PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445856

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445856

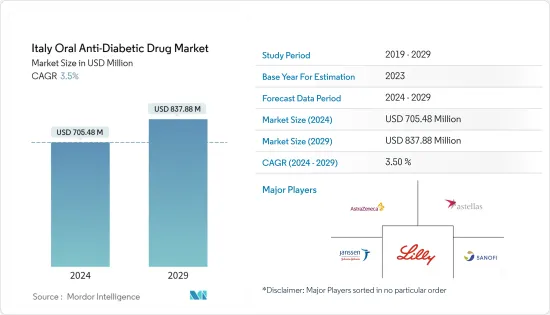

Italy Oral Anti-Diabetic Drug - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Italy Oral Anti-Diabetic Drug Market size is estimated at USD 705.48 million in 2024, and is expected to reach USD 837.88 million by 2029, growing at a CAGR of 3.5% during the forecast period (2024-2029).

The COVID-19 pandemic caused early fatalities during the first year of its existence, primarily in older people. The first nation in Europe to experience COVID-19 was Italy. One of the nations with the greatest excess mortality rates is Italy. The majority of COVID-19 fatalities were caused by the co-existence of two or more chronic diseases in the same person. Several studies have established the link between long-term conditions, including diabetes, and unfavorable results in COVID-19 patients. Diabetic patients were more likely than healthy individuals to experience significant consequences. The makers of diabetic pharmaceuticals took precautions during COVID-19 to ensure that the meds were delivered to diabetes patients with the aid of local governments. According to a statement made by Novo Nordisk on their website, "Since the start of COVID-19, our commitment to patients, our employees, and the communities where we operate has remained unchanged. We continue to supply our medications and devices to people with diabetes and other serious chronic diseases, protect the health of our employees, and take actions to support doctors and nurses as they work to defeat COVID-19."

Pharmaceuticals known as diabetic medications were created to stabilize and regulate blood glucose levels in diabetics. Diabetes patients infected with SARS-CoV-2 during the COVID-19 pandemic were treated with diabetic medications. According to IDF, 9.9% of Italians will have diabetes by 2021. Obesity, a poor diet, and lack of exercise are the main causes of the rise in newly diagnosed Type 1 and Type 2 diabetes cases. Diabetes care items are being used more frequently, as evidenced by the fast-rising incidence, prevalence, and healthcare costs of diabetic individuals.

Italy Oral Anti-Diabetic Drug Market Trends

Sodium-glucose Cotransport-2 (SGLT-2) inhibitor Segment Occupied the Highest Market Share in the Italy Oral Anti-Diabetic Drugs Market in 2022

In terms of revenue, the Sodium-glucose Cotransport-2 (SGLT-2) inhibitor Segment is anticipated to lead the Italy Oral Anti-Diabetic Drugs Market and post a CAGR of over 11% during the course of the forecast year.

A class of pharmaceuticals known as the Sodium-glucose Cotransport-2 (SGLT-2) inhibitor Segment is used to treat type 2 diabetes, and several of these medications have also been licensed to treat obesity. The fact that this family of medications has a reduced risk of producing hypoglycemia than older insulin secretagogues like sulfonylureas or meglitinides is one of their advantages. In addition to playing a substantial role in decreasing blood sugar, SGLT2 also has strong anti-inflammatory, lung-protective, and impacts on the composition of gut microorganisms. Consequently, SGLT2 drugs have proved excellent antidiabetic (glucose-lowering) medications during the COVID-19 pandemic times as well as viable candidates for treating people impacted by COVID-19 infection, with or even without type 2 diabetes. Italian legislation establishes a framework with medical organizations, prevention initiatives, staff education, and legal protection to control the clinical care of diabetic patients. The National Health Program is set up into fundamental tiers of aid, each of which can be defined uniquely in each location. LEAs are how the National Health Program is organized. All medical aid programs provided by the INHS to citizens, with or without a patient's income-based partial contribution, are defined by LEAs. One of the major problems facing the Italian healthcare system is diabetes, a serious health issue. The development of novel medications to give diabetic patients more treatment options has been driven by the disease's increasing incidence, prevalence, and progressive nature. Some of the potential prospects for the companies in the Italian diabetes medications market include the introduction of several new products, expanding international research collaborations for technological advancement, and raising public awareness of diabetes.

Increasing Diabetes Population in Italy is driving the market.

Italy witnessed an alarming increase in the prevalence of diabetes in recent years. Patients with diabetes require many corrections throughout the day to maintain nominal blood glucose levels, such as oral anti-diabetic medication or ingestion of additional carbohydrates by monitoring their blood glucose levels. The rate of newly diagnosed Type 1 and Type 2 diabetes cases is seen to increase, mainly due to obesity, unhealthy diet, and physical inactivity. The rapidly increasing incidence and prevalence of diabetic patients and healthcare expenditure are indications of the increasing usage of diabetic drugs.

Oral anti-diabetic medications have been made available globally and are advised for usage when type 2 diabetes therapy needs to be escalated along with lifestyle modification. Due to the wide range of efficacy, safety, and modes of action that oral medicines have, they are frequently the first treatments employed in the treatment of type 2 diabetes. Diabetes patients can minimize their risk of complications and maintain control of their illness with the use of anti-diabetic medications. Throughout the rest of their lives, people with diabetes may need to take anti-diabetic medications to manage their blood sugar levels and prevent hypo and hyperglycemia. Oral anti-diabetic medications have higher acceptance than insulin, which improves adherence to therapy. They also have the advantages of easier control and lower costs. The Italian National Healthcare Service (NHS) ensures universal coverage for all citizens. People living with diabetes have access, with no out-of-pocket expenditure, to all the medicines, devices, and medical services they need. Overall, Italy has a well-developed system of diabetes care, with numerous diabetes centers throughout the country and treatment free at the point of delivery. The Italian health system is highly decentralized, with most administrative and organizational powers held by the Regions. The National Diabetes Plan defines priorities and provides guidelines to improve the quality of diabetes care with a patient-centered focus.

It is therefore anticipated to drive the category expansion during the forecast period because of the aforementioned factors.

Italy Oral Anti-Diabetic Drug Industry Overview

The Italy oral anti-diabetes drug market is consolidated, with a few major manufacturers like Eli Lilly, AstraZeneca, Sanofi, and Janssen Pharmaceuticals having a global market presence. In contrast, the remaining manufacturers are confined to the other local or regional markets. Companies are focusing on innovations in diabetes drugs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Oral Anti-diabetic drugs (Value and Volume, 2017 - 2028)

- 5.1.1 Biguanides

- 5.1.1.1 Metformin

- 5.1.2 Alpha-Glucosidase Inhibitors

- 5.1.2.1 Alpha-Glucosidase Inhibitors

- 5.1.3 Dopamine D2 receptor agonist

- 5.1.3.1 Bromocriptin

- 5.1.4 SGLT-2 inhibitors

- 5.1.4.1 Invokana (Canagliflozin)

- 5.1.4.2 Jardiance (Empagliflozin)

- 5.1.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.1.4.4 Suglat (Ipragliflozin)

- 5.1.5 DPP-4 inhibitors

- 5.1.5.1 Onglyza (Saxagliptin)

- 5.1.5.2 Tradjenta (Linagliptin)

- 5.1.5.3 Vipidia/Nesina(Alogliptin)

- 5.1.5.4 Galvus (Vildagliptin)

- 5.1.6 Sulfonylureas

- 5.1.6.1 Sulfonylureas

- 5.1.7 Meglitinides

- 5.1.7.1 Meglitinides

- 5.1.1 Biguanides

6 MARKET INDICATORS

- 6.1 Type-1 Diabetic Population (2017 - 2028)

- 6.2 Type-2 Diabetic Population (2017 - 2028)

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Takeda

- 7.1.2 Novo Nordisk

- 7.1.3 Pfizer

- 7.1.4 Eli Lilly

- 7.1.5 Janssen Pharmaceuticals

- 7.1.6 Astellas

- 7.1.7 Boehringer Ingelheim

- 7.1.8 Merck And Co.

- 7.1.9 AstraZeneca

- 7.1.10 Bristol Myers Squibb

- 7.1.11 Novartis

- 7.1.12 Sanofi

8 MARKET OPPORTUNITIES AND FUTURE TRENDS