PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836568

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836568

Automotive Fuel Delivery System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

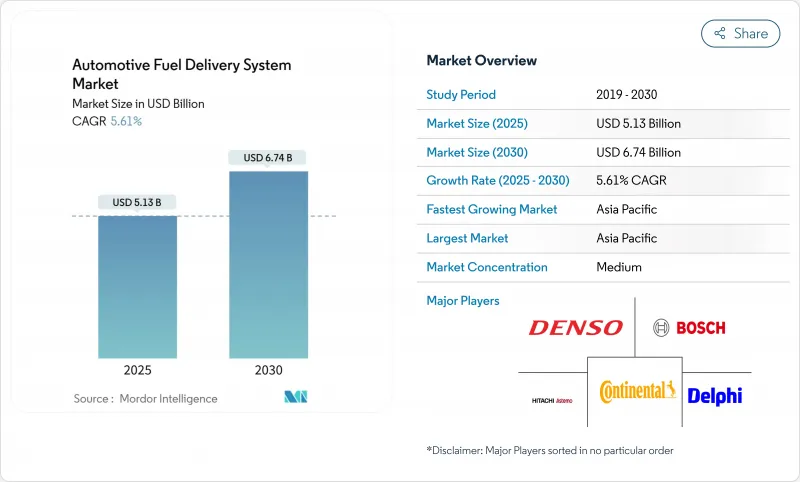

The automotive fuel delivery system market size stood at USD 5.13 billion in 2025 and is forecast to reach USD 6.74 billion by 2030, advancing at a 5.61% CAGR.

The growth trajectory reflects the sector's ability to meet tougher emission limits while staying relevant in an era of rising electrification. Euro 7 rules that apply from July 2025 and the EPA Phase 3 standards, effective 2027, are pushing automakers toward high-precision injection modules and corrosion-resistant lines, sustaining capital expenditure on modern internal-combustion (ICE) architectures. Suppliers adopt "technology-neutral" portfolios that keep ICE value streams alive yet prepare for plug-in and fuel-cell demand shifts, limiting downside risk for the automotive fuel delivery system market.

Global Automotive Fuel Delivery System Market Trends and Insights

Stringent Emission Norms Driving Advanced Fuel-Delivery Modules

Euro 7 tightens particulate and NOx thresholds for all light-duty engines from November 2026, while EPA Phase 3 slashes NOx to 35 mg/hp-hr for heavy trucks in 2027 . Automakers are therefore standardizing high-pressure pumps and gasoline particulate filters across global platforms. Durability requirements rise to 160,000 km, pushing suppliers to develop long-life injectors and corrosion-proof rails, factors that underpin the automotive fuel delivery system market through 2030.

Rising Global Vehicle Production and Parc Rejuvenation

Light-vehicle output rebounded in 2025, and replacement cycles shortened as average fleet age passed 12 years in Europe, reinforcing component demand for the automotive fuel delivery system market. Vehicle-makers localize plants in India, Indonesia, and Mexico, creating regional sourcing pull for tier-1 suppliers. Fleet operators refresh hardware to meet fuel-economy benchmarks, prolonging ICE relevance despite EV penetration.

Rapid Growth of Electric Vehicles Reducing ICE Share

China and California are accelerating toward full zero-emission mandates by 2035. EV momentum is cutting ICE-linked profit pools by an anticipated 50% this decade. Fuel pumps and injectors are absent from battery platforms, creating long-run headwinds, yet regional differences keep the automotive fuel delivery system market relevant in heavy-duty, rural, and developing-country segments.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Gasoline Direct-Injection Engines in Passenger Cars

- Increasing Sales of Light Commercial Vehicles

- Volatility in Raw-Material Prices for Fuel-System Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel pumps generated 37.81% revenue of the automotive fuel delivery system market in 2024 and remain indispensable across all engine sizes, anchoring the automotive fuel delivery system market. Their ubiquity provides steady volumes even as electrification advances. Accelerating fastest, injectors will rise at 7.14% CAGR to 2030 on the back of 2,200 psi GDI requirements, pushing "smart" tip designs and stainless-steel rails for ethanol blends.

Component upgrades now emphasize on-board diagnostics, remote pressure sensing, and over-the-air firmware that cuts unplanned downtime. Biofuel growth lifts demand for corrosion-resistant lines and filters, while vapor-recovery valves and tank-mounted sensors add incremental electronics value. Together, these shifts keep the automotive fuel delivery system market size for components on an upward curve despite future EV displacement threats.

Passenger cars delivered 64.33% of the automotive fuel delivery system market revenue in 2024. Hatchbacks and sedans require cost-efficient returnless pumps, whereas SUVs integrate higher-pressure rails because of increased torque loads. Light commercial vehicles, forecast at 6.23% CAGR, prefer robustness over efficiency, sustaining steel-braid hoses and replaceable filters, a pattern that enlarges the automotive fuel delivery system market share commanded by commercial platforms.

Longer daily mileage and fleet telematics open retrofitting business, while medium and heavy trucks, though smaller in volume, retain high-flow diesel injection rails that stabilize volumes until battery densities permit long-haul substitution. As such, the automotive fuel delivery system market remains diversified across duty cycles.

The Automotive Fuel Delivery System Market Report is Segmented by Component (Fuel Pump, Fuel Injector, and More), Vehicle Type (Passenger Cars, and Commercial Vehicles), Fuel Type (Gasoline, Diesel, and More), Delivery Method (Port Fuel Injection, Gasoline Direct Injection, and More), Distribution Channel (OEM (Factory-Fitted) and Aftermarket (Replacement)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific captured 38.55% of the automotive fuel delivery system market's 2024 turnover and will outpace all other regions with a 6.92% CAGR to 2030, owing to China's outsized production, India's highway expansion, and ASEAN's localized assembly clusters. Chinese OEMs are building fuel-system subsystems in Thailand and Indonesia to bypass tariffs and shorten logistics chains, strengthening the automotive fuel delivery system market across Southeast Asia. Semiconductor joint ventures in Japan also secure microcontroller flow for high-pressure pumps, buffering regional supply risk.

North America remains technology-rich, driven by EPA regulations that mandate 0.035 g/b-hp-hr NOx by 2027. Investments such as the USDA's USD 26 million E15 infrastructure program expand biofuel uptake, creating niche demand for ethanol-ready rails and seals that enlarge the automotive fuel delivery system market. Mexico's attractively priced labor and USMCA trade benefits encourage tier-1s to add capacity in Ramos Arizpe and Aguascalientes.

Europe faces the twin pressures of Euro 7 and accelerated carbon-neutrality pledges. OEMs are retrofitting particulate filters and vapor-containment hardware ahead of 2026, raising per-vehicle bill-of-materials but sustaining supplier order books. Eastern European plants offer lower costs for line assemblies, ensuring competitiveness even as Western European factories pivot to electric modules. Hydrogen corridor pilots from Spain to Germany are also giving the automotive fuel delivery system market an early foothold in fuel-cell applications.

- Robert Bosch GmbH

- Continental AG

- DENSO Corporation

- Delphi Technologies (BorgWarner)

- Magna International Inc.

- TI Fluid Systems plc (TI Automotive)

- Toyoda Gosei Co., Ltd.

- Ucal Fuel Systems Ltd.

- Marelli Holdings Co., Ltd.

- Hitachi Astemo Ltd.

- Stanadyne LLC

- Carter Fuel Systems LLC

- Aisin Corporation

- Valeo SA

- MS Motorservice International GmbH (Pierburg)

- Walbro LLC

- Johnson Electric Holdings Ltd.

- Woodward, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent emission norms driving adoption of advanced fuel-delivery modules

- 4.2.2 Rising global vehicle production and parc rejuvenation

- 4.2.3 Growing demand for gasoline direct-injection engines in passenger cars

- 4.2.4 Increasing sales of light commercial vehicles in emerging markets

- 4.2.5 Integration of smart diagnostics within electric fuel pumps

- 4.2.6 Surge in synthetic/bio-fuel blends requiring corrosion-resistant lines

- 4.3 Market Restraints

- 4.3.1 Rapid growth of electric vehicles reducing ICE share

- 4.3.2 Volatility in raw-material prices for fuel-system components

- 4.3.3 Tightening evaporative-emission norms raising system cost

- 4.3.4 Semiconductor shortages disrupting electronic pump controllers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Fuel Pump

- 5.1.2 Fuel Injector

- 5.1.3 Fuel Rail

- 5.1.4 Fuel Pressure Regulator

- 5.1.5 Fuel Filter

- 5.1.6 Fuel Line and Hoses

- 5.1.7 Others

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.1.1 Hatchback

- 5.2.1.2 Sedan

- 5.2.1.3 Sports Car and Coupe

- 5.2.1.4 SUV and Crossover

- 5.2.2 Commercial Vehicles

- 5.2.2.1 Light Commercial Vehicles (LCV)

- 5.2.2.2 Medium and Heavy Commercial Vehicles (MCV and HCV)

- 5.2.1 Passenger Cars

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.3.3 Flex Fuel (E10-E85)

- 5.3.4 CNG and LPG

- 5.3.5 Biofuel and Synthetic Fuel

- 5.3.6 Hydrogen

- 5.4 By Delivery Method

- 5.4.1 Port Fuel Injection

- 5.4.2 Gasoline Direct Injection

- 5.4.3 Returnless Fuel Systems

- 5.4.4 Common-Rail Diesel Injection

- 5.5 By Distribution Channel

- 5.5.1 OEM (Factory-fitted)

- 5.5.2 Aftermarket (Replacement)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Nigeria

- 5.6.5.6 Egypt

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 DENSO Corporation

- 6.4.4 Delphi Technologies (BorgWarner)

- 6.4.5 Magna International Inc.

- 6.4.6 TI Fluid Systems plc (TI Automotive)

- 6.4.7 Toyoda Gosei Co., Ltd.

- 6.4.8 Ucal Fuel Systems Ltd.

- 6.4.9 Marelli Holdings Co., Ltd.

- 6.4.10 Hitachi Astemo Ltd.

- 6.4.11 Stanadyne LLC

- 6.4.12 Carter Fuel Systems LLC

- 6.4.13 Aisin Corporation

- 6.4.14 Valeo SA

- 6.4.15 MS Motorservice International GmbH (Pierburg)

- 6.4.16 Walbro LLC

- 6.4.17 Johnson Electric Holdings Ltd.

- 6.4.18 Woodward, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment