PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445968

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445968

Emergency And Disaster Response - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

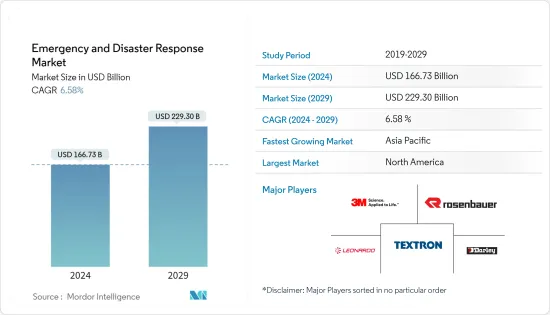

The Emergency And Disaster Response Market size is estimated at USD 166.73 billion in 2024, and is expected to reach USD 229.30 billion by 2029, growing at a CAGR of 6.58% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic had a significant impact on the emergence and disaster response market. With the unprecedented surge in cases, the demand for medical equipment, personal protective gear, and emergency supplies skyrocketed, putting immense pressure on the industry's capacity. Additionally, the pandemic highlighted the need for enhanced digital solutions and data analytics to improve response coordination and resource allocation in times of crisis, leading to a shift towards more technology-driven approaches in the market.

- In an ever-changing world, marked by the constant threat of natural calamities, technological mishaps, and unforeseen pandemics, the ability to respond swiftly and effectively to emergencies and disasters has become a paramount concern for governments, organizations, and individuals alike. The focus on preparedness and resilience has intensified, driving investment in research and development of innovative solutions to tackle future emergenies effectively. Increasing incidents of natural and anthropogenic hazards globally have led to a rise in the procurement of necessary equipment and response vehicles by the concerned government agencies. As emergencies become more complex and diverse, traditional approaches might prove insufficient, neccessitating continous adaptiona and innovation. This uncertainity can make it difficult for stakeholders to anticipate and prepare for all potential scenerios, adding further strain on the market's ability to respond effectively.

Emergency and Disaster Response Market Trends

Land Segment to Register the Highest CAGR during the Forecast Period

- The land segment recorded the highest CAGR in the market in the forecast period. Increasing procurement of land vehicles by various public and private organizations is acting as the main driver for the market. Land vehicles can be locally stationed and can be easily and promptly deployed for emergency damage alleviation purposes. To increase the availability of land-based emergency response vehicles, local disaster management and emergency response teams keep these vehicles at their disposal.

- Thus, their procurement volumes are higher compared to the aerial vehicles, whose overall fleet is less, as they are stationed only in bigger cities that possess the necessary infrastructure to maintain the aircraft. However, with the growing number of large-scale disasters, the deployment of aerial vehicles for purposes like firefighting and disaster relief logistics is increasing.

- For instance, in May 2022, American Medical Response was awarded a new USD 1.2 billion five-year contract to provide medical transport and support in response to national disasters and emergencies. AMR is the biggest provider of ground medical transportation in the US and FEMA's prime EMS provider.

North America to Dominate Market Share During the Forecast Period

- North America dominates the market share due to high spending from the government, in addition to the continual procurement of related equipment and vehicles by various public and private disaster rescue teams. Severe hurricanes and floods have hit the US in the recent past, and the country, along with Canada, has seen several forest fires in the past five years. In response to all these occurrences, the procurement of disaster response equipment and vehicles has increased in the region. These factors are expected to drive the market in the region during the forecast period.

- For instance, in January, ICF was awarded a new USD 51 million contract by the Puerto Rico Department of Housing (PRDOH) to support the commonwealth's single-family disaster recovery and mitigation programs. The contract is for three years with an option to extend for another 24 months. ICF will expand its implementation support of PRDOH's Community Development Block Grant for Disaster Recovery (CDBG-DR) and Community Development Block Grant for Mitigation (CDBG-MIT) grant programs to repair and rebuild homes damaged by hurricanes Irma and Maria, as well as build resilience against future natural disasters, under the terms of the contract.

- However, the Asia-Pacific region, which is one of the largest disaster-prone zones in the world, is projected to experience the highest growth rates in the market. The presence of some of the largest populated countries in the world, where a delay in emergency and disaster response can increase fatality rates drastically, is compelling the governments in the region to stay prepared for disasters and other emergencies by procuring the necessary equipment. For instance, the Provincial Government of Batangas (Philippines) has announced their purchase of 186 brand new Hino 200 Series Rescue trucks to enhance emergency response capabilities. Likewise, Williamson County is looking to revolutionize its flood disaster preparation, response and recovery with a new contract with FloodMapp. FloodMapp is an Australian technology company that provides real-time flood mapping for emergency managers to reduce the impacts on their communities.

Emergency and Disaster Response Industry Overview

The market is fragmented, with various players in the market supplying their products to various applications that fall under the overall emergency and disaster response market. Rosenbauer International AG, Darley, Textron Inc., 3M, and Leonardo S.p.A. are some of the major players in the market. In addition, the presence of many local players in each country with varying product portfolios is enhancing market fragmentation.

Thus, the competition for the players is restricted to the product portfolios they offer, and there are no cross-industry competitors for the players. In such cases, players compete with a relatively lower direct-competitor pool than facing a larger set of multi-industry players having different product offerings. Established players in the market gain the flexibility to expand their product reach by entering other related industries either by partnerships or acquisitions.

For instance, Rosenbauer is very successful in Germany with its ET series these days. Currently, the group firefighting vehicles for disaster relief (LF 20 KatS) are being delivered, which the Federal Ministry of the Interior ordered at the end of 2021, on behalf of the Federal Office of Civil Protection and Disaster Assistance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment

- 5.1.1 Threat Detection Equipment

- 5.1.2 Personal Protection Gear

- 5.1.3 Medical Equipment

- 5.1.4 Temporary Shelter Equipment

- 5.1.5 Mountaineering Equipment

- 5.1.6 Fire Fighting Equipment

- 5.1.7 Other Equipment

- 5.2 Vehicle Platform

- 5.2.1 Land

- 5.2.2 Marine

- 5.2.3 Airborne

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rosenbauer International AG

- 6.2.2 Darley

- 6.2.3 Ziegler GmbH

- 6.2.4 Magirus GmbH

- 6.2.5 Emergency One Group

- 6.2.6 Viking Air Ltd.

- 6.2.7 Textron Inc.

- 6.2.8 Leonardo S.p.A

- 6.2.9 3M

- 6.2.10 Emergency Medical International

- 6.2.11 Smiths Group plc

- 6.2.12 REV Group, Inc.

- 6.2.13 Honeywell International, Inc.

- 6.2.14 Juvare, LLC

- 6.2.15 Esri, Inc.

- 6.2.16 Everbridge, Inc.

- 6.2.17 Hexagon AB

7 MARKET OPPORTUNITIES AND FUTURE TRENDS