PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836503

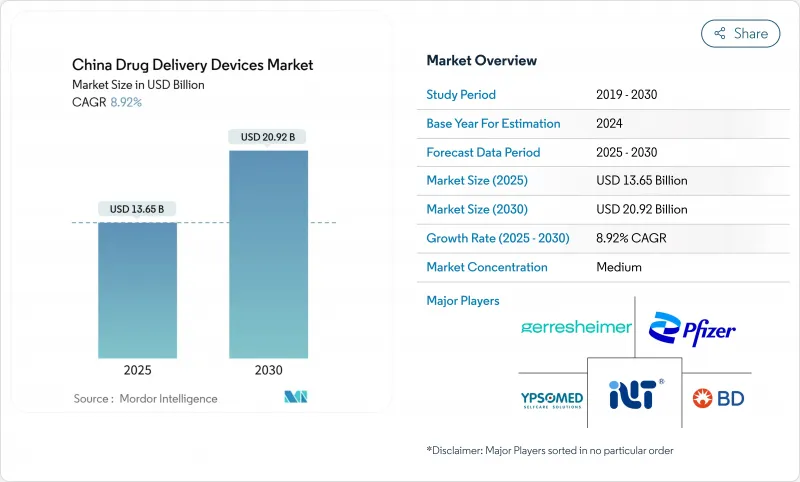

China Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The China drug delivery devices market is valued at USD 13.65 billion in 2025 and is forecast to reach USD 20.92 billion by 2030, registering an 8.92% CAGR over the period.

Growth is powered by a rapidly aging population, 28% of citizens will be over 60 by 2040, along with rising chronic-disease prevalence, sweeping reimbursement reforms, and a wave of biologics that demand precision delivery. Volume-Based Procurement (VBP) has lowered average drug prices by 53%, which is steering hospitals toward locally made devices while encouraging global suppliers to localize production. Persistent air-quality challenges in tier-1 cities are sustaining demand for inhalation platforms even as respiratory conditions remain a public-health priority. At the same time, 5G connectivity and AI-enabled adherence tools are opening fresh opportunities for smart, home-use systems in rural regions. Competitive pressure is intensifying as domestic contract development and manufacturing organizations (CDMOs) scale up, compressing costs for both injectables and emerging implantables.

China Drug Delivery Devices Market Trends and Insights

Rising Burden of Chronic Diseases

China now houses 22% of the global diabetes population, and cardiovascular illness affects around 330 million citizens, driving hospitals and payers toward precise, home-use devices that can curb readmissions while enabling self-management. The "Healthy China 2030" blueprint backs this shift, prioritizing chronic-disease control and broadening access to community-level services. Aging-related disability also lifts demand for long-acting implantables that reduce caregiver workload without compromising therapeutic outcomes. Devices that automate dosing or use remote monitoring are therefore gaining traction among provincial health authorities looking to shrink long-term care costs. Hospital groups in Shanghai and Guangzhou have already introduced bundled packages that pair insulin analogues with connected pens, demonstrating early commercial success.

Advances in Biologics Necessitating Sophisticated Devices

Chinese biotech funding remains buoyant-47 cell- and gene-therapy firms raised new capital in 1H 2024-pushing developers to seek materials and formats that protect fragile payloads. AI-driven start-ups such as METiS Pharmaceuticals are refining lipid nanoparticles for mRNA, which in turn boosts orders for temperature-controlled syringes and autoinjectors. Regulators have responded with guidelines that mandate post-marketing stability data, adding urgency for delivery innovations that maintain bioavailability from plant to patient.Oncology remains a focal point: personalized dosing regimens require variable-volume cartridges compatible with in-clinic compounding workflows. As a result, domestic syringe makers in Jiangsu have expanded clean-room capacity by double digits to serve local biopharma clients.

High R&D and Approval Costs

Maider Medical's revenue slid 42.77% in 2024 even as it kept R&D at 14.70% of sales, underscoring cost pressures on smaller firms. Contec Medical Systems faced a similar squeeze after a 35.76% top-line drop while sustaining RMB 10.52 million in research outlays. Enhanced NMPA testing requirements heighten compliance spend, creating a hurdles-to-entry effect that favors capital-rich incumbents. BeiGene's cumulative loss of RMB 62.67 billion illustrates how even leading innovators absorb steep investment to meet global standards.

Other drivers and restraints analyzed in the detailed report include:

- Government Health-Insurance Expansion

- Domestic CDMO Scale-Up Lowering Device Costs

- Centralized VBP Price Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Injectable platforms retained a 42.34% share in 2024, anchoring the China drug delivery devices market as hospitals prefer proven parenteral formats for biologics and vaccines. Implantables post the fastest 11.33% CAGR, benefiting from materials science advances that support weeks-long release profiles. Inhalers continue to thrive in polluted metropolitan zones, while infusion pumps rise steadily on the back of ICU modernization projects. Transdermal patches win favor among seniors seeking pain relief without oral side effects, and ocular inserts gain momentum as diabetic retinopathy rates climb. Nasal and buccal formats, though niche, attract pediatric demand where needle avoidance is critical.

Injectables are also the first choice for home-based biologic regimens, which tightens linkages between prefilled syringe makers and tele-pharma platforms. Meanwhile, implantables ride on gene-therapy momentum: start-ups in Shanghai are prototyping refillable micro-reservoirs to pair with autologous cell payloads. These trends reinforce the China drug delivery devices market size leadership of injectable formats, yet implantables are closing the gap as payers recognize reduced dosing frequency benefits.

With 48.65% of 2024 revenue, injectables remain the backbone of therapeutic delivery owing to unmatched bioavailability and multi-therapeutic flexibility. Ocular routes, however, show a 10.78% CAGR through 2030 as sustained-release implants cut injection frequency for macular degeneration. Inhalation stands firm because pollution-driven chronic obstructive pulmonary disease (COPD) cases remain high in urban clusters. Transdermal lines grow in cardiovascular care, aided by skin-friendly adhesives that enable week-long nitroglycerin delivery. Oral mucosal and nasal routes gain share for emergency and pediatric uses where rapid onset is pivotal.

Regulators now encourage patient-reported outcomes in ocular trials, fast-tracking approvals for micro-dose injectors that limit systemic exposure. Local inhaler makers add smartphone pairing to monitor technique, meeting NHSA evidence thresholds for reimbursement. As a result, the China drug delivery devices market share of non-injectable routes is set to widen, although injectables keep pole position for biologics and vaccines.

The China Drug Delivery Devices Market Report is Segmented by Device Type (Injectable Delivery Devices, Inhalation Delivery Devices, Infusion Pumps, and More), Route of Administration (Injectable, Inhalational, Transdermal, and More), Therapeutic Application (Cardiovascular, Oncology, Diabetes, and More), and Sales Channel (Hospitals, Offline Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beckton Dickinson

- Gerresheimer

- Pfizer

- Teleflex Medical

- Teva Pharmaceutical Industries

- Organon

- Novartis

- GlaxoSmithKline

- Baxter

- Ypsomed

- Kindly Medical Instruments Co., Ltd.

- Jiangsu Delfu Medical Device Co., Ltd.

- MicroPort

- Shanghai Pukun Medical Co., Ltd.

- SHL Medical AG

- Tianjin Pharmaco Medical Devices Co., Ltd.

- Nemera

- Owen Mumford

- Elcam Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases

- 4.2.2 Advances in Biologics Necessitating Sophisticated Devices

- 4.2.3 Government Health-Insurance Expansion

- 4.2.4 Urban Air-Quality Decline Boosting Inhalation Demand

- 4.2.5 Domestic CDMO Scale-up Lowering Device Costs

- 4.2.6 5G-enabled Smart Connectivity for Adherence Monitoring

- 4.3 Market Restraints

- 4.3.1 High R&D and Approval Costs

- 4.3.2 Centralized Volume-based Procurement (VBP) Price Pressure

- 4.3.3 Cold-chain Gaps in Lower-tier Cities

- 4.3.4 Fragmented IP Landscape Delaying Innovation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Injectable Delivery Devices

- 5.1.2 Inhalation Delivery Devices

- 5.1.3 Infusion Pumps

- 5.1.4 Transdermal Patches

- 5.1.5 Implantable Drug Delivery Systems

- 5.1.6 Ocular Inserts & Delivery Implants

- 5.1.7 Nasal & Buccal Delivery Devices

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Inhalation

- 5.2.3 Transdermal

- 5.2.4 Oral Mucosal (Buccal & Sublingual)

- 5.2.5 Ocular

- 5.2.6 Nasal

- 5.3 By Therapeutic Application

- 5.3.1 Cardiovascular

- 5.3.2 Oncology

- 5.3.3 Autoimmune Disorders

- 5.3.4 Pulmonary Diseases

- 5.3.5 Diabetes

- 5.3.6 Neurological Disorders

- 5.3.7 Other Applications

- 5.4 By Sales Channel

- 5.4.1 Hospitals

- 5.4.2 Offline Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Other Channels

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Gerresheimer AG

- 6.3.3 Pfizer Inc.

- 6.3.4 Teleflex Medical

- 6.3.5 Teva Pharmaceutical Industries Ltd.

- 6.3.6 Organon

- 6.3.7 Novartis AG

- 6.3.8 GSK plc

- 6.3.9 Baxter International Inc.

- 6.3.10 Ypsomed Holding AG

- 6.3.11 Kindly Medical Instruments Co., Ltd.

- 6.3.12 Jiangsu Delfu Medical Device Co., Ltd.

- 6.3.13 MicroPort Scientific Corporation

- 6.3.14 Shanghai Pukun Medical Co., Ltd.

- 6.3.15 SHL Medical AG

- 6.3.16 Tianjin Pharmaco Medical Devices Co., Ltd.

- 6.3.17 Nemera

- 6.3.18 Owen Mumford Ltd.

- 6.3.19 Elcam Medical

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment