PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445859

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445859

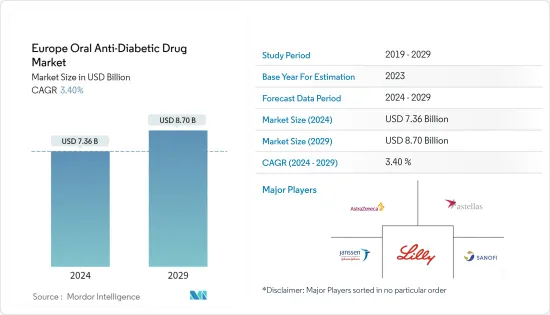

Europe Oral Anti-Diabetic Drug - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Europe Oral Anti-Diabetic Drug Market size is estimated at USD 7.36 billion in 2024, and is expected to reach USD 8.70 billion by 2029, growing at a CAGR of 3.40% during the forecast period (2024-2029).

The COVID-19 epidemic significantly influenced the European Diabetes Medicines Market. As people with diabetes already have weakened immune systems, COVID-19 causes those immune systems to deteriorate rapidly. Compared to healthy persons, those with diabetes are more likely to experience significant complications. During COVID-19, the makers of diabetes pharmaceuticals took special care to ensure that diabetic patients received their meds with the assistance of local governments. On their website, NovoNordisk stated that they "continue to provide our medicines and devices to people living with diabetes and other serious chronic diseases, safeguard the health of our employees, and take actions to support doctors and nurses.

Pharmaceuticals known as diabetic medications were created to stabilize and regulate blood glucose levels in diabetics. Diabetes patients infected with SARS-CoV-2 during the COVID-19 pandemic may be treated with diabetic medications. The estimated cost per hospital admission for type 2 diabetes patients with good glycemic control during the first wave of COVID-19 in Europe ranged from EUR 25,018 to EUR 57,244 for type 1 diabetes patients with poor glycemic control, reflecting a higher risk of intensive care, ventilator support, and a longer hospital stay. Those without diabetes were expected to pay EUR 16,993. For COVID-19 secondary care, 13.9 billion euros in direct costs were projected to be spent overall in Europe. Hence, diabetes treatment accounted for 23.5% of overall costs.

In recent years, diabetes prevalence has increased alarmingly throughout the European continent. Many health issues are related to diabetes. Diabetes patients need to make several adjustments throughout the day to keep their blood glucose levels within normal ranges. For example, they may need to administer more insulin or consume more carbohydrates.

As a result of the aforementioned variables, it is projected that the market under study will expand during the course of the investigation.

Europe Oral Anti-Diabetic Drug Market Trends

Biguanide Segment Occupied the Highest Market Share in the Europe Oral Anti-Diabetic Drugs Market in 2022

The drug metformin is categorized as a biguanide and is used to treat type 2 diabetes. For its "off-label" use in treating persons with disorders like insulin resistance, it is prescribed. Since metformin therapy was introduced, a large number of patients have been successfully treated with this widely accessible drug with a good risk/benefit profile and is advised by IDF recommendations as a first-line prescription. As a result, metformin continues to be the most widely prescribed oral antidiabetic drug in the world, being prescribed in 45-50% of all prescriptions and being taken by more than 150 million people annually. The large market share is a result of long-term favorable experience with metformin use, strong evidence of clinical efficacy, safety, high adherence rate, low cost, widespread availability, and cost-effectiveness.

In recent years, diabetes prevalence has increased alarmingly throughout the European continent. People with diabetes need to make several adjustments during the day to keep their blood glucose levels within acceptable ranges. Examples include taking oral anti-diabetic medicine or consuming more carbs while keeping an eye on their blood glucose levels. Obesity, a poor diet, and lack of exercise are the main causes of the rise in newly diagnosed Type 1 and Type 2 diabetes cases. Diabetes medicine usage is on the rise, as evidenced by the fast-rising incidence, prevalence, and healthcare costs of diabetes individuals. Oral anti-diabetic medications have been made available globally and are advised for usage when type 2 diabetes therapy needs to be escalated along with lifestyle modification. Due to the wide range of efficacy, safety, and modes of action that oral medicines have, they are frequently the first treatments employed in the treatment of type 2 diabetes. Diabetes patients can minimize their risk of complications and maintain control of their illness with the use of anti-diabetic medications. Throughout the rest of their lives, people with diabetes may need to take anti-diabetic medications to manage their blood sugar levels and prevent hypo and hyperglycemia. Oral anti-diabetic medications have higher acceptance than insulin, which improves adherence to therapy. They also have the advantages of easier control and lower cost.

In the Europe Oral Anti-Diabetes Medications Market, Germany holds more than 15% of the market share.

Throughout the projected period, Germany is anticipated to dominate the market and post a CAGR of over 3%.

One of the astonishing issues facing Germany's healthcare institutions is diabetes, a serious health issue. The adult population of Germany has a very high prevalence of type 1 and type 2 diabetes, as well as a sizable number of individuals who have not yet received a diagnosis. Throughout the coming years, it is anticipated that the prevalence of type 2 diabetes will rise significantly as a result of an aging population and an unhealthy lifestyle. The most important elements in preventing complications in German type 2 diabetes patients are high-quality care, which includes proper monitoring, control of risk factors, and active self-management.

The development of novel medications to give diabetic patients more treatment options has been driven by the disease's increasing incidence, prevalence, and progressive nature. More than half of sales in the anti-diabetic market are currently made by non-insulin medications, which are utilized as first-line therapies for type 2 diabetes patients. Sodium-glucose cotransporter-2 inhibitors and dipeptidyl peptidase-4 inhibitors (DPP-4) are two significant groups that have just entered this market. In order to lower blood sugar levels in persons with type 2 diabetes, oral antidiabetic medications function in a variety of methods. Some increase pancreatic insulin secretion, while others enhance cell insulin sensitivity or stop the liver from producing glucose. Others reduce the rate of glucose absorption following meals.

The German Diabetes Center (DDZ) estimates that at least 7.2% of the population in Germany presently has diabetes, and that number will rise dramatically over the next 20 years. According to German legislation, public insurance plans must cap out-of-pocket medical expenses and provide coverage for all medically essential procedures, including oral Anti-Diabetes Market. One of the developed nations with cutting-edge medical facilities in Germany. The market is further driven by the strict regulation of pricing and reimbursement policies. Some of the potential prospects for the companies in the German diabetes medications market include the introduction of several new products, expanding international research collaborations for technological advancement, and raising public awareness of diabetes.

Europe Oral Anti-Diabetic Drug Industry Overview

The Europe oral anti-diabetes drug market is consolidated, with a few major manufacturers like Eli Lilly, AstraZeneca, Sanofi, and Janssen Pharmaceuticals having a global market presence. In contrast, the remaining manufacturers are confined to the other local or regional markets. Companies are focusing on innovations in diabetes drugs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Oral Anti-diabetic drugs (Value and Volume, 2017 - 2028)

- 5.1.1 Biguanides

- 5.1.1.1 Metformin

- 5.1.2 Alpha-Glucosidase Inhibitors

- 5.1.2.1 Alpha-Glucosidase Inhibitors

- 5.1.3 Dopamine D2 receptor agonist

- 5.1.3.1 Bromocriptin

- 5.1.4 SGLT-2 inhibitors

- 5.1.4.1 Invokana (Canagliflozin)

- 5.1.4.2 Jardiance (Empagliflozin)

- 5.1.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.1.4.4 Suglat (Ipragliflozin)

- 5.1.5 DPP-4 inhibitors

- 5.1.5.1 Onglyza (Saxagliptin)

- 5.1.5.2 Tradjenta (Linagliptin)

- 5.1.5.3 Vipidia/Nesina(Alogliptin)

- 5.1.5.4 Galvus (Vildagliptin)

- 5.1.6 Sulfonylureas

- 5.1.6.1 Sulfonylureas

- 5.1.7 Meglitinides

- 5.1.7.1 Meglitinides

- 5.1.1 Biguanides

- 5.2 Geography

- 5.2.1 France (Value and Volume 2017-2028)

- 5.2.1.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.2 Germany (Value and Volume 2017-2028)

- 5.2.2.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.3 Italy (Value and Volume 2017-2028)

- 5.2.3.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.4 Russia (Value and Volume 2017-2028)

- 5.2.4.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.5 Spain (Value and Volume 2017-2028)

- 5.2.5.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.6 United Kingdom (Value and Volume 2017-2028)

- 5.2.6.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.7 Rest of Europe (Value and Volume 2017-2028)

- 5.2.7.1 By Drug (Biguanides, Alpha-glucosidase Inhibitors, Dopamine-D2 Receptor Agonists, SGLT-2 Inhibitors, DPP-4 Inhibitors, Sulfonylureas, Meglitinides)

- 5.2.1 France (Value and Volume 2017-2028)

6 MARKET INDICATORS

- 6.1 Type-1 Diabetic Population (2017 - 2028)

- 6.2 Type-2 Diabetic Population (2017 - 2028)

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Takeda

- 7.1.2 Novo Nordisk

- 7.1.3 Pfizer

- 7.1.4 Eli Lilly

- 7.1.5 Janssen Pharmaceuticals

- 7.1.6 Astellas

- 7.1.7 Boehringer Ingelheim

- 7.1.8 Merck And Co.

- 7.1.9 AstraZeneca

- 7.1.10 Bristol Myers Squibb

- 7.1.11 Novartis

- 7.1.12 Sanofi

8 MARKET OPPORTUNITIES AND FUTURE TRENDS