PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939666

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939666

Wood-based Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

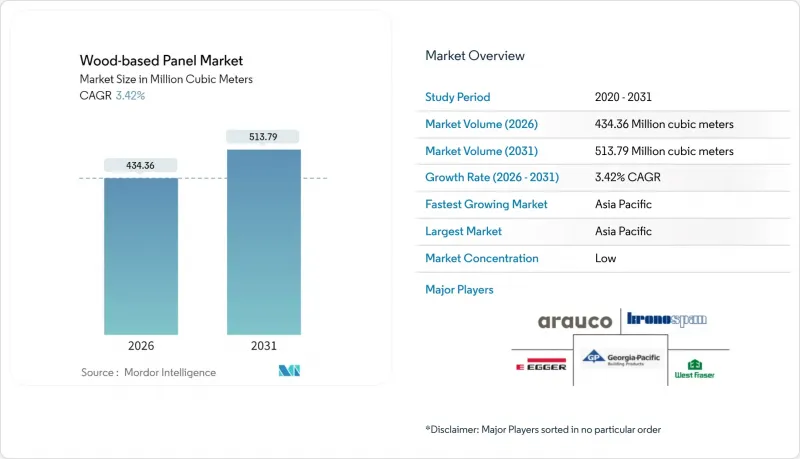

The Wood-based Panel Market size in 2026 is estimated at 434.36 million cubic meters, growing from 2025 value of 419.99 million cubic meters with 2031 projections showing 513.79 million cubic meters, growing at 3.42% CAGR over 2026-2031.

Robust residential construction, e-commerce-driven furniture demand, and circular-economy regulations anchor this growth even as manufacturers contend with tightening emission norms and volatile fiber costs. Abundant timber resources in Asia-Pacific, capacity expansions across Eastern Europe and the U.S. South, and the rapid uptake of structural insulated panels (SIPs) in modular housing provide additional tailwinds. Competitive strategies now center on vertical integration, resin innovation, and investments in recycling lines that recover fiber from end-of-life boards. These moves aim to capture value as transparent-wood glazing, photoluminescent facades, and other high-performance applications expand the total addressable market.

Global Wood-based Panel Market Trends and Insights

Construction Up-cycle in Emerging Economies

Governments across Asia-Pacific and parts of Latin America are doubling infrastructure outlays, triggering sustained demand for plywood, MDF, and oriented strand board. India's federal highway program and Indonesia's new capital project underpin multi-year procurement cycles, while Turkey's earthquake reconstruction tripled imports of Russian sawn timber to 292,200 m3 in early 2024. Manufacturers are stockpiling logs despite near-term demand softness to hedge against future supply squeezes, as evidenced by India's 40% import surge over two quarters. Japanese conglomerates such as Sumitomo Forestry are committing to building 7,000 Southeast-Asian homes within five years, signaling confidence in regional housing pipelines. These developments cement an upward consumption trajectory across structural panels through at least 2028.

Furniture E-commerce Boom

Rising online furniture sales reduce geographic barriers, prompting quicker model turnover and small-lot production that favors flexible panel suppliers. U.S. residential furniture orders rose 22% year-on-year in April 2024, even as domestic wood-furniture shipments are 48% below 2000 levels. Import-oriented value chains still depend heavily on particleboard, MDF, and plywood substrates, sustaining bulk panel volumes. Malaysia leveraged e-commerce logistics to lift wood exports to RM 22.7 billion in 2021, with plywood the top item. Agile mills capable of just-in-time lamination and digital-print decor delivery continue capturing share within this fast-moving channel.

Formaldehyde-Emission Regulations Tightening

The EU will cap indoor-air formaldehyde at 0.062 mg/m3 from August 2026, compelling mills to switch to no-added-formaldehyde resins that cost 15-25% more. Germany's harmonization with the EU rule eliminates domestic carve-outs, while U.S. EPA limits remain at similar thresholds, leaving little room for avoidance. Capital upgrades to continuous-press lines and alternative adhesive systems squeeze cash flows, especially at smaller particleboard facilities that already operate on slim spreads.

Other drivers and restraints analyzed in the detailed report include:

- Circular-Economy Mandates Favoring Engineered Wood

- Rapid Uptake of OSB-based SIPs in Modular Housing

- EU Deforestation Regulation Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Global MDF/HDF shipments are projected to expand at a 4.12% CAGR, outpacing overall wood-based panel market growth. China continues to supply roughly 60% of the world's MDF, yet new mills in Vietnam and Eastern Europe are closing distance through lower-cost fiber, automated sanding lines, and digital-print decors. Mekong Wood's 600,000 m3 press in Cam Khe entered service in July 2024, immediately targeting Japanese importers seeking CARB-compliant board. In mature economies, sustainability labeling steers demand toward MDF blended with up to 24% recycled fiber without compromising bending strength.

Plywood retains a commanding 27.85% share thanks to universality in sheathing and cabinet carcasses. Yet OSB volumes are rising faster on the back of SIPs and code-compliant shear panels, while particleboard holds relevance in value-priced furniture. Hardwood plywood captures premium kitchen and RV interiors, leveraging exotic veneers despite supply tightness linked to the EUDR. Producers are diversifying feedstocks, using plantation teak offcuts in India and rubberwood in Malaysia to cut log costs and improve lifecycle scores.

The Wood-Based Panel Report is Segmented by Product Type (Medium Density Fiberboard (MDF)/High-Density Fiberboard (HDF), Oriented Strand Board (OSB), Particleboard, Plywood, Hardwood, and Other Types), Application (Furniture, Construction, Packaging, and Other), and Geography (Asia Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Million Cubic Meters).

Geography Analysis

Asia-Pacific generated 52.12% of 2025 shipments and is set to expand at a 3.85% CAGR through 2031. China's plywood exports reached 13.27 million m3 valued at USD 5.27 billion in 2024, bolstered by tariff concessions into ASEAN and the Middle East. Europe's panel makers confront mixed conditions. Mills must retrofit formaldehyde-free resins and implement EUDR tracing, elevating cost curves. Yet post-pandemic renovation booms in Germany and France, plus biomass subsidies for panel offcuts, cushion demand. Eastern European plants, such as Kronospan's 700,000 m3 OSB line in Rivne, enjoy proximity to conifer stands and EU end-users, positioning them to backfill supply gaps.

North America exhibits bifurcated trends. Structural panel output fell 4.6% for OSB and 1.0% for plywood in 2023. Mills in the U.S. South leverage low stumpage and upgraded continuous presses to export surplus OSB to Europe. British Columbia capacity rationalization continues due to stumpage hikes and wildfire disruptions. Latin America, led by Brazil, is the emergent supply base; abundant Pinus plantations and currency advantages permit price-competitive exports, while domestic consumption grows alongside prefabricated social housing schemes.

- Arauco

- Boise Cascade

- CenturyPly

- Dexco

- Dongwha Group

- Egger

- Georgia-Pacific

- Greenpanel Industries Limited

- Kastamonu Entegre

- Kronoplus Limited

- Langboard Inc.

- Louisiana-Pacific Corporation

- Pfleiderer

- Roseburg Forest Products

- Swiss Krono Group

- West Fraser

- Weyerhaeuser Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction Up-Cycle in Emerging Economies

- 4.2.2 Furniture E-Commerce Boom

- 4.2.3 Circular-Economy Mandates Favouring Engineered Wood

- 4.2.4 Transparent-Wood Facades and Automotive Glazing Adoption

- 4.2.5 Rapid Uptake of OSB-Based SIPs in Modular Housing

- 4.3 Market Restraints

- 4.3.1 Formaldehyde-Emission Regulations Tightening

- 4.3.2 Volatile Log and Fibre Costs

- 4.3.3 EU Deforestation Regulation (EUDR) Compliance Burden

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Medium Density Fiberboard (MDF)/High-Density Fiberboard (HDF)

- 5.1.2 Oriented Strand Board (OSB)

- 5.1.3 Particleboard

- 5.1.4 Plywood

- 5.1.5 Hardwood

- 5.1.6 Other Types

- 5.2 By Application

- 5.2.1 Furniture

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.2 Construction

- 5.2.2.1 Floor and Roof

- 5.2.2.2 Wall

- 5.2.2.3 Door

- 5.2.2.4 Other Construction (Decor, Frames, Accessories)

- 5.2.3 Packaging

- 5.2.4 Other (Artistry, Industrial Prototyping, Toys)

- 5.2.1 Furniture

- 5.3 By Geography

- 5.3.1 Asia Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arauco

- 6.4.2 Boise Cascade

- 6.4.3 CenturyPly

- 6.4.4 Dexco

- 6.4.5 Dongwha Group

- 6.4.6 Egger

- 6.4.7 Georgia-Pacific

- 6.4.8 Greenpanel Industries Limited

- 6.4.9 Kastamonu Entegre

- 6.4.10 Kronoplus Limited

- 6.4.11 Langboard Inc.

- 6.4.12 Louisiana-Pacific Corporation

- 6.4.13 Pfleiderer

- 6.4.14 Roseburg Forest Products

- 6.4.15 Swiss Krono Group

- 6.4.16 West Fraser

- 6.4.17 Weyerhaeuser Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment