PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836435

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836435

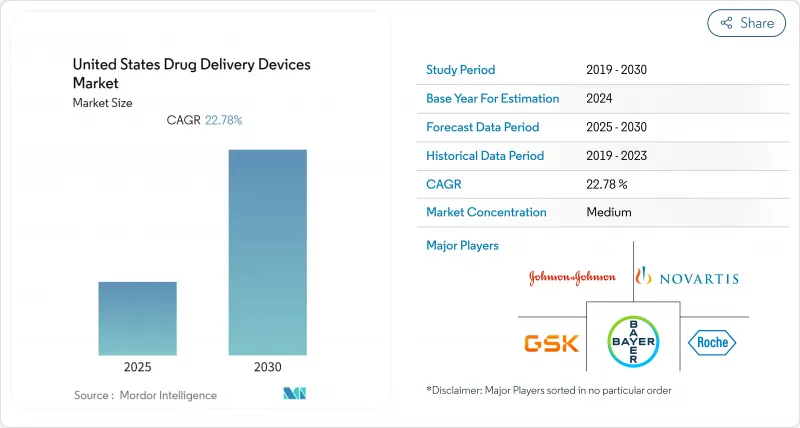

United States Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States drug delivery devices market is valued at USD 51.24 billion in 2025 and is forecast to reach USD 75.20 billion by 2030, expanding at a 6.71% CAGR.

Growth is grounded in the nation's rising chronic-disease burden, continual product innovation, and a decisive pivot toward patient-centric therapy that favors self-administration and home care.[1]Traditional modalities remain relevant, yet device makers are layering connectivity, sensors, and analytics onto proven platforms to improve adherence and real-world outcomes. Hospitals continue to anchor demand, but reimbursement trends and high deductibles are funneling volume into ambulatory clinics and living rooms, reshaping channel economics. Competitive intensity is sharpening around biologics-ready injectors, smart inhalation systems, and on-body pumps that reduce clinic visits. At the same time, the FDA's Digital Health Advisory Committee is shortening feedback loops for software-driven devices while maintaining a stringent safety bar, creating both opportunity and compliance cost for innovators.

United States Drug Delivery Devices Market Trends and Insights

Rise in Self-Administration Preferences Driven by High Patient Deductibles and Telehealth Adoption

Demand for convenient dosing formats is accelerating as patients shoulder higher out-of-pocket costs. Telehealth visits rose sharply during the pandemic and remain elevated, enabling clinicians to coach users on connected pens, pumps, and inhalers without in-person training. Hospitals, facing USD 115 billion in 2023 drug spend, encourage take-home therapies to trim length-of-stay and pharmacy overhead. The FDA's April 2025 clearance of CT-132, a digital therapeutic for migraine, underscores momentum for software-enhanced regimens that transfer care into the home. Continuous glucose monitoring now starts earlier in diabetes journeys, aligning device selection with individual lifestyle and boosting confidence in self-managed dosing.

Expanding Biologics Pipeline Necessitating Advanced Parenteral Delivery Platforms

Large-molecule therapies represent a growing share of FDA approvals, demanding devices that maintain viscosity control, temperature stability, and precise micro-dosing[1]. Wearable injectors capable of 5-10 mL subcutaneous delivery are entering trials, offering at-home alternatives to infusion centers. Early device strategy is now embedded in molecule design as drug makers weigh formulation viscosity against patient comfort. Contract manufacturers with polymer expertise enjoy a widening moat, especially in Boston-area and Bay-area biotech clusters. Industry attention to biologics-ready systems expanded further after AstraZeneca highlighted lipid nanoparticle and oral biologic platforms in its pipeline update.

Stringent FDA Premarket Review for Combination Products Extending Time-to-Market

Approval cycles for novel drug-device combinations can stretch to 36 months, straining venture-backed developers. Draft user-fee legislation aims to streamline reviews but will introduce new documentation layers in the near term. Firms now integrate regulatory specialists early in concept design, adding cost and prolonging R&D. Larger incumbents with established quality systems widen competitive distance as smaller entrants wrestle with documentation rigor. Any leadership turnover or budget pressure at FDA may influence review cadence and resource allocation.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancement and Product Innovation

- High Burden of Chronic Disease

- Reimbursement Uncertainty for Digital Companion Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inhalers record the fastest 9.13% CAGR, outpacing the broader United States drug delivery devices market yet still trailing Syringes and Needles that hold 30.34% share. This surge stems from propellant redesigns and digital dose-counters that assure correct technique, critical for the 25 million Americans managing asthma. GSK's low-carbon Ventolin prototype positions sustainability as a new differentiator.

Momentum in inhalation technology is steering investment into soft-mist and dry-powder platforms capable of systemic delivery of biologics. Needle-free injectors now attract users with strong aversion to sharps, while auto-injectors and pens leverage spring-loaded mechanics for precise biologic dosing at home. Implantable pumps fill long-term therapy niches such as ophthalmology inserts reviewed by the FDA in February 2025. These diverse modalities enlarge the addressable base and reduce single-technology dependence within the United States drug delivery devices market.

Injectables retained 42.12% share of the United States drug delivery devices market size in 2024 due to compatibility with biologics. Yet topical systems grow at 7.88% thanks to permeation enhancers, microneedle patches, and polymer films that deliver peptides through skin layers. Regulatory nods for migraine nasal sprays and ocular refillable implants demonstrate expanding options beyond needles.

Oral dosage formats remain favored for small molecules, supported by innovations in bioavailability boosters. Pulmonary delivery methods broaden into systemic applications, and transdermal GLP-1 patches target the obesity epidemic. Together these shifts diversify modality risk and spread growth vectors across the United States drug delivery devices market.

The United States Drug Delivery Devices Market Report is Segmented by Device Type (Inhalers, Transdermal Patch, and More), Route of Administration (Injectable, Topical, and More), Technology (Sustained/Controlled Release System, Targeted/Site-Specific Delivery, and More), Application (Diabetes, Cancer and More), and End Users (Hospitals, Ascs, and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beckton Dickinson

- Solventum

- Johnson & Johnson

- Medtronic

- West Pharmaceutical Services

- Insulet

- Baxter

- Boston Scientific

- Terumo

- Gerresheimer

- Ypsomed

- Tandem Diabetes Care

- Antares Pharma (a Halozyme company)

- Pfizer

- Roche

- Bayer

- Sanofi

- GlaxoSmithKline

- Eli Lilly and Company

- Novo Nordisk

- AstraZeneca

- Teva Pharmaceutical Industries

- AptarGroup, Inc.

- The Cooper Companies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Self-Administration Preferences Driven by High Patient Deductibles and Telehealth Adoption

- 4.2.2 Expanding Biologics Pipeline Necessitating Advanced Parenteral Delivery Platforms

- 4.2.3 Technological Advancement and Product Innovation

- 4.2.4 High Burden of Chronic Disease

- 4.2.5 Increased Use of Advanced and Connected Drug Delivery Devices

- 4.2.6 CMS Home-Infusion Therapy Benefit and Hospital-at-Home Programs Fueling Demand for Portable Infusion Pumps

- 4.3 Market Restraints

- 4.3.1 Stringent FDA Premarket Review for Combination Products Extending Time-to-Market

- 4.3.2 Reimbursement Uncertainty for Digital Companion Applications

- 4.3.3 Rising Needlestick Injury Litigation Elevating Liability Insurance Premiums

- 4.3.4 Persistent Shortages of Medical-Grade Silicone and Specialty Polymers Disrupting Device Manufacturing Schedules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Inhalers

- 5.1.2 Transdermal Patches

- 5.1.3 Infusion Pumps

- 5.1.4 Syringes & Needles

- 5.1.5 Injection Pens

- 5.1.6 Auto-Injectors

- 5.1.7 Needle-Free Injectors

- 5.1.8 Implantable Drug Delivery Devices

- 5.1.9 Others

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Topical

- 5.2.3 Oral

- 5.2.4 Pulmonary

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.2.7 Others

- 5.3 By Technology

- 5.3.1 Sustained / Controlled Release Systems

- 5.3.2 Targeted / Site-Specific Delivery

- 5.3.3 Biodegradable / Bioresorbable Systems

- 5.3.4 Smart & Connected Drug Delivery Devices

- 5.3.5 Needle-less Technologies

- 5.4 By Application

- 5.4.1 Diabetes

- 5.4.2 Cancer

- 5.4.3 Cardiovascular Diseases

- 5.4.4 Respiratory Diseases

- 5.4.5 Central Nervous System Disorders

- 5.4.6 Infectious Diseases

- 5.4.7 Others

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers (ASCs)

- 5.5.3 Home Healthcare Settings

- 5.5.4 Clinics and Physician Offices

- 5.5.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Becton, Dickinson and Company

- 6.4.2 Solventum

- 6.4.3 Johnson & Johnson

- 6.4.4 Medtronic plc

- 6.4.5 West Pharmaceutical Services, Inc.

- 6.4.6 Insulet Corporation

- 6.4.7 Baxter International Inc.

- 6.4.8 Boston Scientific Corporation

- 6.4.9 Terumo Corporation

- 6.4.10 Gerresheimer AG

- 6.4.11 Ypsomed AG

- 6.4.12 Tandem Diabetes Care, Inc.

- 6.4.13 Antares Pharma (a Halozyme company)

- 6.4.14 Pfizer Inc.

- 6.4.15 F. Hoffmann-La Roche Ltd.

- 6.4.16 Bayer AG

- 6.4.17 Sanofi

- 6.4.18 GlaxoSmithKline plc

- 6.4.19 Eli Lilly and Company

- 6.4.20 Novo Nordisk A/S

- 6.4.21 AstraZeneca plc

- 6.4.22 Teva Pharmaceutical Industries Ltd.

- 6.4.23 AptarGroup, Inc.

- 6.4.24 CooperSurgical, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment