PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445504

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445504

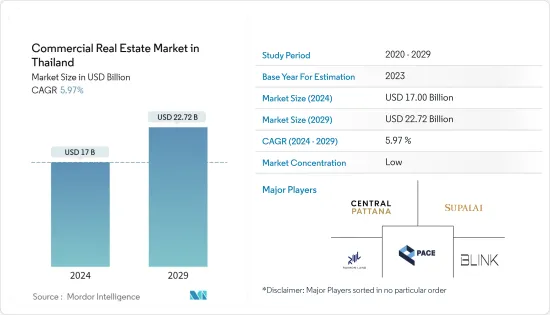

Commercial Real Estate in Thailand - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Commercial Real Estate Market in Thailand Market size is estimated at USD 17 billion in 2024, and is expected to reach USD 22.72 billion by 2029, growing at a CAGR of 5.97% during the forecast period (2024-2029).

Key Highlights

- The cost of living and office space is among the lowest in Thailand. With the trend of an active workplace, the office real estate market in Bangkok is evolving, and co-working spaces significantly impact the city's ability to lease significant quantities of office space.

- Older office buildings will be under pressure to modernize and upgrade due to the incoming new supply to remain competitive in the shifting market. Bangkok also has the best cost of living and level of development in the area. Over 7,400 hotel keys are planned to be completed by the end of 2022, which may increase the supply of hotel keys in Bangkok by 6.7%.

- The demand for modern logistics properties (MLPs) in Thailand rose due to the growth of already-established businesses and the introduction of new businesses in the logistics sector. The need for logistics real estate in Thailand increased due to the rapid rise of e-commerce. The average occupancy rate of all industrial estates in Thailand is approximately 90%. Foreign nationals who wish to permanently emigrate to Thailand and ex-pats who are applying for work visas continue to grow in number. The Thai real estate market has been on a rising trend for more than 10 years.

Thailand Commercial Real Estate Market Trends

Growth in Tourism is Driving the Market

With Thailand's key tourism sector reopening, the country's economy grew by 1.2% in 2021, exceeding the Finance Ministry's previous forecast of 1%. In November 2021, the country started welcoming vaccinated visitors, which boosted its economic activity in the fourth quarter. The Ministry predicted that growth in 2022 could reach 4.5%, exceeding its previous forecast of 4%.

With a stronger grip on the outbreak and an expected global economic recovery in 2022, the government has been aiming to support growth through measures to boost consumption, exports, private investment, public spending, and business recovery. So far, the government's spending to support the economy has amounted to 14.6% of the GDP.

Compared to other nations in the region, such as Mainland China, Singapore, and Hong Kong, Thai real estate is relatively reasonably priced. Buyers from these nations continue to find Thailand, particularly Bangkok, a desirable location to purchase real estate.

Recovery of Bangkok's Office Space Driving the Market

Office landlords are reviewing their product offerings and amenities to meet the shifting demand as a result of the increased market competition. Given that many tenants see coworking space as a crucial amenity in the building, potential collaborations with coworking space operators will enhance the property's value offer. When office supply and vacancy rates rise, tenants may have more negotiating leverage for better rents and terms because landlords may want to prioritize occupancy above rentals. Tenants may have more options and be able to choose the space best suited for their needs from the range of high-quality new office buildings for the first time in many years.

As nine new projects were completed in the second half of 2021, another 175,800 sq. m of office space is expected to enter the market. CBD may account for roughly 60% of the anticipated new supply. In comparison, if launches in Q3 2021-Q3 2026 go as planned, Bangkok's office market supply may increase by 1.67 million sq. m or 302,000 sq. m per year.

Take-up increased by 61% Q-o-Q to 78,000 sq. m, indicating that leasing activity is improving. This level of take-up is higher than the 10-year average of 67,000 sq. m per quarter. Meanwhile, 57,100 sq. m of space was vacated, marking the fourth consecutive quarter of growth. Net absorption of 21,000 sq. m was recorded as take-up exceeded the amount of space vacated, marking the first quarter in which net absorption was positive since Q1 2020.

Following the third wave of COVID-19, the remote working trend became even more significant. A combination of core + flex space and remote working may define the future of workplaces. As a result, no significant drop in demand for office space is expected in the medium to long term.

Thailand Commercial Real Estate Industry Overview

The Thai commercial real estate market is fragmented due to the presence of many players in the country. Some of the major real estate players in the market are Central Pattana PLC, Sansiri Public Co. Ltd, Pace Development Corporation PLC, and Raimon Land PCL.

The market is expected to grow during the forecast period due to continued economic growth and increased demand for commercial real estate in metropolitan cities. Other factors like demand for office spaces and growth in tourism may also drive the market. Industrial estate developers are more likely to focus on investments or develop new phases or projects in the future.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Current Market Scenario

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Government Initiatives and Regulatory Aspects for the Commercial Real Estate Sector

- 4.7 Insights on Existing and Upcoming Projects

- 4.8 Insights on Interest Rate Regime for General Economy and Real Estate Lending

- 4.9 Insights on Rental Yields in the Commercial Real Estate Segment

- 4.10 Insights on Capital Market Penetration and REIT Presence in Commercial Real Estate

- 4.11 Insights on Public-private Partnerships in Commercial Real Estate

- 4.12 Insights on Real Estate Tech and Start-ups Active in the Real Estate Segment (Broking, Social Media, Facility Management, Property Management)

- 4.13 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Industrial

- 5.1.4 Logistics

- 5.1.5 Multi-family

- 5.1.6 Hospitality

- 5.2 By Key Cities

- 5.2.1 Bangkok

- 5.2.2 Chiang Mai

- 5.2.3 Hua Hin

- 5.2.4 Koh Samui

- 5.2.5 Rest of Thailand

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Developers

- 6.2.1.1 Central Pattana PLC

- 6.2.1.2 Supalai Company Limited

- 6.2.1.3 Pace Development Corporation PLC

- 6.2.1.4 Raimon Land PCL

- 6.2.1.5 Blink Design Group*

- 6.2.2 Real Estate Agencies

- 6.2.2.1 CBRE Thailand

- 6.2.2.2 Savills

- 6.2.2.3 Colliers International Thailand

- 6.2.2.4 RE/MAX Thailand

- 6.2.2.5 JLL Thailand

- 6.2.2.6 Knight Frank Thailand*

- 6.2.3 Other Companies (Start-ups, Associations)

- 6.2.3.1 Property Perfect

- 6.2.3.2 Hipflat

- 6.2.3.3 DDProperty

- 6.2.3.4 Dot Property*

- 6.2.1 Developers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX