PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836449

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836449

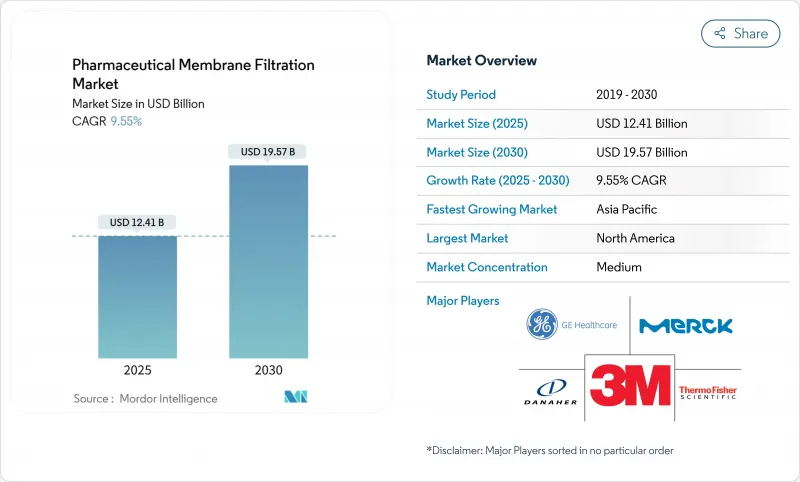

Pharmaceutical Membrane Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Pharmaceutical Membrane Filtration Market size is estimated at USD 12.41 billion in 2025, and is expected to reach USD 19.57 billion by 2030, at a CAGR of 9.55% during the forecast period (2025-2030).

Demand stems from the surge in biologics, gene therapies, and vaccine programs that require sterile, high-performance filters. The sector also benefits from regulatory pressure to prove viral clearance and from single-use systems that heighten production agility while curbing cross-contamination. Investments in nanofiltration, continuous processing, and real-time analytics further lift adoption, especially for virus removal, protein concentration, and water-for-injection operations. North America retains a leading position thanks to an entrenched bioprocessing base and clear guidance from the FDA, while Asia-Pacific gains momentum on the back of large-scale capacity additions and biotech incentives.

Global Pharmaceutical Membrane Filtration Market Trends and Insights

Increasing Adoption of Single-Use Technologies

Single-use filtration assemblies shorten change-over times by up to 50% and remove cleaning validation, making them a central pillar of modern biologics facilities. Compatibility with hollow-fiber tangential-flow designs lets producers retrofit legacy lines quickly. Flexible bag-based systems permit parallel campaigns for personalized therapies, while built-in sensors transmit critical quality data that satisfy FDA expectations for continuous monitoring. Cost advantages rise as utilities and labor shrink, and waste volumes decline thanks to lighter construction materials. As gene therapy volumes scale, single-use cartridges rated to >99.999% endotoxin removal enable rapid batch turnaround without risking cross-product carryover. The model aligns with pandemic-preparedness strategies that require fast site deployment and surge capacity.

Expansion of Biologics & Gene Therapy Pipelines

The global biologics pipeline surpasses 10,000 active programs, each requiring robust virus filtration that meets >6 log10 reduction mandates. Plasmid DNA and viral vectors impose high-viscosity loads that spur demand for membranes with optimized pore geometry to avoid shear-induced degradation.Asahi Kasei's Planova FG1 delivers seven-fold higher flux, cutting process time without compromising retention. Updated Q5A(R2) guidance promotes risk-based validation, encouraging application-specific filter development that supports rapid commercialization. The trend extends to mRNA vaccines, where clarification and sterilization must proceed under low binding conditions to protect fragile lipid nanoparticles.

High Capital Investment

Commercial-scale filtration suites cost upward of USD 10 million once skids, analytics, and validation are included, a hurdle for small firms and CDMOs. Integration of PAT sensors raises spending further because data historians and cybersecurity layers must be certified. Emerging-market manufacturers often rely on subsidies or partnerships to secure funding, and currency fluctuations can erode budgets. Thermo Fisher's USD 4.1 billion Solventum purchase shows the size of bets required to stay competitive in purification technology. Multinational companies must duplicate test protocols across regions, swelling capital tied up in duplicate equipment.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Regulatory Requirements

- Advancements in Nanofiltration Technology

- Membrane Fouling Issues & Reduced Lifecycle

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PES accounted for 32.84% of the pharmaceutical membrane filtration market in 2024, favored for high chemical resistance and low protein binding. Its hydrophilic nature supports 211 mL/min flow rates with protein adsorption below 1%, enabling consistent yields in mAb purification. Surface sulfonation and PEG grafting deepen hydrophilicity, stretch lifespan, and limit fouling.

PVDF is projected to grow at 10.01% CAGR despite PFAS scrutiny, owing to its low extractables and suitability for final fill lines. Regulatory uncertainty encourages suppliers to devise PFAS-free variants, but users value PVDF's thermal stability for steam-in-place cycles. Mixed cellulose ester, nylon, and polypropylene membranes satisfy niche lab or cost-sensitive tasks where extreme robustness is not essential. Comparative studies find PES retains permeability under high solids loads while PVDF excels in low-binding sterile filtration. Manufacturers target ultraclean grades that meet ever tighter leachables limits, preserving product purity throughout storage.

Microfiltration held 44.32% revenue share in 2024 due to entrenched use for cell harvesting and bioburden reduction. Resistance-in-series models allow accurate scale-up, ensuring pilot data translate to manufacturing. Continuous microfiltration combined with alternating tangential flow lifts harvest titers for intensified fed-batch cultures. Nanofiltration is set to rise at 12.95% CAGR on the back of vaccine and gene therapy pipelines demanding virus removal under high flux.

Two-dimensional material coatings raise water permeability without sacrificing 20 nm pore exclusion, facilitating >6 log10 virus clearance. Scale-down rigs help define optimal pH and conductivity windows, driving 900% throughput gains when parameters are tuned. Ultrafiltration remains vital for buffer exchange and protein concentration, whereas reverse osmosis handles water treatment for injection systems.

The Report Covers Pharmaceutical Membrane Filtration Market is Segmented by Material (Polyethersulfone, Polyvinylidene Difluoride, and More), Technique (Microfiltration, and More), Process Stage (Final Product Sterile-Filtration, and More), Scale (Laboratory, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 36.55% share of the pharmaceutical membrane filtration market in 2024, powered by a dense network of biologics plants and an FDA that endorses advanced manufacturing with clear guidance. Federal incentives for pandemic preparedness sustain spending on high-capacity single-use systems and continuous lines. Europe follows closely, driven by Annex 1 revisions that compel producers to adopt PUPSIT and automated integrity checks. Firms invest in virus filters and data-rich skids to navigate stringent audit expectations.

Asia-Pacific is set to grow at 11.67% CAGR through 2030 as governments pour funds into biotech hubs. Cytiva's USD 150 million Korean site and MilliporeSigma's EUR 300 million plant in Daejeon signal the region's ascent, offering local supply of sterile filters and single-use kits that shorten logistics chains. China and India increase GMP adherence, with close to 90% of Chinese and 100% of Indian biomanagers targeting global market entry. Latin America and the Middle East make incremental progress, led by Brazil and Saudi Arabia, which court CDMOs to diversify their economies. Harmonization of ICH guidelines eases technology transfer, enabling global firms to deploy identical filtration trains across multiple continents.

- 3M

- Danaher

- Merck

- Sartorius

- Thermo Fisher Scientific

- Parker Hannifin

- Repligen

- GEA Group

- Graver Technologies

- GE Healthcare

- Meissner Filtration

- Alfa Laval

- Cobetter Filtration

- Amazon Filters

- Porvair Filtration Group

- Novasep

- Donaldson Company

- Asahi Kasei

- Tami Industries

- Cole-Parmer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Single-Use Technologies

- 4.2.2 Expansion of Biologics & Gene Therapy Pipelines

- 4.2.3 Stringent Regulatory Requirements

- 4.2.4 Advancements in Nanofiltration Technology

- 4.2.5 Rising R&D Investments

- 4.2.6 Expanding Pharmaceutical Manufacturing in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Capital Investment

- 4.3.2 Membrane Fouling Issues & Reduced Lifecycle

- 4.3.3 Complexity in Integration

- 4.3.4 Limited Awareness in Developing Regions

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Material

- 5.1.1 Polyethersulfone (PES)

- 5.1.2 Polyvinylidene Difluoride (PVDF)

- 5.1.3 Mixed Cellulose Ester & Cellulose Acetate (MCE & CA)

- 5.1.4 Nylon

- 5.1.5 Polypropylene & Others

- 5.2 By Technique

- 5.2.1 Microfiltration

- 5.2.2 Ultrafiltration

- 5.2.3 Nanofiltration

- 5.2.4 Reverse-Osmosis & Others

- 5.3 By Process Stage

- 5.3.1 Final Product Sterile-filtration

- 5.3.2 Bulk Drug Substance Clarification

- 5.3.3 Cell Separation & Harvesting

- 5.3.4 Water & Utility Filtration

- 5.3.5 Air/Gas Filtration

- 5.4 By Scale

- 5.4.1 Laboratory

- 5.4.2 Pilot

- 5.4.3 Commercial Production

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Danaher

- 6.3.3 Merck KGaA

- 6.3.4 Sartorius Stedim Biotech

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Parker Hannifin

- 6.3.7 Repligen Corporation

- 6.3.8 GEA Group

- 6.3.9 Graver Technologies

- 6.3.10 GE Healthcare

- 6.3.11 Meissner Filtration

- 6.3.12 Alfa Laval

- 6.3.13 Cobetter Filtration

- 6.3.14 Amazon Filters

- 6.3.15 Porvair Filtration Group

- 6.3.16 Novasep

- 6.3.17 Donaldson Company

- 6.3.18 Asahi Kasei

- 6.3.19 Tami Industries

- 6.3.20 Cole-Parmer

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment