PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445832

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445832

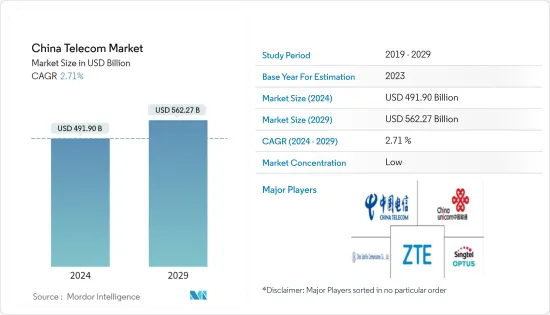

China Telecom - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The China Telecom Market size is estimated at USD 491.90 billion in 2024, and is expected to reach USD 562.27 billion by 2029, growing at a CAGR of 2.71% during the forecast period (2024-2029).

Over the past three decades, China's telecommunications sector has undergone several waves of liberalization and privatization-related reforms. One of the world's biggest marketplaces for communications today is China. The Chinese telecoms sector has undergone several changes and impressive developments in recent years.

Key Highlights

- According to official figures, China's telecoms industry had sustained growth in the first seven months of this year. 944.2 billion yuan (USD 137.87 billion) was the total industrial income, up 8.3% year over year, according to the Ministry of Industry and Information Technology. During this time, emerging industries like big data, cloud computing, internet data centres, and the Internet of Things saw fast growth. According to China's Ministry of Industry and Information Technology (MIIT), the country's three telecom players, China Telecom, China Mobile, and China Unicom saw a 35.1 per cent increase in emerging business income yearly to 184.3 billion yuan (USD 25.71 billion).

- New players now have chances to improve the telecom ecosystem on the back of 5G deployment. Whether or not they are successful, the most recent 5G launch demonstrates how the number of participants is growing. According to GSMA Intelligence, 198 operators have introduced 5G services, including FWA, in 77 markets as of Q1 of the previous year. 5G connections made up 8% of all mobile connections worldwide. 85% of the USD 620 billion worldwide mobile CAPEX that operators are predicted to spend on 5G between last year and 2025. With 68% of all 5G connections worldwide as of Q1 of the previous year, China is a significant 5G market. Chinese operators intend to collectively install 2 million 5G base stations by the end of last year.

- The digital transformation in China is opening opportunities not just for people inside its borders but also for enterprises worldwide. For enterprises worldwide, it will be crucial to comprehend this enormous shift in the Chinese market's use of technology and how to capitalize on it. Since customers spend more money online at established e-commerce sites, this expansion has been centered on them. According to an All-China Review, China's gross domestic product (GDP) growth between 2013 and 2025 may be attributed to 7 and 22% of the country's upcoming digital revolution.

- However, the United States authorities have recently targeted Chinese telecom and technology companies due to national security concerns. In November 2021, President Joe Biden signed legislation prohibiting organizations deemed a security danger from obtaining new telecom equipment licenses. The Secure Equipment Act mandates that the Federal Communications Commission (FCC) cease to review applications from risk-prone organizations. This prohibits the use of equipment from Huawei, ZTE, and three other Chinese businesses in the US telecommunications network. Also, during the same time, the United States government added a dozen Chinese firms to its list of entities with whom it has prohibited trade, citing national security and foreign policy concerns.

- The COVID-19 pandemic made people aware of how strong the telecommunication network is to Chinese finance, business, and the economy. According to GSMA research, mobile networks have played a crucial role in sustaining social and economic activity during the epidemic by supplying connections. During the pandemic, the volume of mobile data traffic in China increased by 40% compared to the previous month. However, despite this increase, the analysis concluded that networks were mainly robust, underscoring operators' major recent expenditures in cutting-edge networks.

China Telecom Market Trends

Stellar performance of 5G would trigger wireless segment growth

- The previous year was crucial for 5G's first success and further development. Globally, 5G is steadily expanding to become the fastest-commercializing mobile technology. China is now the country with the most 5G connections and base stations globally. Due to the implementation of 5G, new players can now enhance the telecom ecosystem. The most recent 5G launch shows how the number of participants is increasing, whether they are successful or not.

- On October 31, 2019, China Telecom, China Unicom, and China Mobile began 5G services. As per an Electronics Media report, compared to the United States, which has 5G in 296 cities, China has 356 more towns covered by 5G services than it has. By the end of last year, China had two million 5G base stations. China Broadnet's 5G service has gained state-wide coverage only a few months after its initial introduction. In September last year, the fourth-largest operator in the nation formally debuted commercial 5G network services in the Qinghai Province in northwest China and the Xizang Autonomous Region in southwest China, expanding its 5G coverage to all 31 provinces.

- Compared to its competitors, China Mobile earned 160MHz in the 2.6GHz band and 100MHz in the 4.9GHz round, while competitor carriers China Telecom and China Unicom each received 100MHz in the 3.5GHz game. Early last year, China Broadnet announced a special discount promotion that will save consumers 40% when purchasing 5G bundles, bringing the operator's 5G coverage roll-out ahead of the anticipated November launch date.

- In a post-pandemic future, digital connections and services are crucial for allowing both innovative business models and better consumer experiences. Authorities in China have moved to develop enabling regulations for constructing cost-effective infrastructure because they recognize the possibilities digital technology can offer society. In January last year, the MIIT report disclosed that operators in mainland China had deployed more than 1.4 million 5G base stations. Since then, the MIIT has set an ambitious goal to treble the number of 5G base stations to 3.64 million by the end of 2025.

Demand for new digital services

- To further the development of digital China, new and innovative technological advancements in fields like software, semiconductors, and operating systems are required. Cloud-network integration has become the key component of digital information infrastructure. To progress the Digital China program, the fifth Digital China Summit, hosted online and offline over two days, focused on new innovations-driven developments and digitalization-led landscapes. It also had a display of the most recent technological developments and items. As the country's largest telecom provider to create a reliable digital telecom infrastructure for a digital China, China Telecom will intensify efforts to promote the convergence of cloud computing and telecom network technologies.

- According to the Ericsson IoT Accelerator report, with the "One Belt, One Road" policy in mind, China Telecom has developed the connection management platform CTWING to accelerate the deployment of IoT products and services deployment. Through collaborations, China Telecom helps businesses to implement, regulate, and grow IoT device management. The managed connection service provided by China Telecom is integrated with the business operations of enterprise clients using this solution to produce highly dependable IoT solutions.

- Ericsson has worked as a dependable, established technology partner with China Telecom for many years. Due to its extensive experience in the worldwide IoT market, Ericsson was chosen as the service provider's partner in IIoT. Its IoT Accelerator platform offers business clients dependable connections based on service-level agreements and a unified perspective of devices and access networks, supporting China Telecom's international IoT aspirations.

- The cloud has evolved into a key growth engine for Chinese telecoms, marking it another point of distinction from other markets. The three telcos reported combined cloud revenues of 70 billion Chinese yuan (USD 10.1 billion) in their interim results from August 2022. China Telecom saw a growth of 101% to 28 billion yuan (USD 3.9 billion), China Mobile saw an increase of 104% to 23 billion yuan (USD 3.2 billion), and China Unicom saw a growth of 143% to 19 billion yuan (USD 2.6 billion).

- According to government research organization CAICT, the public cloud accounted for three-fifths of the 301-billion-yuan (USD 42 billion) industry in the previous year, with the Chinese cloud market growing by 48%. As per an IDC report, the government cloud industry is one of the markets with the most significant growth potential, which is expected to develop gradually over the next three to five years and reach USD 6 billion in revenue in the previous year, an increase of 21%.

- As per a study by China Internet Network Information Center (CNNIC), China had more than one billion Internet users as of June last year; the enormous scale has accelerated the creation of new digital infrastructure, facilitated domestic circulation, and enhanced digital government services. These factors have all contributed to the high-quality development of China's economy. The flexible work paradigm exemplified by the online office will continue to be developed in China as digital business transformation continues. Online document collaborative editing and online video/teleconferencing usage were both 23.8% as of June last year, up 1.0 and 2.6 percentage points, respectively, from December 2020. As reported by CNNIN, online document collaborative editing and online video/teleconferencing usage were both 23.8% as of June last year, up 1.0 and 2.6 percentage points, respectively, from December 2020.

China Telecom Industry Overview

The Chinese Telecom market is highly fragmented in nature. Some major players in the market studied include China Telecom Corp, China United Network Communications Group Co., Ltd., China Satellite Communications Co., Ltd, ZTE Corporation, and Singtel Optus Pty. The market also hosts other Internet service providers (ISPs), MVNOs, and fixed-line service providers. Some US telecommunication companies are competitive internationally and hold firm ground in the global telecom space.

- In January 2022, China Mobile tested a three-part Carrier Aggregation (CA) system in collaboration with Nokia and MediaTek in Shanghai. A total of 190MHz bandwidth was successfully combined in the testing by combining a 30MHz FDD block in the 700MHz frequency with 100MHz and 60MHz TDD blocks in the 2.6GHz spectrum.

- In July 2022, China Unicom Video Technology, in partnership with Huawei, launched the Huawei Go3D solution. This technology can produce 3D video streams automatically for live TV and video-on-demand (VOD) services. Also, this technology boosts operators' video services by lowering the cost of producing 3D content and offering a completely fresh user experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness-Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 COVID-19 Impact on the Industry Ecosystem

- 4.5 Regulatory Landscape in the Country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Continuous roll out of 5G

- 5.1.2 Growth of high-quality defensive companies

- 5.1.3 Demand for new digital services

- 5.2 Market Restrain

- 5.2.1 Intensified restrictions of the United States

- 5.2.2 Security Threat from Chinese Telecom

- 5.3 Analysis of the Market based on Connectivity (Coverage to include In-depth Trend Analysis)

- 5.3.1 Fixed Network

- 5.3.1.1 Broadband (Cable modem, wireline-fiber, wireline DSL, fixed Wi-Fi ), Trends regarding ADSL/VDSL, FTTP/B, cable modem, FWA, and 5G FWA )

- 5.3.1.2 Narrowband

- 5.3.2 Mobile Network

- 5.3.2.1 Smartphone and mobile penetration

- 5.3.2.2 Mobile Broadband

- 5.3.2.3 2G, 3G, 4G and 5G connections

- 5.3.2.4 Smart Home IoT and M2M connections

- 5.3.1 Fixed Network

- 5.4 Analysis of Telecom Towers (Coverage to include in-depth trend analysis of various types of towers, like, lattice, guyed, monopole, and stealth towers)

6 MARKET SEGMENTATION

- 6.1 Segmentation by Services (Coverage to include Average Revenue Per User for the overall Services segment, Market size and Estimates for each segment for the period of 2020-2027 and in-depth Trend Analysis)

- 6.1.1 Voice Services

- 6.1.1.1 Wired

- 6.1.1.2 Wireless

- 6.1.2 Data and Messaging Services (Coverage to include Internet & Handset Data packages, Package Discounts)

- 6.1.3 OTT and PayTV Services

- 6.1.1 Voice Services

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 China Telecom Corp.

- 7.1.2 China United Network Communications Group Co., Ltd.

- 7.1.3 China Satellite Communications Co., Ltd.

- 7.1.4 ZTE Corporation.

- 7.1.5 Singtel Optus Pty

- 7.1.6 Wingtech Technology Co.Ltd

- 7.1.7 Jiangsu Zhongtian Technology Co., Ltd.

- 7.1.8 China Railway Signal & Communication Co.,Ltd.

- 7.1.9 FiberHome Telecommunication Technologies Co Ltd

- 7.1.10 Tencent Holdings Ltd.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS