms on a single interposer, accelerating software reuse and system integration.

The Neuromorphic Chip Market Report is Segmented by Chip Type (Analog, Digital, Mixed-Signal), Architecture (Spiking Neural Network, ReRAM-Based Architectures, and More), End-User Industry (Automotive, Industrial IoT & Robotics, and More), Deployment Model (Edge Devices, Data-centre/Cloud), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 34.85% neuromorphic chip market share in 2025 on the back of DARPA funding and Intel's 1.15 billion-neuron Hala Point platform. The region hosts robust academic-industry linkages; MIT's integrated photonic processor completed neural computations in sub-nanosecond intervals while retaining more than 92% accuracy, signaling future spin-outs into commercial stacks. Canadian tooling expertise, highlighted by Nengo software, further entrenches the ecosystem's maturity and draws venture capital to Silicon Valley start-ups.

Asia-Pacific, though smaller in absolute terms, is the neuromorphic chip market's fastest-growing territory with a forecast 104.7% CAGR to 2031. China's Darwin Monkey system offers 2 billion neurons across 960 Darwin 3 chips, demonstrating the state's commitment to strategic autonomy in AI hardware. South Korea's EUR 5 million EU partnership advances spintronic semiconductors, while Japanese consortia pair phase-change memory with edge cameras for factory automation. India's national photonic-chip initiative and Singapore's neuromorphic robotics labs round out the region's diversified R&D map.

Europe remains a pivotal secondary hub, channeling Horizon funds into resistive memory and event-driven vision research. German automakers spearhead ADAS pilots that integrate Spiking Neural Network coprocessors, leveraging local tier-ones for vehicle-grade packaging. Swiss firm SynSense supplies sub-1 mW DSP blocks to European drone OEMs, underscoring cross-border supply-chain synergies. Regulatory leadership in privacy and sustainability influences global design targets, nudging chipmakers toward transparent power reporting and on-device data retention.

- Intel Corporation

- International Business Machines Corporation

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- BrainChip Holdings Ltd

- SynSense AG

- GrAI Matter Labs SAS

- Nepes Corporation

- Qualcomm Technologies, Inc.

- Micron Technology, Inc.

- Synaptics Incorporated

- Innatera Nanosystems BV

- Prophesee SA

- MemryX Inc.

- Mythic Inc.

- Syntiant Corp.

- Gyrfalcon Technology Inc.

- Applied Brain Research Inc.

- General Vision Inc.

- Vicarious Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising edge-AI demand in consumer and automotive

- 4.2.2 Data-center energy crisis favouring ultra-low-power compute

- 4.2.3 Government brain-inspired R&D programmes

- 4.2.4 Event-driven sensor-SoC integration wave

- 4.2.5 On-board satellite AI processing need

- 4.2.6 OT-cybersecurity anomaly detection requirements

- 4.3 Market Restraints

- 4.3.1 Immature software and toolchain ecosystem

- 4.3.2 Fabrication variability of analog NVM

- 4.3.3 Lack of spike-system test/validation standards

- 4.3.4 Unclear medical-device regulatory path

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Emerging Use-Cases for Neuromorphic Chips

- 4.9 Impact of Macroeconomic Trends on the Market

- 4.10 Investment Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chip Type

- 5.1.1 Analog

- 5.1.2 Digital

- 5.1.3 Mixed-Signal

- 5.2 By Architecture

- 5.2.1 Spiking Neural Network

- 5.2.2 ReRAM-based Architectures

- 5.2.3 Phase-Change-Memory Architectures

- 5.3 By End-User Industry

- 5.3.1 Automotive (ADAS / AV)

- 5.3.2 Industrial IoT and Robotics

- 5.3.3 Consumer Electronics

- 5.3.4 Financial Services and Cybersecurity

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Aerospace and Defense

- 5.4 By Deployment Model

- 5.4.1 Edge Devices

- 5.4.2 Data-centre / Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 International Business Machines Corporation

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 SK hynix Inc.

- 6.4.5 BrainChip Holdings Ltd

- 6.4.6 SynSense AG

- 6.4.7 GrAI Matter Labs SAS

- 6.4.8 Nepes Corporation

- 6.4.9 Qualcomm Technologies, Inc.

- 6.4.10 Micron Technology, Inc.

- 6.4.11 Synaptics Incorporated

- 6.4.12 Innatera Nanosystems BV

- 6.4.13 Prophesee SA

- 6.4.14 MemryX Inc.

- 6.4.15 Mythic Inc.

- 6.4.16 Syntiant Corp.

- 6.4.17 Gyrfalcon Technology Inc.

- 6.4.18 Applied Brain Research Inc.

- 6.4.19 General Vision Inc.

- 6.4.20 Vicarious Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment