PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911704

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911704

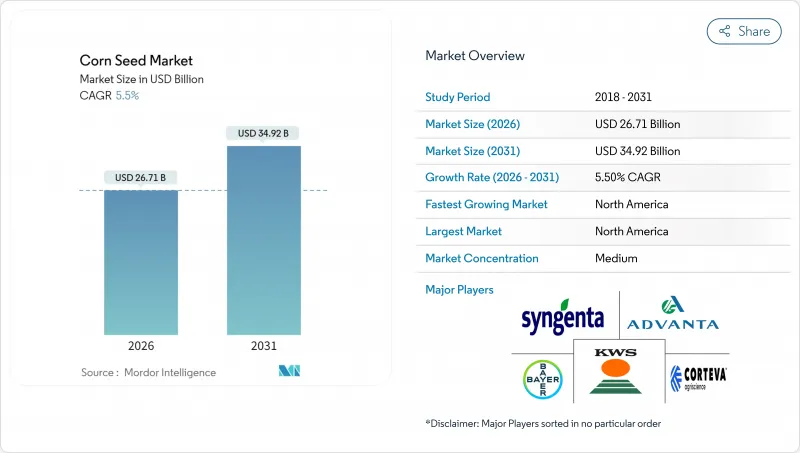

Corn Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The corn seed market was valued at USD 25.32 billion in 2025 and estimated to grow from USD 26.71 billion in 2026 to reach USD 34.92 billion by 2031, at a CAGR of 5.50% during the forecast period (2026-2031).

Hybrid replacement cycles are shortening, stacked-trait technologies are commanding premium prices, and digital agronomy services are becoming integral to seed packages, together accelerating revenue growth across all major growing regions. Climate variability is fueling demand for drought- and heat-tolerant germplasm, while faster regulatory pathways for gene-edited events are reshaping product pipelines. Precision-agriculture platforms that link genetics, prescriptions, and input logistics are deepening supplier-farmer relationships and raising switching costs. At the same time, low-cost direct-to-farmer channels are unlocking underserved smallholder segments, widening the corn seed market base.

Global Corn Seed Market Trends and Insights

High Adoption of Stacked-Trait Transgenic Hybrids

Stacked-trait hybrids capture the maximum percentage of North American seed sales because they integrate herbicide tolerance with multiple Bt proteins that curb pest damage and simplify weed control. Bayer's SmartStax PRO platform, launched across key corn belt states, demonstrates yield advantages of 8-12% over single-trait alternatives under high pest pressure conditions. Approval timelines in Argentina and Brazil have narrowed to roughly 24 months for products with proven safety records, hastening commercial launches. Competitive positioning now depends on stacking breadth as well as refuge-in-a-bag convenience. As more farmers prioritize agronomic simplicity, the corn seed market continues to migrate toward multi-trait packages that protect profit margins. Adoption strength in major export countries also influences trait preference in import-dependent regions that benchmark technology performance on the United States and Brazilian acreage.

Rapid Mechanization and Hybrid Replacement Cycles

India's agricultural machinery subsidies, expanded under the Sub-Mission on Agricultural Mechanization, have increased combine harvester adoption by 35% since 2022, enabling farmers to plant newer hybrid varieties with improved standability characteristics. Similar patterns are emerging in Kenya, Ghana, and Nigeria through development-bank equipment programs, stimulating fresh demand for machine-friendly hybrids with sturdy stalks and synchronized maturity. Shorter life cycles enlarge the cumulative corn seed market by prompting faster turnover of each farmer's preferred germplasm. Breeders with robust screening programs for mechanical harvesting tolerance gain a competitive edge because farmers replace older lines more frequently. The transition also amplifies data flow on hybrid performance, reinforcing localized breeding decisions and boosting adoption of higher-value seed classes.

Trait-Royalty Concentration Pushing Retail Seed Prices Upward

Patent clustering among three biotechnology leaders increased trait royalty fees between 2020 and 2024, driving retail seed prices beyond the reach of smallholders in emerging economies. Licensing costs now account for shelf prices in premium transgenic hybrids, limiting volume expansion in cost-constrained regions. Antitrust probes in Brazil and India highlight competition concerns but have yet to yield remedies, sustaining pricing power for incumbents. As farmers weigh input costs, some revert to conventional hybrids or saved seed, tempering growth in technology-intensive tiers of the corn seed market. End-user pushback is influencing public-sector breeding programs to develop royalty-free alternatives for marginal zones.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Precision-Agriculture Platforms Bundling Seed and Digital Agronomy

- Accelerated Regulatory Fast-Track for Gene-Edited Corn Varieties

- Escalating Pest Resistance to Bt Toxins Driving Costly R&D Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid seed commanded 90.12% of total sales in 2025, confirming its position as the cornerstone of the corn seed market. Transgenic hybrids with stacked herbicide-tolerant and insect-resistant traits constitute this category, leveraging multi-trait packages that simplify in-field weed and pest control. Adoption spreads fastest among commercial growers in the United States, Brazil, and Argentina, where digital agronomy tools validate hybrid return on investment through geospatial mapping. Non-transgenic hybrids retain relevance in organic systems and GMO-regulated zones, anchored by strong demand across select European states. Meanwhile, premium protein and waxy corn variants are carving out specialty niches, aided by gene-editing edits that avoid transgenic triggers.

Open-pollinated varieties plus hybrid derivatives are expanding at a 5.78% CAGR, propelled by seed-saving benefits and lower capital requirements for subsistence farmers. Public-sector breeding programs contribute royalty-free germplasm that private dealers distribute through informal networks, extending reach into remote geographies. Combined, these dynamics keep the corn seed market diversified across technology classes, balancing high-margin biotech lines with volume-oriented traditional seeds.

The Corn Seed Market Report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), and Geography (Africa, Asia-Pacific, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

North America held 49.62% of the corn seed market share in 2025, and Asia-Pacific holds a modest share in the market. Chinese policy that now encourages foreign joint ventures, opening access to proprietary traits while maintaining local germplasm stewardship. In India, dealer-network expansion, coordinated with state subsidies, moved hybrid adoption, lifting average yields by nearly over traditional cultivars. Emerging economies such as Indonesia and Vietnam are transitioning to disease-tolerant tropical hybrids as feed demand for poultry and aquaculture intensifies. Regional breeding focus centers on downy mildew resistance, ear rot tolerance, and stability under monsoon variability, underpinning the sustained dominance of Asia-Pacific in the corn seed market.

North America is projected to grow at a 7.08% CAGR through 2031, the fastest among all regions, as precision-ag depth, gene-editing approvals, and agronomic service bundling reinforce premium pricing power. Mexico's dual structure accommodates both biotech-intensive commercial farms and native landrace cultivation, requiring suppliers to manage discrete product lines for divergent customer bases.

Regulatory clarity around gene-editing fosters rapid commercial rollout of traits like elevated amino-acid content, which taps feed-mill demand for nutrient-dense corn. Canada's warming prairie climate is extending corn suitability zones, further enlarging the corn seed market size in temperate latitudes. While Europe, South America, Africa, and the Middle East exhibit diverse demand patterns shaped by policy and climate, their combined uptake highlights the need for regionalized germplasm, tailored stewardship, and flexible licensing terms.

- Advanta Seeds - UPL

- Bayer AG

- Charoen Pokphand Group (CP Group)

- Corteva Agriscience

- Groupe Limagrain

- Hefei Fengle Seed Industry Co. Ltd

- Kaveri Seeds

- KWS SAAT SE & Co. KGaA

- Syngenta Group

- Yuan Longping High-Tech Agriculture Co. Ltd

- Stine Seed Company

- Mahyco

- DLF A/S

- Rijk ZwaaRijk Zwaan Zaadteelt en Zaadhandel B.V.

- Seed Co International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 High adoption of stacked-trait transgenic hybrids

- 4.6.2 Rapid mechanization and hybrid replacement cycles

- 4.6.3 Expansion of precision-ag platforms bundling seed and digital agronomy

- 4.6.4 Accelerated regulatory fast-track for gene-edited corn varieties

- 4.6.5 Climate-resilient seed demand amid rising drought and heat episodes

- 4.6.6 Emergence of low-cost direct-to-farmer e-commerce seed channels

- 4.7 Market Restraints

- 4.7.1 Trait-royalty concentration pushing retail seed prices upward

- 4.7.2 Escalating pest resistance to Bt toxins driving costly R&D cycles

- 4.7.3 Stringent GMO restrictions and coexistence rules

- 4.7.4 Proliferation of counterfeit seed undermining trust in certified channels

5 MARKET SIZE AND GROWTH FORECAST (VALUE AND VOLUME)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties and Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Geography

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Ghana

- 5.2.1.2.4 Kenya

- 5.2.1.2.5 Nigeria

- 5.2.1.2.6 South Africa

- 5.2.1.2.7 Tanzania

- 5.2.1.2.8 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Indonesia

- 5.2.2.2.6 Japan

- 5.2.2.2.7 Myanmar

- 5.2.2.2.8 Pakistan

- 5.2.2.2.9 Philippines

- 5.2.2.2.10 Thailand

- 5.2.2.2.11 Vietnam

- 5.2.2.2.12 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Saudi Arabia

- 5.2.4.2.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.5.2.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Charoen Pokphand Group (CP Group)

- 6.4.4 Corteva Agriscience

- 6.4.5 Groupe Limagrain

- 6.4.6 Hefei Fengle Seed Industry Co. Ltd

- 6.4.7 Kaveri Seeds

- 6.4.8 KWS SAAT SE & Co. KGaA

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

- 6.4.11 Stine Seed Company

- 6.4.12 Mahyco

- 6.4.13 DLF A/S

- 6.4.14 Rijk ZwaaRijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.15 Seed Co International

7 KEY STRATEGIC QUESTIONS FOR SEED CEOS