PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836661

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836661

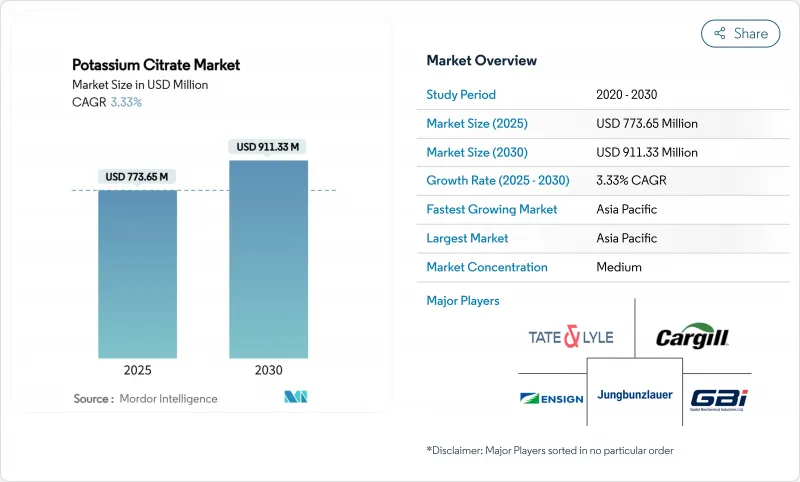

Potassium Citrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The global potassium citrate market stands at USD 773.65 million in 2025 and is projected to reach USD 911.33 million by 2030, expanding at a CAGR of 3.33% during the forecast period.

This moderate yet consistent growth trajectory reflects the compound's entrenched position across multiple high-value applications, from sodium reduction initiatives in processed foods to specialized pharmaceutical formulations for renal health management. The market's resilience stems from potassium citrate's unique dual functionality as both a food additive and active pharmaceutical ingredient, positioning it at the intersection of two robust end-use sectors that continue to prioritize health-conscious formulations. Regulatory momentum significantly amplifies market dynamics, particularly through the FDA's Phase II sodium reduction guidance issued in August 2024, which targets average sodium intake reduction to 2,750 mg per day. This initiative directly benefits potassium citrate manufacturers, as food processors increasingly substitute sodium-based additives with potassium alternatives to meet regulatory targets while maintaining product functionality. Simultaneously, the beverage sector's growing emphasis on pH control agents for product stability and taste enhancement creates additional demand vectors, particularly in functional and sports drink categories where electrolyte balance remains paramount.

Global Potassium Citrate Market Trends and Insights

Surging Use of Potassium Citrate as a Sodium-Free Food Additive

Global efforts to reduce sodium in food systems are propelling the growth of the potassium citrate market. With regulatory bodies advocating for reduced sodium consumption, potassium citrate stands out as a viable substitute. Being sodium-free, it can replace conventional sodium-based additives, preserving crucial functions like buffering, emulsification, and mineral fortification. This is especially vital in processed foods, where sodium salts have long been essential. Data from the Centers for Disease Control and Prevention (January 2024) highlights the issue: Americans average 3,400 milligrams of sodium daily, well above the federal recommendation of 2,300 milligrams for teens and adults. This overconsumption is linked to serious health concerns. From August 2021 to August 2023, adult hypertension in the U.S. hit 47.7%, with men at 50.8% and women at 44.6%, and rates climbing with age . The regulatory landscape is shifting, with a clear push for sodium-reduction measures in the industry, aiming for compliance by 2026. This urgency boosts the demand for potassium citrate as a reliable sodium alternative. Potassium citrate can be easily incorporated into current food formulations, sparing manufacturers from intricate adjustments. This ensures product quality and shelf stability while adhering to health standards. Heightened consumer health awareness, solid epidemiological links between sodium and cardiovascular risks, and tightening regulatory sodium limits fuel the growing adoption of potassium citrate in various food applications.

Increasing Preference for Clean-Label and Health-Focused Ingredients

Driven by evolving consumer preferences for clean-label and health-centric formulations, the food and beverage industry is undergoing a significant transformation, with notable repercussions for the potassium citrate market. While potassium citrate is industrially synthesized, it enjoys a favorable consumer perception, largely due to its association with naturally occurring citric acid. In-depth consumer studies reveal a growing inclination towards ingredients perceived as natural or those that offer pronounced nutritional advantages. This trend is particularly evident in the European natural food additives market, where regulatory frameworks are increasingly endorsing ingredients sourced from natural origins or processes . Manufacturers have adeptly repositioned potassium citrate, emphasizing its ties to traditional food preservation and its role as a potassium source, vital for cardiovascular health and electrolyte balance. Highlighting this trend, the International Food Information Council's 2023 research found that about 26% of U.S. respondents view "natural and low-sodium" as the foremost indicator of healthy food . This underscores a rising consumer demand for straightforward, natural formulations.

Stringent Regulatory Compliance in Pharmaceutical and Food Sector

Pharmaceutical applications of potassium citrate face increasingly complex regulatory requirements that extend development timelines and increase compliance costs for manufacturers. The FDA's drug master file requirements for pharmaceutical-grade potassium citrate demand extensive documentation of manufacturing processes, impurity profiles, and stability data, creating barriers for smaller suppliers seeking to enter high-value pharmaceutical markets. USP monograph requirements specify stringent purity standards exceeding 99.5% for pharmaceutical applications, necessitating sophisticated manufacturing processes and quality control systems that increase production costs. International harmonization efforts, while beneficial long term, create short-term compliance complexity as manufacturers must navigate varying requirements across major markets. The regulatory landscape becomes particularly challenging for combination products where potassium citrate interacts with other active ingredients, requiring extensive stability and compatibility testing. These compliance requirements favor established pharmaceutical suppliers with existing regulatory infrastructure while creating market entry barriers that limit competitive intensity in premium segments.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Cosmetic and Personal Care Formulations Using Chelating Agents

- Rising Popularity of Vegan and Plant-Based Supplementation Solution

- Taste Alteration in Food Limiting Wider Acceptance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, the high-purity potassium citrate segment, boasting purity levels more than 99%, commanded a dominant 42.44% market share. This trend highlights a growing appetite for ultra-refined formulations, particularly in premium pharmaceuticals and niche food applications. Stringent regulatory standards and the paramount importance of formulation precision primarily drive the surge in demand. In sectors like pharmaceuticals, where even minute impurities can jeopardize safety or therapeutic outcomes, this emphasis on purity is critical. Potassium citrate, in these settings, plays dual roles: as an active ingredient and a buffering agent, notably in renal health treatments and extended-release drugs. The segment's dominance underscores the industry's unwavering commitment to purity and stringent quality benchmarks. Meanwhile, the 98-99% purity tier finds its niche in food processing and select industrial applications, where functional performance is key, but ultra-high purity isn't a prerequisite.

Meanwhile, the segment with purity levels below 98% is witnessing the most rapid expansion, boasting a notable CAGR of 4.64%. Its growth trajectory is fueled by its attractiveness in high-volume applications that prioritize cost-effectiveness and consistent operations over absolute purity. Key drivers include its burgeoning use in animal nutrition, bulk food production, and pH regulation across diverse sectors. In response, manufacturers are pivoting, rolling out more budget-friendly potassium citrate formulations that fulfill essential functional needs, sidestepping the premium of ultra-refinement. This divergence in purity preferences paints a picture of a maturing market landscape. Potassium citrate has evolved from a generic commodity to a tailored solution, catering to varied end-user demands. Such an evolution not only sparks innovation but also enhances supply chain adaptability and competitive edge, spanning both premium and budget-conscious market segments.

The Potassium Citrate Market is Segmented by Purity (Less Than 98%, 98 - 99%, and More Than 99%), by Application (Food and Beverage, Industrial, Dietary Supplement, Personal Care and Cosmetics, and Others), and by Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2024, Asia-Pacific not only emerged as the largest regional market, holding a 31.32% share, but also showcased its rapid growth, boasting a 5.44% CAGR projected through 2030. This growth is largely attributed to the region's expanding food processing infrastructure and a heightened health consciousness among its urban populace. Ongoing trade investigations and antidumping reviews underscore China's leading role in citrate production. In India, the burgeoning pharmaceutical sector fuels the demand for high-purity potassium citrate, essential for generic drug manufacturing. Simultaneously, India's expanding processed food industry presents significant volume opportunities for food-grade applications. Meanwhile, Japan and Australia are driving regional growth by focusing on premium applications in functional foods and dietary supplements, with consumers willing to pay a premium for perceived health benefits.

North America, while mature, is undergoing an evolution, largely driven by regulatory initiatives reshaping demand. The FDA's guidance on sodium reduction has spurred a consistent demand for potassium citrate as a sodium substitute. Concurrently, North America's advanced pharmaceutical sector ensures a steady appetite for high-purity grades tailored for specialized therapeutic uses. Notably, Canada's involvement in trade investigations, alongside China, underscores the region's intertwined supply chains and the resultant competitive dynamics influencing pricing and product availability. Additionally, Mexico's burgeoning food processing sector amplifies the demand, especially for health-conscious consumers seeking reduced-sodium options in traditional foods.

Europe stands at the forefront of clean-label and natural ingredient trends, with potassium citrate gaining traction as a natural substitute for synthetic additives. The EU's regulatory stance, which leans towards natural preservatives, has elevated potassium citrate's market value, especially in organic and premium food sectors. Furthermore, Europe's sophisticated cosmetic industry is increasingly turning to potassium citrate as a preferred alternative to EDTA in personal care products. With a pronounced emphasis on sustainability,

- Cargill, Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland (ADM)

- Jungbunzlauer Suisse AG

- Gadot Biochemical Industries

- Cofco Biochemical

- Huangshi Xinghua Biochemical

- Biofuran Materials

- American Tartaric Products

- Juxian Hongde Citric Acid

- Wang Pharmaceuticals & Chemicals

- Vishal Laboratories

- DPL-US

- Weifang Ensign Industry

- Spectrum Chemical Mfg Corp.

- Adani Pharmachem Private Limited

- Merck KGaA

- Dr. Paul Lohmann

- FBC Industries

- Ava Chemicals Private Limited,

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Use of Potassium Citrate as a Sodium-Free Food Additive

- 4.2.2 Increasing Preference for Clean-Label and Health-Focused Ingredients

- 4.2.3 Surge in Cosmetic and Personal Care Formulations Using Chelating Agents

- 4.2.4 Rising Popularity of Vegan and Plant-Based Supplementation Solution

- 4.2.5 Growing Awarness of Natural Preservatives in Food Safety

- 4.2.6 Amplyfing Demand from the Beverage Sector for pH Control Agents

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Compliance in Pharmaceutical and Food Sector

- 4.3.2 Taste Alteration in Food Limiting Wider Acceptance

- 4.3.3 Storage and Stability Challenges During Long-Tem Use

- 4.3.4 Consumer Skepticism Towards Chemical-Sounding Additives

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Purity

- 5.1.1 Less than 98%

- 5.1.2 98 - 99%

- 5.1.3 More than 99%

- 5.2 By Application

- 5.2.1 Food and Beverage

- 5.2.2 Industrial

- 5.2.3 Dietary Supplement

- 5.2.4 Personal Care and Cosmetics

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 Netherlands

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Singapore

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 Tate & Lyle PLC

- 6.4.3 Archer Daniels Midland (ADM)

- 6.4.4 Jungbunzlauer Suisse AG

- 6.4.5 Gadot Biochemical Industries

- 6.4.6 Cofco Biochemical

- 6.4.7 Huangshi Xinghua Biochemical

- 6.4.8 Biofuran Materials

- 6.4.9 American Tartaric Products

- 6.4.10 Juxian Hongde Citric Acid

- 6.4.11 Wang Pharmaceuticals & Chemicals

- 6.4.12 Vishal Laboratories

- 6.4.13 DPL-US

- 6.4.14 Weifang Ensign Industry

- 6.4.15 Spectrum Chemical Mfg Corp.

- 6.4.16 Adani Pharmachem Private Limited

- 6.4.17 Merck KGaA

- 6.4.18 Dr. Paul Lohmann

- 6.4.19 FBC Industries

- 6.4.20 Ava Chemicals Private Limited,

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK