PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836493

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836493

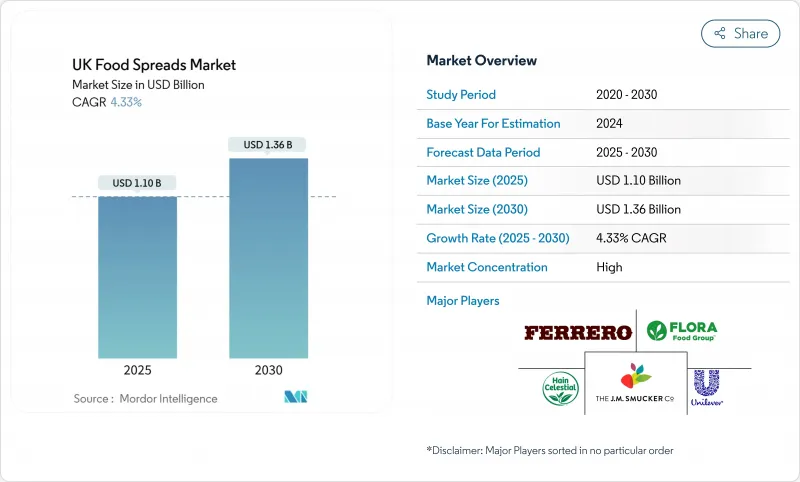

UK Food Spreads - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United Kingdom Food Spreads Market stands at USD 1.10 billion in 2025 and is projected to reach USD 1.36 billion by 2030, growing at a CAGR of 4.33% during the forecast period.

This growth trajectory reflects the market's resilience despite economic pressures, as consumers increasingly view food spreads as affordable indulgences that offer versatility across multiple consumption occasions. The market's expansion is being propelled by the dual forces of premiumization and health consciousness, with consumers willing to pay more for products that deliver on taste, quality, and nutritional benefits. The growing breakfast culture in the UK, combined with continuous innovation in flavors and premium ingredients, is reshaping the food spreads landscape. Manufacturers are responding to consumer demands by introducing new flavor variants and incorporating high-quality ingredients, while the increasing popularity of breakfast occasions provides multiple opportunities for spread consumption throughout the day. As the market continues to evolve, the combination of innovative product development and changing consumer preferences positions for sustained growth and diversification in the coming years.

UK Food Spreads Market Trends and Insights

Growing popularity of breakfast culture increases spread consumption

The resurgence of breakfast as a critical meal is fundamentally reshaping the UK food landscape. This trend extends beyond traditional toast applications, as consumers incorporate spreads into breakfast bowls, smoothies, and baked goods. This perspective is particularly evident among younger demographics who consider morning nutrition fundamental to their wellness routines, creating opportunities for spreads with specific functional benefits such as protein enhancement or energy provision. The breakfast trend's sustainability is reinforced by home-based consumption patterns established during pandemic lockdowns, which have continued even as work routines normalize. Manufacturers are responding to this shift by developing innovative spread formulations that cater to specific dietary preferences, including plant-based and reduced-sugar options. Additionally, the growing emphasis on breakfast has led to increased retail shelf space dedicated to morning-focused spreads, reflecting the market's adaptation to evolving consumer preferences.

Busy lifestyles increase the preference for convenient and versatile food options

The increasing employment rates and busy lifestyles are reshaping consumer food preferences, particularly in favor of convenient and versatile options. This time compression in modern households has elevated the strategic importance of versatile food products, particularly food spreads, which serve multiple culinary functions. The market is adapting to these changing consumer needs by expanding beyond traditional bread applications, with food spreads gaining popularity as cooking ingredients, dessert components, and snack complements. The food spreads market has evolved to meet consumer demands through innovative product formulations that offer enhanced functionality and convenience, including squeezable packaging and portion-controlled formats. According to UK Labour Market Statistics, the employment rate for people aged 16-64 reached 75.1% in February to April 2025, with 34.01 million people aged 16 and above in employment, marking an increase of approximately 667,000 over the previous year . Additionally, the integration of food spreads into meal preparation has become more prevalent, with consumers utilizing these products as quick flavor enhancers and nutritional supplements in various recipes.

High competition from private-label brands pressures pricing

Economic pressures are accelerating the shift toward private label products in food spreads, creating margin compression for branded manufacturers who must demonstrate distinctive value propositions to justify premium pricing. This trend is particularly pronounced in staple segments like fruit spreads, where product differentiation is challenging and price sensitivity is high. The private label threat is intensifying as retailers enhance their own-brand offerings with premium cues, clean labels, and sustainability credentials that previously distinguished national brands. The regulatory environment is further disrupting the market, driving reformulation efforts across both branded and private label segments as manufacturers recalibrate their value propositions. These market dynamics pose significant challenges for manufacturers, potentially limiting their ability to maintain profit margins and invest in product innovation. The competitive landscape has become increasingly complex as manufacturers face pressure to innovate while simultaneously managing cost structures and maintaining market share. Additionally, changing consumer preferences toward healthier and more sustainable options have compelled both national brands and private labels to adapt their product portfolios, further straining operational resources and development capabilities.

Other drivers and restraints analyzed in the detailed report include:

- Innovation in flavors and premium ingredients attracts new consumers

- Expansion of vegan and organic product lines drives market growth

- Health concerns over sugar and fat content reduce traditional spread usage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fruit-based spreads hold a dominant 38.51% market share in 2024, supported by traditional breakfast consumption patterns and their natural ingredient perception. However, the segment faces volume decline as consumers become increasingly conscious of sugar content in traditional jams. This trend is particularly evident in developed markets where health-conscious consumers are actively seeking alternatives with reduced sugar content. Manufacturers like B Healthy Limited, Locco are responding by expanding their product portfolio in low-sugar and sugar-free variants, incorporating natural sweeteners and fruit concentrates.

Nut and seed-based spreads are experiencing rapid growth, with a projected CAGR of 6.81% from 2025-2030. This growth stems from their high protein content and alignment with plant-based diets. Products featuring natural, minimally processed ingredients have gained substantial market acceptance. The increasing adoption of these spreads in snacking applications has further accelerated their market penetration. The category has witnessed significant innovation in flavor combinations and ingredient profiles, including the introduction of specialty nuts and superseeds. The versatility of these spreads, from breakfast applications to recipe ingredients, has contributed to their expanding consumer base across different demographic segments.

The conventional segment holds a 72.31% market share in 2024, driven by established brands, extensive distribution networks, and competitive pricing. The segment maintains its dominant position by delivering consistent quality and familiar taste profiles that align with traditional consumer preferences. The conventional segment's market leadership is further reinforced by its strong brand recognition and consumer trust built over decades. These products benefit from economies of scale in production and established relationships with retailers, enabling manufacturers to maintain competitive price points. Additionally, conventional spreads continue to dominate household penetration rates due to their widespread availability across various retail channels and their role as pantry staples.

The organic food spreads segment is projected to grow at a CAGR of 9.84% during 2025-2030, exceeding the overall market growth rate. This expansion stems from increasing consumer preference for natural, clean-label products and environmentally sustainable options. The growth trajectory is supported by rising health consciousness and increasing disposable income among consumers. The segment's growth is further accelerated by expanding retail shelf space dedicated to organic products and increasing investment in organic farming practices by manufacturers. Moreover, the introduction of innovative organic spread variants and flavors, coupled with enhanced marketing efforts highlighting their health benefits, continues to attract new consumer segments.

The United Kingdom Food Spreads Market is Segmented by Product Type (Honey, Chocolate-Based Spread, Fruit-Based Spread, and More); Nature (Conventional and Organic), Packaging Type (Jars, Tubs, Sachets/Pouches and Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and Others). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Unilever PLC

- Ferrero International SA

- Flora Food Company

- The J.M. Smucker Company

- The Hain Celestial Group

- Conagra Brands, Inc

- Lindt & Sprungli AG

- Premier Foods plc

- Lotus Bakeries

- Pip & Nut Ltd

- Intersnack Group GmbH & Co. KG

- SHS Group

- ManiLife Ltd

- Hilltop Honey Ltd

- Valeo Foods

- Stute Foods Ltd

- Andros Group

- The Kraft Heinz Company

- St. Dalfour SAS

- F. Duerr & Sons Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing popularity of breakfast culture increases spread consumption.

- 4.2.2 Busy lifestyles increase the preference for convenient and versatile food options

- 4.2.3 Innovation in flavors and premium ingredients attracts new consumers.

- 4.2.4 Expansion of vegan and organic product lines drives market growth.

- 4.2.5 Convenience packaging formats encourage on-the-go usage.

- 4.2.6 Strong retail infrastructure supports wide product availability.

- 4.3 Market Restraints

- 4.3.1 High competition from private-label brands pressures pricing.

- 4.3.2 Health concerns over sugar and fat content reduce traditional spread usage.

- 4.3.3 Increasing allergy awareness limits nut-based spread consumption.

- 4.3.4 Regulatory constraints on labeling and health claims add complexity.

- 4.4 Regulatory Outlook

- 4.5 Technology Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Honey

- 5.1.2 Chocolate-based Spreads

- 5.1.3 Fruit-based Spreads

- 5.1.4 Nut and Seed-based Spreads

- 5.1.5 Dairy and Cheese Spreads

- 5.1.6 Other Product Types

- 5.2 By Nature

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 By Packaging Type

- 5.3.1 Jars

- 5.3.2 Tubs

- 5.3.3 Sachets/Pouches

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Unilever PLC

- 6.4.2 Ferrero International SA

- 6.4.3 Flora Food Company

- 6.4.4 The J.M. Smucker Company

- 6.4.5 The Hain Celestial Group

- 6.4.6 Conagra Brands, Inc

- 6.4.7 Lindt & Sprungli AG

- 6.4.8 Premier Foods plc

- 6.4.9 Lotus Bakeries

- 6.4.10 Pip & Nut Ltd

- 6.4.11 Intersnack Group GmbH & Co. KG

- 6.4.12 SHS Group

- 6.4.13 ManiLife Ltd

- 6.4.14 Hilltop Honey Ltd

- 6.4.15 Valeo Foods

- 6.4.16 Stute Foods Ltd

- 6.4.17 Andros Group

- 6.4.18 The Kraft Heinz Company

- 6.4.19 St. Dalfour SAS

- 6.4.20 F. Duerr & Sons Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK