PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1835650

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1835650

Breakfast Cereals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

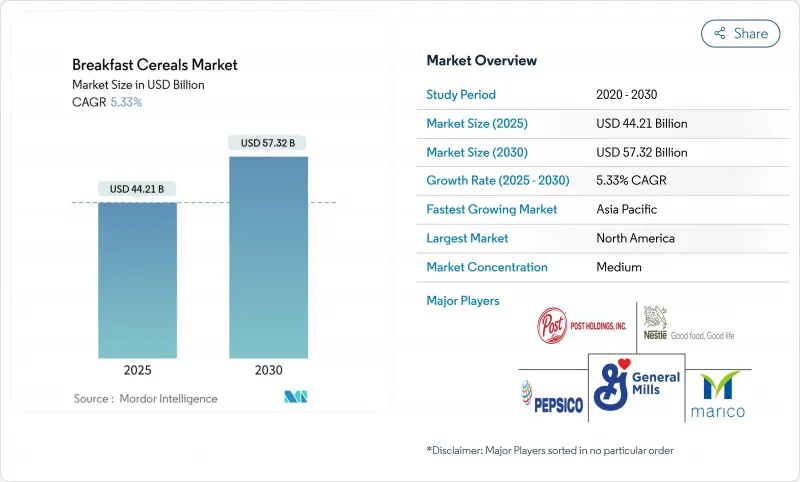

The global breakfast cereals market is valued at USD 44.21 billion in 2025 and is projected to reach USD 57.32 billion by 2030, growing at a compound annual growth rate (CAGR) of 5.33% during the forecast period (2025-2030).

The market growth is driven by changing consumer preferences, increased health consciousness, and demand for convenient breakfast options. The fast-paced modern lifestyle has increased the demand for ready-to-eat and hot cereal products that offer quick meal solutions. Consumers are seeking cereals with enhanced nutritional profiles, including those fortified with fiber, protein, whole grains, and probiotics, while preferring options with reduced sugar content. The market is also experiencing growth in plant-based, organic, and gluten-free varieties to meet specific dietary requirements. In addition, the rise of e-commerce and digital grocery platforms has improved product accessibility, particularly in developing markets, contributing to the market's expansion.

Global Breakfast Cereals Market Trends and Insights

Rising Demand for High-Protein Cereal Variants Among Consumers

The breakfast cereals market is experiencing a notable transition toward protein-enriched products, driven by increased consumer focus on nutrition and health. In December 2024, General Mills Inc. expanded its Cheerios portfolio by introducing Cheerios Protein, which contains 8 grams of protein per serving. This product launch reflects market trends, supported by the 2024 Food and Health Survey from the International Food Information Council, which revealed that 71% of consumers aim to increase their protein consumption . The protein cereal segment has gained particular momentum among millennial parents seeking both nutritional value and convenience, enabling manufacturers to implement premium pricing strategies. Manufacturers are also expanding their protein sources beyond dairy to include plant-based alternatives, addressing the growing flexitarian consumer base and creating new market opportunities in the breakfast cereal category.

Surge in Single-Serve Breakfast Habits Fueling On-the-Go Cereal Cups

The global breakfast cereals market is experiencing significant growth driven by increasing demand for single-serve and on-the-go breakfast formats, particularly cereal cups. This trend reflects the impact of urbanization and changing lifestyles among working professionals and students who have limited time for traditional breakfast meals. Single-serve cereal cups meet consumer needs by combining convenience with nutrition through portable, portion-controlled options that are easy to prepare. These formats are particularly popular in urban areas where consumers often eat breakfast during their commute or at work. Also, major cereal manufacturers are responding by diversifying their product lines with portable formats that incorporate ingredients such as granola, oats, seeds, and various milk options. The products feature improved packaging designs, including microwaveable containers, resealable lids, and recyclable materials, which enhance both functionality and environmental sustainability. For instance, in October 2024, Inventure launched four of its popular cereal flavors in a new 'on the go' cup format, designed for consumption at pre-school, office, or as a snack, requiring consumers to simply peel back the lid and add milk.

Volatile Oat and Corn Commodity Prices Compressing Margins

Cereal manufacturers face increasing margin pressure as key ingredient costs experience significant volatility, affecting pricing strategies and production planning. The Food and Agriculture Organization (FAO) forecasts global cereal trade to decline to 478 million tonnes in 2024/25, a 6.8% decrease from 2023/24. Agricultural adaptations, including stress-tolerant hybrids and improved farming practices, have partially offset grain price volatility caused by climate change and erratic weather patterns. However, market dynamics remain unstable. The United States Department of Agriculture (USDA) projects tightening supplies for key grains in 2024-25, despite minor increases in global wheat production. This supply constraint affects manufacturers with global supply chains, as regional production disruptions impact interconnected ingredient markets. Companies are managing these challenges through long-term supplier contracts, flexible ingredient formulations, and hedging programs to stabilize input costs.

Other drivers and restraints analyzed in the detailed report include:

- Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

- Private-Label Premiumization Driving Value Growth

- Intensifying Anti-Sugar Advocacy Affecting Cereal Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corn-based cereals hold a dominant 36.70% market share in 2024, benefiting from cost advantages and manufacturing efficiencies that enable competitive pricing in value segments. Oat-based products show the highest growth rate at 6.53% CAGR (2025-2030), supported by their established nutritional benefits and adaptability in both ready-to-eat (RTE) and ready-to-cook (RTC) formats. Technological advancements in oat processing have improved texture and flavor while maintaining nutritional value. The European Union leads global oats production at 33%, followed by Canada at 15% for 2024/25, according to the United States Department of Agriculture (USDA) . The regional consumption of oat-based breakfast cereals continues to increase, driven by consumer demand for nutritious, high-fiber breakfast products.

Wheat-based cereals continue to hold substantial market share, especially in flaked formats, while rice-based cereals gain traction in the gluten-free category. Barley remains limited to multi-grain formulations despite its nutritional benefits. Alternative grains, including quinoa and amaranth, show rapid growth in premium segments, though their overall market share remains small. This expanding range of grain sources reflects industry efforts to develop distinct products for specific dietary requirements, as demonstrated by Nestle's commitment to using whole grains as the primary ingredient in all their ready-to-eat cereals.

Ready-to-eat (RTE) cereals hold a dominant 75.23% market share in 2024, primarily due to their convenience for time-constrained households. Ready-to-cook (RTC) cereals are experiencing faster growth with a CAGR of 5.97% (2025-2030), as consumers increasingly view hot cereals as more nutritious and filling. Hot oatmeal, in particular, has gained popularity due to its health benefits and adaptability for customization with various toppings.

In the Ready-to-eat (RTE) segment, flakes remain the largest sub-segment, while granola and clusters show higher growth rates due to their wholesome ingredients and texture. Protein enrichment is driving new product development in this category. For example, in November 2024, FUEL10K introduced Multigrain Flakes in Chocolate and Red Berry flavors, featuring high-protein, high-fiber wholegrain wheat flakes. In the RTC segment, premium muesli and specialized porridge mixes are growing faster than basic oatmeal, indicating consumers' willingness to pay more for higher quality and enhanced nutritional benefits.

The Global Breakfast Cereal Market is Segmented by Product Type (Ready-To-Cook Cereals and Ready-To-Eat Cereals), Ingredient Source (Wheat, Corn, Oats, Rice, and More), Packaging Type (Boxes, Stand-Up Pouches, and More), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and More), by Age Group (Adults and Children), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds a 36.77% share of the global breakfast cereals market in 2024, supported by high per-capita consumption and extensive retail distribution networks. The region shows moderate growth as manufacturers develop value-added products to address volume challenges in mature segments. Health-oriented innovations, specifically protein-enriched varieties and reduced-sugar formulations, drive market expansion. The FDA's 2024 nutrition labeling requirements have enhanced transparency for added sugars, prompting manufacturers to adapt formulations to meet consumer preferences.

Asia-Pacific demonstrates the highest growth potential with a projected CAGR of 6.42% (2025-2030), supported by urbanization, increasing disposable incomes, and evolving dietary habits. China, India, and Southeast Asian countries show robust growth as urban consumers adopt Western-style breakfast options. International manufacturers are customizing products for local tastes while promoting nutritional benefits, establishing foundations for sustained market expansion.

Europe exhibits distinct regional consumption patterns and product preferences in a mature market environment. Consumers demonstrate high nutritional awareness, favoring organic, whole grain, and reduced-sugar products. The European Food Safety Authority's 2024 nutritional guidelines emphasize whole grain consumption and sugar reduction, affecting consumer choices and product formulations. Private label products maintain a significant market presence, with retailers developing competitive offerings across price segments. Eastern European markets present growth opportunities as rising disposable incomes support increased breakfast cereal consumption.

- General Mills Inc.

- Post Holdings Inc.

- Nestle S.A.

- PepsiCo Inc.

- Marico Ltd.

- Calbee Inc.

- Sanitarium Health & Wellbeing Company

- Nature's Path Foods

- Tata Consumer Products Limited

- The Hain Celestial Group, Inc.

- Bob's Red Mill Natural Foods

- Bagrrys India Limited

- Dr. Oetker GmbH

- Jordan's & Ryvita Company

- Rude Health Foods Ltd.

- Three Wishes Cereal

- Familia AG

- Hero AG

- Purely Elizabeth

- Shantis Food

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High-Protein Cereal Variants Among Consumers

- 4.2.2 Surge in Single-Serve Breakfast Habits Fueling On-the-Go Cereal Cups

- 4.2.3 Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

- 4.2.4 Private-Label Premiumization Driving Value Growth

- 4.2.5 Production Technology Advances Enhance Product Quality

- 4.2.6 Rising Children's Population Increases Nutritional Focus

- 4.3 Market Restraints

- 4.3.1 Volatile Oat and Corn Commodity Prices Compressing Margins

- 4.3.2 Intensifying Anti-Sugar Advocacy Affecting Cereal Sales

- 4.3.3 Environmental Concerns about Packaging

- 4.3.4 Supply Chain Issues and Raw Material Cost Fluctuations

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Ready-to-Eat Cereals

- 5.1.1.1 Flakes

- 5.1.1.2 Puffed Cereals

- 5.1.1.3 Granola and Clusters

- 5.1.1.4 Others (Coated/Sugar-Frosted Cereals, Shredded and Threaded)

- 5.1.2 Ready-to-Cook Cereals

- 5.1.2.1 Hot Oatmeal

- 5.1.2.2 Muesli and Porridge Mixes

- 5.1.2.3 Other Ready-to-Cook Cereals

- 5.1.1 Ready-to-Eat Cereals

- 5.2 By Ingredient Source

- 5.2.1 Wheat

- 5.2.2 Corn

- 5.2.3 Oats

- 5.2.4 Rice

- 5.2.5 Barley

- 5.2.6 Others

- 5.3 By Packaging Type

- 5.3.1 Boxes

- 5.3.2 Stand-Up Pouches

- 5.3.3 Cups and Bowls

- 5.3.4 Others (plastic jars, and bags, etc.)

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Specialty Stores

- 5.4.4 Online Retailers

- 5.4.5 Other Distribution Channels

- 5.5 By Age Group

- 5.5.1 Adults

- 5.5.2 Children

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Poland

- 5.6.2.8 Belgium

- 5.6.2.9 Sweden

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Indonesia

- 5.6.3.6 South Korea

- 5.6.3.7 Thailand

- 5.6.3.8 Singapore

- 5.6.3.9 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Peru

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Egypt

- 5.6.5.6 Morocco

- 5.6.5.7 Turkey

- 5.6.5.8 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Mills Inc.

- 6.4.2 Post Holdings Inc.

- 6.4.3 Nestle S.A.

- 6.4.4 PepsiCo Inc.

- 6.4.5 Marico Ltd.

- 6.4.6 Calbee Inc.

- 6.4.7 Sanitarium Health & Wellbeing Company

- 6.4.8 Nature's Path Foods

- 6.4.9 Tata Consumer Products Limited

- 6.4.10 The Hain Celestial Group, Inc.

- 6.4.11 Bob's Red Mill Natural Foods

- 6.4.12 Bagrrys India Limited

- 6.4.13 Dr. Oetker GmbH

- 6.4.14 Jordan's & Ryvita Company

- 6.4.15 Rude Health Foods Ltd.

- 6.4.16 Three Wishes Cereal

- 6.4.17 Familia AG

- 6.4.18 Hero AG

- 6.4.19 Purely Elizabeth

- 6.4.20 Shantis Food

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK