Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683494

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1683494

United States Animal Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 249 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

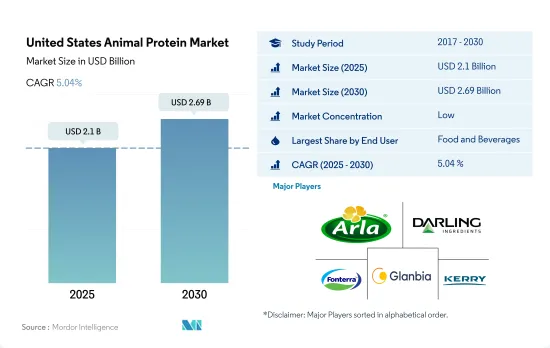

The United States Animal Protein Market size is estimated at 2.1 billion USD in 2025, and is expected to reach 2.69 billion USD by 2030, growing at a CAGR of 5.04% during the forecast period (2025-2030).

Rising health concerns in the country influence the use of high-protein ingredients in various segments

- The F&B segment, majorly the snacks sub-segment, dominated the market in terms of growth rate, and it is expected to register a CAGR of 2.28%, by value, during the forecast period. Animal protein, in particular, is becoming more and more popular with consumers, impacting all food and beverage sectors. The demand for protein snacks is particularly strong, with 1 in 4 US consumers indicating "high in protein" as a very important attribute in 2022 when deciding which snacks to consume, which is especially true for millennial consumers. Consumers seek protein snacks for various reasons, including satiety, energy, muscle support, weight loss, healthy aging, and general nutrition.

- The supplement segment is the major segment in the market after F&B, and it is expected to record a CAGR of 5.55%, by value, during the forecast period. By supplement type, sports nutrition saw the highest demand due to its functionalities like growth, repair, and strengthening of muscular tissue. In the United States, 36.5% of adults are obese, and 32.5% are overweight. More than two-thirds of adults in the United States were overweight or obese in 2021. Around 45 million adults (approximately 14% of the population) had a gym membership or fitness center membership in 2021. Rising health concerns, higher obesity prevalence, and a rise in health clubs led to increased demand for these products.

- The Y-o-Y growth rate of the F&B segment increased to 0.68%, by value, in 2021. It was mainly due to the US food price index for meat, poultry, and fish, which increased by 4.3%, and the cereal and bakery index increased by 2.9% in 2021.

United States Animal Protein Market Trends

The consumption growth of animal protein fuels opportunities for key players in the ingredients segment

- Despite the rising vegan population, the demand for animal protein has been steady in the United States. The majority of protein in the American diet comes from beef and poultry, followed by dairy. In 2022, 80% of US adult consumers preferred pork, beef, poultry, and fish as their main sources of protein. Due to its water-binding properties, the market is majorly driven by the growing usage of gelatin in the functional food industry. Consumers continue to demand traditional protein options, but they are signaling an expectation of the animal protein industry to do more to address environmental concerns.

- With a wide range of applications and consumer preferences toward a healthy lifestyle, many US ingredient manufacturers are trying to enter the collagen market, which is the major reason for the increase in per capita consumption patterns. From 2019 to 2021, the unadjusted prevalence of doctor-diagnosed arthritis in the United States was 24.2% among women and 17.9% among men. Due to the high incidence of arthritis in the area, there is a growing need for collagen-based supplements to support bone and joint health.

- Over the years, considerable research has proven that animal protein has a higher biological value than plant protein. In the Protein Digestibility-corrected Amino Acid Score proposed by the Food and Agricultural Organization, milk and whey protein scored 1, indicating that the protein would provide 100% (or more) of all the amino acids required in the diet. On the contrary, plant sources lack one or more amino acids, with delayed digestibility. This factor is driving athletes and fitness enthusiasts to consume animal-based protein.

Meat and milk production contributes majorly as raw material for animal protein ingredients

- The graph given depicts the production data for raw materials such as meat of cattle, pigs, and chicken (with bone, fresh or chilled), raw milk from cattle and goats, skim milk from cows, and dry whey powder. In 2023, 24,087 pounds of milk was produced per cow, an increase of 1.30% from 23,777 pounds in 2020. As of 2022, the average number of milk cows in the United States was 9,402. Milk is usually separated through various processes into components and processed into fluid beverage milk or the manufacture of other dairy products.

- The United States is the world's largest producer of chicken meat and accounted for a 20% share of global chicken meat production in 2023. The meat production and processing sector is estimated to benefit from government initiatives such as 'Biden-Harris Administration's Action Plan," which has been introduced to support the development of a fairer, more competitive, and more resilient meat and poultry supply chain in the country. The US Department of Agriculture made USD 32 million in grants to 167 existing meat and poultry processing facilities to help them reach more customers.

- Cattle meat is one of the most common sources of collagen, providing a significant amount of this unique protein. On average, beef has approximately 2-3% collagen in its composition. With the largest fed-cattle industry in the world, the United States is also the world's largest producer of cattle meat, primarily high-quality, grain-fed cattle meat for domestic and export use. Beef cattle are raised in all 50 states of the United States, with Texas, Oklahoma, Missouri, Nebraska, South Dakota, Kansas, and Montana as the leading cattle meat-producing states in the country as of July 2023.

United States Animal Protein Industry Overview

The United States Animal Protein Market is fragmented, with the top five companies occupying 22.60%. The major players in this market are Arla Foods amba, Darling Ingredients Inc., Fonterra Co-operative Group Limited, Glanbia PLC and Kerry Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90069

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Animal

- 3.3 Production Trends

- 3.3.1 Animal

- 3.4 Regulatory Framework

- 3.4.1 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Protein Type

- 4.1.1 Casein and Caseinates

- 4.1.2 Collagen

- 4.1.3 Egg Protein

- 4.1.4 Gelatin

- 4.1.5 Insect Protein

- 4.1.6 Milk Protein

- 4.1.7 Whey Protein

- 4.1.8 Other Animal Protein

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 RTE/RTC Food Products

- 4.2.2.1.8 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Agropur Dairy Cooperative

- 5.4.2 Ajinomoto Co. Inc.

- 5.4.3 AMCO Proteins

- 5.4.4 Arla Foods amba

- 5.4.5 Baotou Dongbao Bio-tech Co. Ltd

- 5.4.6 Darling Ingredients Inc.

- 5.4.7 Enterra Corporation

- 5.4.8 ETChem

- 5.4.9 Farbest-Tallman Foods Corporation

- 5.4.10 Fonterra Co-operative Group Limited

- 5.4.11 Gelita AG

- 5.4.12 Glanbia PLC

- 5.4.13 Groupe Lactalis

- 5.4.14 Kerry Group PLC

- 5.4.15 Milk Specialties Global

- 5.4.16 Symrise AG

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.