PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836438

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836438

Global Ostomy Drainage Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

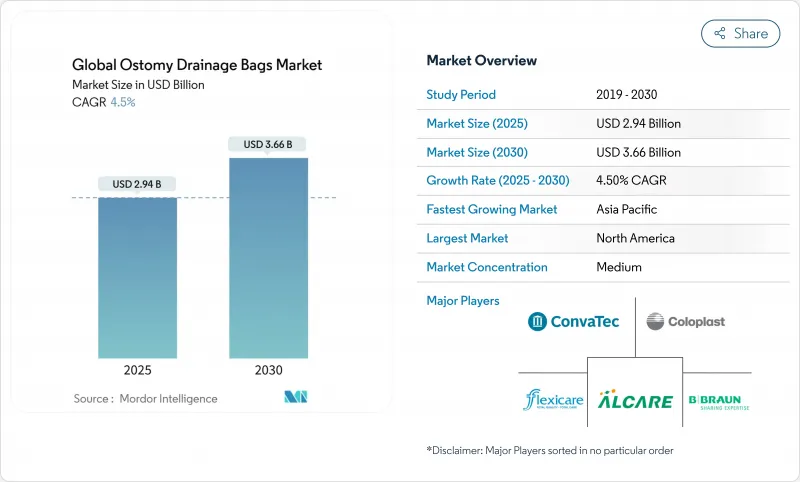

The Ostomy drainage bags market size stands at USD 2.94 billion in 2025 and is forecast to reach USD 3.66 billion by 2030, translating to a steady 4.5% CAGR.

Demographic momentum is the core catalyst, as an expanding pool of older surgical candidates carries higher comorbidity levels that lengthen postoperative ostomy usage. Converging with age trends, the global rise in inflammatory bowel disease and cancer surgeries keeps procedural volumes on an upward path, while smart-sensor pouches reposition the category as part of digital health rather than a commodity appliance. Subscription-based home-delivery services improve adherence and cut stock-out risk, and healthcare sustainability rules encourage fresh research into recyclable films and hydrocolloid blends. Together, these forces shape a predictable but opportunity-rich environment for both incumbents and new entrants in the Ostomy drainage bags market.

Global Ostomy Drainage Bags Market Trends and Insights

Increasing Incidence of Inflammatory Bowel Disease

New epidemiological updates confirm that ulcerative colitis and Crohn's disease continue to affect a wider segment of adults and seniors, prompting earlier and more frequent ostomy interventions. Specialist centers in North America already treat well over 2.5 million residents living with IBD, and clinicians expect the present caseload to tilt further toward patients aged over 60. Payer databases show that direct IBD care costs now exceed USD 27 billion annually in the United States, much of which relates to surgical diversion episodes that necessitate advanced pouching systems. Emerging economies such as India and China register rapid year-over-year jumps in newly diagnosed IBD yet have limited stoma-care infrastructure, creating a high-growth frontier for the Ostomy drainage bags market. Device developers therefore tailor portfolio extensions that address both the high-volume basic segment and specialist lines for hard-to-seal peristomal skin. Heightened clinical attention on quality-of-life metrics further elevates demand for products with secure adhesives, thin profiles and user-friendly closures.

Rapidly Growing Aging Population

Hospital discharge records for 2024 show a noticeable shift toward older and heavier surgical candidates, with four in every five elective colorectal operations now involving a patient who presents above normal BMI levels . Higher age correlates with greater ostomy-related complications such as skin irritation, herniation and leakage anxiety, expanding the requirement for premium hydrocolloid barriers that flex with abdominal contour changes. Diabetes prevalence among surgical patients is climbing past 15%, adding wound-healing challenges that push clinicians toward longer-wear pouches incorporating antibacterial layers. Home-based tele-monitoring garners acceptance among geriatric users, with recent studies showing 95% concordance between remote and bedside stoma assessments, a finding that strengthens reimbursement arguments for connected devices. Collectively, these dynamics add meaningful incremental volume to the Ostomy drainage bags market while also raising the average selling price through technology-rich features.

Unstructured or Shrinking Reimbursement Coverage

Medicare caps on monthly pouch quantities and recent HCPCS code adjustments increase provider paperwork and may delay beneficiary access to upgraded appliances. Private insurers in the United States impose variable prior-authorization thresholds or coinsurance levels, prompting some patients to stretch wear-time at the expense of skin health. Policy divergence across European payers magnifies disparity; for example, a regional Medicaid program in the southern United States now requires explicit medical-necessity proof for accessories such as barrier rings, whereas a neighboring state imposes no copayment but limits closed-end pouches. In Japan, toughened cost-containment rules cut reimbursement lists for imported devices, urging suppliers to justify incremental performance benefits with real-world evidence. Such hurdles temper short-term uptake of premium two-piece systems in the Ostomy drainage bags market until coverage clarity improves.

Other drivers and restraints analyzed in the detailed report include:

- Rising Colorectal and Bladder Cancer Cases

- Emergence of Smart-Sensor Ostomy Bags

- High Cost of Advanced Multi-Layer Barrier Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Colostomy bags maintained 45.85% revenue leadership in 2024 due to steady colorectal cancer volumes and high prevalence of diverticular disease. This dominant position supplies a reliable baseline for the Ostomy drainage bags market, especially in North America and Western Europe where permanent stomas remain common. Temporary diversion patterns from low-anterior resection continue to shape product roadmaps toward softer plates and low-profile flanges that improve discretion during social activity. In parallel, ileostomy bags register the briskest 4.91% CAGR through 2030, supported by the climbing burden of inflammatory bowel disease among adults under 50. Surgeons favor loop ileostomy to protect anastomoses, a choice that drives higher pouch change frequency and thus raises per-patient consumption inside the Ostomy drainage bags market size.

The short fluidic output of ileostomies spurs demand for high-capacity drainable options with lockable tap valves, while colostomy users prioritize odor barriers and filter reliability. R&D teams now integrate gas-selective membranes into both segments, aiming to curb ballooning without compromising discretion. On the urinary side, cutaneous ureterostomy gains traction for frail patients, and this procedure raises the need for specialized anti-reflux urostomy pouches. Continent diversions such as K-pouch present a niche but clinically significant area where internal reservoirs still require external night drainage, opening another micro-specialty for innovators within the Ostomy drainage bags market.

One-piece appliances captured 60.12% revenue in 2024 as their all-in-one design appeals to elderly or dexterity-limited users. These systems reduce handling steps and minimize potential misalignment between barrier and pouch. Yet two-piece systems are advancing at a 5.12% CAGR because modularity resonates with active users who value the freedom to replace either component without disturbing the other. Clinical audits reveal that more than 90% of moldable two-piece users report easier application after structured nurse training, translating into lower peristomal skin complications and longer wear-time. Lock-and-roll closures as well as audible coupling clicks further elevate user confidence and fuel brand loyalty across the Ostomy drainage bags market.

Manufacturing investments in injection-molded coupling rings bring down cost differentials, narrowing the historic price gap between formats. This shift, combined with payers' growing focus on total-care cost rather than unit price, underpins the two-piece momentum. In the premium tier, connected sensor wafers currently launch only for flat plates, yet roadmaps indicate curved and convex versions will follow, allowing two-piece configurations to capture the earliest volumes in the smart-device niche of the Ostomy drainage bags market size.

The Report Covers Urinary Drainage Bags Market Trends & Growth and the Market is Segmented by Type (Colostomy Bags, Ileostomy Bags, Urostomy Bags, and Other Ostomy Types), End User (Hospitals, Home Care Setups, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Provides the Value (in USD Million) for the Above-Mentioned Segments.

Geography Analysis

North America owned 41.95% of global revenue in 2024 because of its advanced surgical infrastructure, broad insurance coverage and early adoption of sensor-enabled devices. The United States remains the region's anchor, supported by more than 2 million projected new cancer cases during 2025 and strong physician loyalty to premium moldable wafers. Canada contributes steady volume growth through nationwide stoma-nurse networks that help keep complication rates low and justify higher average selling prices. In Mexico, expanding private hospital chains now mirror U.S. formularies, fostering fresh demand for two-piece appliances with lock-in coupling systems and filter upgrades.

Europe generates balanced growth as universal health schemes favor cost-effectiveness while still endorsing products that demonstrate tangible skin-health benefits. Germany and France promote specialist stoma clinics that encourage best-practice adoption, while Italy and Spain remain price-focused but increasingly receptive to connected leak-alert add-ons. Environmental legislation is a prominent agenda item; the upcoming EU Packaging and Packaging Waste Regulation requires full pouch packaging recyclability by 2035 for healthcare, urging suppliers to expedite thinner multilayer film research. Such regulation shapes product design decisions and could expand the Ostomy drainage bags market share of companies with early compliant portfolios.

Asia-Pacific is the most dynamic territory, clocking a 5.81% CAGR to 2030 as healthcare infrastructure investment accelerates. China's ongoing hospital construction boom and widening social-insurance coverage allow international brands to distribute premium two-piece and smart-sensor models beyond top-tier cities. ConvaTec reported double-digit ostomy sales growth in China during 2024, underscoring local appetite for higher-performance solutions. India shows fast-rising IBD incidence that stretches stoma nursing resources, but the private-hospital segment is increasingly sourcing high-capacity drainable pouches to limit peristomal dermatitis. Japan's reimbursement cuts temper near-term price escalation, yet local clinicians maintain a preference for high-quality skin barriers, sustaining stable unit value. Australia, South Korea and select Southeast Asian economies extend regional momentum through aging populations and rising colorectal screening programs, together ensuring that the Ostomy drainage bags market remains on a multi-year growth trajectory.

- Alcare

- B. Braun

- Coloplast

- Convatec

- Hollister

- Flexicare Medical

- Marlen Manufacturing

- Pelcin Healthcare

- Salts Healthcare

- Torbot Group

- Welland Medical

- Prowess Care

- Goodhealth

- Oakmed Healthcare

- 3M

- Genairex Inc.

- Cymed Ostomy Co.

- Nu-Hope Laboratories

- Jiangsu Steadlive Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing incidence of IBD & Crohn's disease

- 4.2.2 Rapidly growing aging population

- 4.2.3 Rising colorectal & bladder cancer cases

- 4.2.4 Emergence of smart-sensor ostomy bags

- 4.2.5 Rapid expansion of direct-to-patient home-delivery subscription

- 4.2.6 Expansion of home-delivery supply subscription models

- 4.3 Market Restraints

- 4.3.1 Unstructured or shrinking reimbursement coverage

- 4.3.2 High cost of advanced multi-layer barrier materials

- 4.3.3 Environmental disposal restrictions on single-use plastics

- 4.3.4 Supply-chain vulnerability for medical-grade resins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Type

- 5.1.1 Colostomy Bags

- 5.1.2 Ileostomy Bags

- 5.1.3 Urostomy Bags

- 5.1.4 Continent Ileostomy & Urostomy Bags

- 5.2 By System Type

- 5.2.1 One-piece Bags

- 5.2.2 Two-piece Bags

- 5.3 By Usability

- 5.3.1 Drainable

- 5.3.2 Closed-end

- 5.4 By End User

- 5.4.1 Home-care Settings

- 5.4.2 Hospitals

- 5.4.3 Ambulatory Surgical Centers

- 5.5 By Distribution Channel

- 5.5.1 Direct Tender

- 5.5.2 Retail & E-commerce

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alcare Co. Ltd

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Coloplast A/S

- 6.3.4 ConvaTec Group Plc

- 6.3.5 Hollister Incorporated

- 6.3.6 Flexicare Medical Ltd

- 6.3.7 Marlen Manufacturing & Development

- 6.3.8 Pelcin Healthcare Ltd

- 6.3.9 Salts Healthcare Ltd

- 6.3.10 Torbot Group Inc.

- 6.3.11 Welland Medical Ltd

- 6.3.12 Prowess Care

- 6.3.13 Goodhealth Inc.

- 6.3.14 Oakmed Healthcare

- 6.3.15 3M Company

- 6.3.16 Genairex Inc.

- 6.3.17 Cymed Ostomy Co.

- 6.3.18 Nu-Hope Laboratories

- 6.3.19 Jiangsu Steadlive Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment