PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836436

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836436

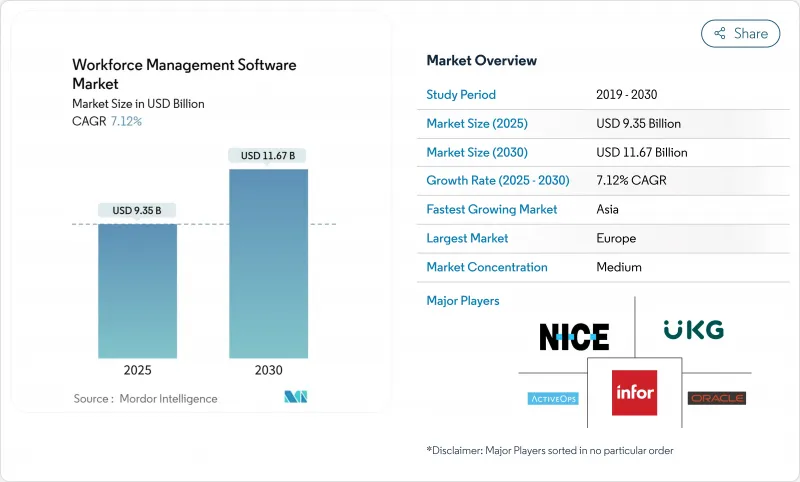

Workforce Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The workforce management software market is valued at USD 9.35 billion in 2025 and is projected to reach USD 11.67 billion by 2030, expanding at a 7.12% CAGR.

Growth stems from clear gains in labor-cost visibility, automated compliance, and the infusion of artificial intelligence into time-and-attendance cores, all of which elevate workforce optimization from routine administration to a board-level priority. Vendors that link predictive scheduling, real-time payroll, and analytics in one platform are capitalizing on demand for connected employee-experience ecosystems. Cloud deployment dominates new spending because hybrid and remote work require anytime access, while mobile interfaces unlock adoption in frontline sectors ranging from on-site retail to healthcare. Simultaneously, biometric authentication and predictive analytics help large enterprises cut overtime by double-digit percentages, convincing chief financial officers that streamlined labor orchestration is a direct profit lever.

Global Workforce Management Software Market Trends and Insights

AI-driven Labor Forecasting Pilots Accelerate Adoption in EU Shift-based Industries

European factories that trial predictive scheduling have lowered overtime outlays by up to 25% while tightening production windows, especially in automotive and consumer goods segments where demand fluctuates weekly. Paycor's 2024 AI assistant embeds these forecasts directly into roster creation, giving planners a two-week view of required headcount. Management teams note that cross-referencing predicted orders, skill profiles, and wage tiers within one algorithm curtails last-minute agency labor and bolsters margin resilience during supply-chain shocks. As European labor markets tighten further, boards are funding AI pilots not as experimental budgets but as core operational upgrades tied to productivity KPIs. The result is faster decision cycles and demonstrable reductions in unplanned downtime, pushing AI scheduling from a niche add-on to a default capability in midscale factories.

Mobile-first WFM Penetration in Southeast Asian Multi-site Retail Chains

Retail groups in Indonesia, Thailand, and the Philippines are rolling out mobile workforce apps that re-align staffing levels with real-time footfall, weather shifts, and regional festivals. Rippling's March 2025 offline kiosk functionality allows clock-in without broadband, solving the connectivity gap that has stalled SaaS rollouts in secondary cities. Headquarters gain unified labor-cost dashboards across hundreds of stores, letting executives benchmark productivity metrics that were once trapped in spreadsheets. Early adopters report single-digit percentage increases in conversion rates because floor managers can swap shifts on the fly when traffic spikes. As regulations diverge across ASEAN member states, mobile solutions that embed local labor rules while feeding consolidated analytics to corporate finance teams are rapidly becoming table stakes for cross-border retailers.

Legacy MES/ERP Integration Costs among German Mittelstand Manufacturers

Specialty manufacturers in Baden-Wurttemberg operate aging manufacturing execution systems that lack modern APIs, forcing custom connectors that swallow up to 20% of the annual IT budget when linking to cloud scheduling engines.Management faces a dilemma: the efficiency upside of real-time labor orchestration is clear, yet payback horizons lengthen when bespoke middleware and data-quality remediation are added. Consequently, tier-one automotive suppliers proceed, while smaller toolmakers postpone upgrades, widening intra-sector productivity disparities. Vendors seeking German market share are responding with low-code integration hubs and success-based pricing to de-risk budgets, but widespread conversion remains a long-run challenge.

Other drivers and restraints analyzed in the detailed report include:

- GCC Healthcare Staffing Shortages Spur Cloud-based WFM Investments

- Emergence of Blockchain-Based Tokenization Enabling Fractional Real-Estate Deals in Asia

- China's Data Residency Rules Limiting Foreign SaaS WFM Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is on track for a 12.5% CAGR, outpacing mature software licenses, as enterprises view successful workforce transformation as a holistic change-management journey rather than a technology procurement. Implementation workshops, role-based training, and continuous optimization programs now anchor multi-year contracts, converting vendors into long-term advisers. The workforce management software market size for services is projected to expand materially as boards allocate operating-expenditure budgets toward recurring value realization rather than capital-expenditure line items. Partner ecosystems that bundle HR consulting with compliance audits are closing deals faster because buyers seek one accountable owner for outcomes.

Software retains 62% revenue because unified suites that integrate attendance, scheduling, and analytics reduce the integration overhead that once favored best-of-breed point solutions. Vendors embed machine learning modules and pre-built regulatory content to increase stickiness. This model shores up gross margins and raises switching costs, ensuring that the workforce management software market continues to prize breadth and depth of functionality. Providers that balance platform scale with high-touch advisory services are pulling ahead in renewal cycles.

Time and Attendance remains foundational, yet Workforce Analytics is registering the strongest 14% CAGR as executive teams demand forward-looking insights rather than retrospective compliance logs. Analytics engines now merge internal shift data with external signals-economic indices, weather feeds, and holiday calendars-to predict staffing demand within 2-percentage-point accuracy. Segments that harness predictive turnover scores report reducing recruitment spend by low-double-digit percentages, validating analytics as a cost-containment lever. Expense justification is easier when dashboards tie labor efficiency gains directly to operating-margin improvements.

The workforce management software market share for Time and Attendance stays compelling at 27% because regulators worldwide tighten record-keeping and payroll mandates. Biometric clock-in curbs buddy punching, while AI video verification guards against spoofing in dispersed workforces. Scheduling modules increasingly serve as orchestration layers that weigh skill credentialing, labor-law ceilings, and employee preferences simultaneously. As organizations move toward outcome-based scheduling, fatigue management embedded in analytics towers elevates workplace safety and employer-brand equity.

Workforce Management Software Market is Segmented by Component (Software, Services), Software Type (Time and Attendance Management, Workforce Scheduling, and More), Deployment Mode (Cloud, On-Premises), Organization Size (Large Enterprises, Smes), End-Use Industry (BFSI, Consumer Goods and Retail, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe contributes 30% of 2024 global revenue, underpinned by stringent labor legislation and early adoption of AI-led forecasting engines. Executives appreciate platforms that bake national overtime thresholds, works-council agreements, and GDPR protocols directly into scheduler logic. Nevertheless, algorithmic management faces union scrutiny, with French and Swedish labor groups pushing for transparency safeguards. Germany's integration hurdles slow uptake among Mittelstand firms, yet large automotive and pharma conglomerates continue to pilot advanced modules, signaling long-run demand.

Asia-Pacific is the fastest mover with a 16.1% CAGR to 2030. In China, local vendors exploit residency rules to win state-owned enterprises, while foreign providers negotiate joint cloud ventures to remain relevant. Southeast Asian retailers leapfrog legacy systems via mobile-first SaaS, and Australian statutory reporting mandates coax organizations toward integrated suites. Simultaneously, broadband gaps in emerging markets constrain real-time services, but World Bank-backed fiber projects covering 160 million new users since 2019 are expected to ease constraints by 2027.

North America keeps a solid growth clip through sustained enterprise modernization and an innovation pipeline of AI scheduling startups. Logistics hubs in Brazil and Colombia deploy biometric time clocks to curb payroll fraud, indicating South American potential when connectivity and compliance frameworks stabilize. In the Middle East, Vision announcements and elevated oil revenues fund hospital expansions and smart-city pilots that embed workforce orchestration at the design phase, demonstrating that regional investments increasingly assume modern WFM as infrastructure.

- ActiveOps PLC

- NICE Ltd.

- Infor Group

- Oracle Corporation

- UKG Inc.

- SAP SE

- ADP LLC

- Blue Yonder Group, Inc. (Panasonic)

- IBM Corporation

- Workday Inc.

- Reflexis Systems Inc. (Zebra)

- SISQUAL Workforce Management, Lda

- ServiceMax Inc.

- Atoss Software AG

- Mitrefinch Ltd (Advanced)

- Deputy Group Pty Ltd

- 7shifts Employee Scheduling Software Inc.

- Sage Group plc

- Roubler Australia Pty Ltd

- tamigo ApS

- Verint Systems Inc.

- ClickSoftware (Salesforce Field Service)

- Ceridian HCM Holding Inc.

- Humanity (TCP Software)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven Labor Forecasting Pilots Accelerate Adoption in EU Shift-based Industries

- 4.2.2 Mobile-first WFM Penetration in Southeast Asian Multi-site Retail Chains

- 4.2.3 GCC Healthcare Staffing Shortages Spur Cloud-based WFM Investments

- 4.2.4 Real-time Payroll Tax Reporting Mandates in Australia and New Zealand Boost Integrated Suites

- 4.2.5 Biometric Time and Attendance to Curb Payroll Fraud in South American Logistics Hubs

- 4.3 Market Restraints

- 4.3.1 Legacy MES/ERP Integration Costs among German Mittelstand Manufacturers

- 4.3.2 China's Data Residency Rules Limiting Foreign SaaS WFM Deployments

- 4.3.3 Unreliable Broadband Infrastructure Hindering Cloud Adoption in Sub-Saharan Africa

- 4.3.4 French Union Pushback Against Algorithmic Shift Scheduling

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

- 4.9 Investment Analysis (Capital Flow and VC Funding Trends)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Software Type

- 5.2.1 Time and Attendance Management

- 5.2.2 Workforce Scheduling

- 5.2.3 Workforce Analytics

- 5.2.4 Absence and Leave Management

- 5.2.5 Fatigue and Task Management

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premise

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-use Industry

- 5.5.1 BFSI

- 5.5.2 Consumer Goods and Retail

- 5.5.3 Automotive

- 5.5.4 Energy and Utilities

- 5.5.5 Healthcare

- 5.5.6 Manufacturing

- 5.5.7 IT and Telecommunications

- 5.5.8 Logistics and Transportation

- 5.5.9 Other Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ActiveOps PLC

- 6.4.2 NICE Ltd.

- 6.4.3 Infor Group

- 6.4.4 Oracle Corporation

- 6.4.5 UKG Inc.

- 6.4.6 SAP SE

- 6.4.7 ADP LLC

- 6.4.8 Blue Yonder Group, Inc. (Panasonic)

- 6.4.9 IBM Corporation

- 6.4.10 Workday Inc.

- 6.4.11 Reflexis Systems Inc. (Zebra)

- 6.4.12 SISQUAL Workforce Management, Lda

- 6.4.13 ServiceMax Inc.

- 6.4.14 Atoss Software AG

- 6.4.15 Mitrefinch Ltd (Advanced)

- 6.4.16 Deputy Group Pty Ltd

- 6.4.17 7shifts Employee Scheduling Software Inc.

- 6.4.18 Sage Group plc

- 6.4.19 Roubler Australia Pty Ltd

- 6.4.20 tamigo ApS

- 6.4.21 Verint Systems Inc.

- 6.4.22 ClickSoftware (Salesforce Field Service)

- 6.4.23 Ceridian HCM Holding Inc.

- 6.4.24 Humanity (TCP Software)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment