PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836516

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836516

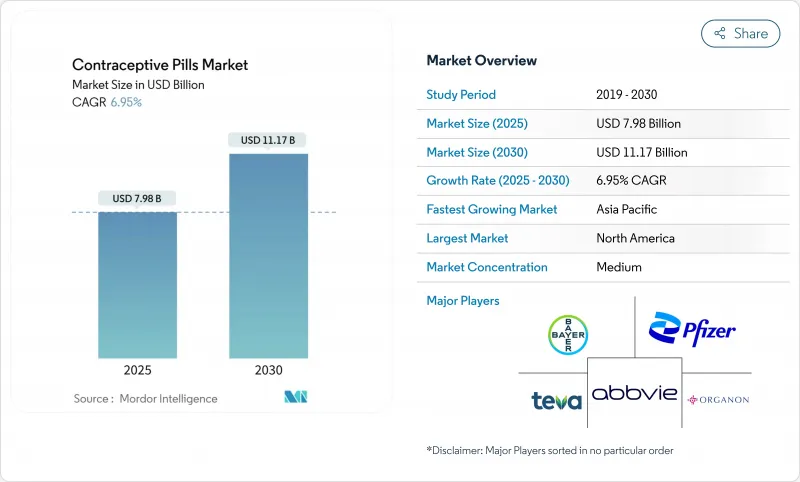

Contraceptive Pills - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The contraceptive pills market reached USD 7.98 billion in 2025 and is forecast to climb to USD 11.17 billion by 2030, advancing at a 6.95% CAGR.

The jump to over-the-counter availability in several countries, led by the United States Food and Drug Administration (FDA) approval of Perrigo's Opill, is rewriting traditional prescription-based growth paths. Softening price points for generics, expanding telehealth distribution, and rising demand for low-dose estrogen formulations are widening the user base while intensifying price competition. Strategic consolidation among originator companies and fast-moving direct-to-consumer (DTC) start-ups is creating a two-tier competitive field that rewards scale on one end and nimble digital execution on the other. Late-stage product pipelines center on progestin-only pills (POPs) and extended-cycle regimens that promise clinical differentiation without raising costs.

Global Contraceptive Pills Market Trends and Insights

Increasing demand for low-dose estrogen formulations

Cardiovascular safety signals identified in large cohort studies have pushed manufacturers toward minimal-dose estrogen products, halving thromboembolic risk without compromising efficacy.Prescription switches accelerated after FDA guidance on lowering estrogen exposure in hormonal contraceptives. Pharmaceutical pipelines now emphasize 10-20 µg ethinyl estradiol ranges, giving physicians clinical incentives to recommend lower-risk brands. Strong marketing around gentler side effect profiles broadens uptake among women over 35 and those with cardiovascular concerns, adding steady volume to the contraceptive pills market.

Government initiatives and policies for family planning and reproductive health

Mandates that require insurers to reimburse over-the-counter pills without copays are removing residual cost barriers in the United States. Parallel moves in Asia-Pacific to bundle oral contraceptives into universal coverage programs stretch demand into semi-urban clinics. Thirty U.S. states plus the District of Columbia authorize pharmacists to prescribe contraceptives, sidestepping appointment bottlenecks and lifting regional prescription fill rates. These policy levers compound in markets where fertility reduction remains a national objective, bolstering long-term unit sales.

Mounting litigation risk linked to hormone-related adverse events

Class-action suits tied to thrombotic events and newly flagged psychiatric outcomes continue to dent brand reputations, exemplified by thousands of Depo-Provera filings in U.S. courts. Escalating legal reserves weigh on budgets for marketing and innovation, tempering the growth slope of the contraceptive pills market.

Other drivers and restraints analyzed in the detailed report include:

- Shift toward tele-prescription and DTC platforms

- Delayed family planning and high rate of unintended pregnancies

- Emergence of long-acting reversible contraceptives (LARCs)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Combination formulations controlled 85.7% of the contraceptive pills market share in 2024, underpinned by favorable reimbursement histories and clinician familiarity. Yet progestin-only pills are expanding at a 7.97% CAGR that outstrips the overall contraceptive pills market. The July 2023 FDA clearance of OTC Opill, which reached shelves in March 2024, validated POP safety profiles for self-administration and emboldened copycat applications. Clinical data from a 2025 Danish cohort study linking combined estrogen exposure with doubled ischemic stroke risk is accelerating physician rotation toward estrogen-free options.

Pharmaceutical pipelines now target refined POP delivery-film-coated tablets, biodegradable implants, and vaginal rings-that mitigate breakthrough bleeding but maintain systemic neutrality. Originator companies are also filing for expanded indications, such as acne reduction, to offset narrowing combination margins. Taken together, these trends should lift the progestin-only slice of the contraceptive pills market size significantly by 2030.

The classic 28-day pack still captured 57.3% of the contraceptive pills market size in 2024, but extended/continuous schedules are on pace for an 9.23% CAGR, the quickest among all regimens. Women cite fewer bleeding episodes, lower cramp frequency, and better lifestyle fit as purchase motivators. Randomized trials demonstrate that 24/4 dosing lowers pregnancy incidence more effectively than 21/7 protocols while sustaining similar side-effect tolerability.

DTC platforms amplify awareness through personalized app reminders, nudging consumers to ask for extended cycles during virtual consults. Manufacturers are answering with flexible packs-four annual withdrawal bleeds-that encourage brand switching without raising manufacturing costs. Wider acceptance could push extended cycles toward a double-digit share of the contraceptive pills market by the decade's close.

Contraceptive Pills Market Report is Segmented by Hormone Type (Progestin-Only Pills and Combination Pills [Monophasic, Biphasic and More]), Dose Regimen (21- Day Cyle, 24- Day Cycle and More), Category (Generic and Branded), Distribution Channel(Hospital Pharmacies, Retail Pharmacies and More), Age Group (15 - 24 Years, 25 - 34 Years and More) and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 36.67% of the contraceptive pills market in 2024, catalyzed by progressive regulatory shifts and broad insurance coverage. The OTC launch of Opill at USD 19.99 has widened pharmacy-checkout access and chipped away at prescription gatekeeping. Yet, policy divergence is stark; states that enacted full abortion bans recorded a 4.1% drop in oral pill fills within a year, underscoring how legal climates modulate regional sales. The contraceptive pills market size is likely to keep expanding as more states empower pharmacists to dispense without a physician's note.

Asia-Pacific posts the fastest 8.85% CAGR for 2025-2030 as government-backed family-planning drives intersect rising female workforce participation. Urban India, Indonesia, and Vietnam headline volume growth, while rural pockets still battle supply gaps. Variations in contraceptive prevalence across demographics persist, but structural investments in public-sector distribution and mobile health units should narrow disparities.

Europe maintains a high baseline of contraceptive prevalence, yet safety-driven shifts toward low-dose estrogen and emerging POPs rekindle moderate value growth. Eastern European reimbursement reforms present fresh volume avenues, whereas Western Europe emphasizes differentiated formulations with minimal side effects.

The Middle East and Africa and South America together represent an under-penetrated frontier for the contraceptive pills industry. Urbanization and female-education gains support incremental adoption, but cultural resistance and logistics shortfalls still hinder uniform access. Funding partners such as UNFPA and USAID lifted contraceptive procurement spending to USD 237 million in FY 2023, paving the way for improved supply reliability clintonhealthaccess.

- Bayer

- Pfizer

- Organon

- Teva Pharmaceutical Industries

- Abbvie

- Johnson & Johnson

- Viatris

- Amneal Pharmaceuticals

- Aurobindo Pharma Ltd.

- Zydus Group

- Mayne Pharma Group Ltd.

- Lupin

- Cipla

- Perrigo (HRA Pharma)

- Sun Pharma Industries Ltd.

- Exeltis USA

- Gedeon Richter Plc.

- Glenmark Pharmaceuticals

- Piramal Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Low-Dose Estrogen Formulations

- 4.2.2 Government Initiatives and Policies for Family Progam and Reproductive Health

- 4.2.3 Shift Toward Tele-Prescription & Direct-to-Consumer Platforms

- 4.2.4 Delayed Family Planning and High Rate on Unintendent Pregnancies

- 4.2.5 Product Innovation & New Formulations

- 4.2.6 Over-the-Counter (OTC) Switch Approvals Expanding Retail Access

- 4.3 Market Restraints

- 4.3.1 Mounting Litigation Risk Linked to Hormone-Related Adverse Events

- 4.3.2 Emergence of Long-Acting Reversible Contraceptives

- 4.3.3 Challenges Associated with Product like Misconception, Misinformation, Adherance Issues etc.

- 4.3.4 Cultural and Religious Opposition in Few Parts of World

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Hormone Type

- 5.1.1 Progestin-Only Pills

- 5.1.2 Combination Pills

- 5.1.2.1 Monophasic

- 5.1.2.2 Biphasic

- 5.1.2.3 Triphasic

- 5.1.2.4 Other Combination Formulations

- 5.2 By Dosage Regimen

- 5.2.1 21-Day Cycle

- 5.2.2 24-Day Cycle

- 5.2.3 28-Day Cycle

- 5.2.4 Extended / Continuous Cycle

- 5.3 By Category

- 5.3.1 Generic

- 5.3.2 Branded

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Age Group

- 5.5.1 15 - 24 Years

- 5.5.2 25 -34 Years

- 5.5.3 35 - 44 Years

- 5.5.4 45 + Years

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Pfizer Inc.

- 6.4.3 Organon & Co.

- 6.4.4 Teva Pharmaceutical Industries Ltd.

- 6.4.5 AbbVie Inc. (Allergan)

- 6.4.6 Johnson & Johnson (Janssen)

- 6.4.7 Viatris Inc.

- 6.4.8 Amneal Pharmaceuticals LLC

- 6.4.9 Aurobindo Pharma Ltd.

- 6.4.10 Zydus Cadila

- 6.4.11 Mayne Pharma Group Ltd.

- 6.4.12 Lupin Ltd.

- 6.4.13 Cipla Ltd.

- 6.4.14 Perrigo (HRA Pharma)

- 6.4.15 Sun Pharma Industries Ltd.

- 6.4.16 Exeltis USA Inc.

- 6.4.17 Gedeon Richter Plc.

- 6.4.18 Glenmark Pharmaceuticals

- 6.4.19 Piramal Healthcare

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment