PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836676

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836676

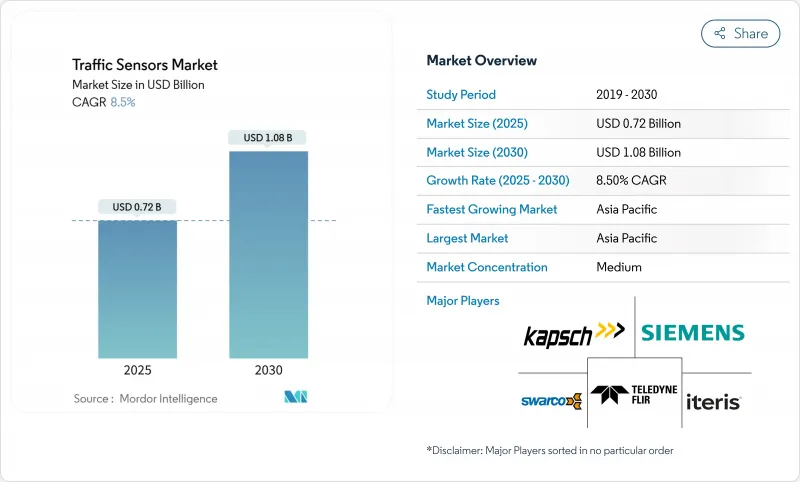

Traffic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The traffic sensors market size reached USD 0.72 billion in 2025 and is on course to expand to USD 1.08 billion by 2030, reflecting an 8.50% CAGR.

Demand rises as cities scale intelligent transportation systems to relieve congestion and cut emissions, and as national agencies lock in multi-year funding for sensor-enabled infrastructure. Statutory real-time data requirements for congestion pricing, dynamic tolling and safety programs anchor new procurement cycles, while edge-AI and 5G connectivity shift the competitive focus from stand-alone hardware to data-rich, upgrade-ready platforms. Asia-Pacific leads adoption on the back of China's and Japan's large-scale smart-city pilots, whereas North America prioritizes retrofits that minimize lane closures. Vendors able to bundle non-intrusive detection, predictive analytics and open-standards communications secure the widest addressable base, especially as governments press for multi-modal coverage that includes pedestrians and micromobility devices.

Global Traffic Sensors Market Trends and Insights

Urbanisation & Congestion Pressure

Metropolitan congestion costs New York USD 20 billion each year, prompting large-scale sensor roll-outs that shorten travel times by as much as 25% and trim CO2 output up to 20% trafficmobilityreviewboard. Federal Highway Safety Improvement funds of USD 3.4 billion embed detection into roadway upgrades to cut fatalities. China's nearly 800 smart-city pilots further accelerate deployments that span vehicles, pedestrians and micromobility users, broadening the traffic sensors market beyond road vehicles alone

Smart-City & ITS Funding Surge

The USD SMART Grants program disbursed USD 50 million across 34 projects in 2024, setting precedents for sensor-rich intersections and edge servers .Horizon Europe earmarked EUR 254 million (USD 276 million) to digital transport infrastructure that mandates interoperable detection. City-level initiatives, such as Alexandria's USD 5 million smart-mobility plan, confirm that funding is cascading rapidly to municipal procurement

High Up-Front Deployment CAPEX

ITS America estimates USD 6.5 billion is needed to equip 250,000 U.S. intersections with V2X technology, a burden intensified by paving, labor and maintenance costs . Developing economies face financing gaps that delay roll-outs, although low-cost wireless nodes such as Oklahoma's USD 40 prototype ease entry barriers Contracts like Rhode Island's USD 2.759 million bridge monitoring deal highlight the sizable capital commitment even for individual assets

Other drivers and restraints analyzed in the detailed report include:

- Mandated Real-Time Data for Tolling & Congestion Pricing

- Edge-AI Low-Power Non-Intrusive Sensors

- Data-Privacy & Cyber-Security Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inductive loops retained 38% traffic sensors market share in 2024, yet LiDAR's 12.2% CAGR signals a pivot to non-intrusive, high-resolution mapping. The traffic sensors market size attached to LiDAR solutions is projected to outpace loops as operators seek vehicle classification and pedestrian safety in one package. Seyond's system posts 99% vehicle accuracy and 92% pedestrian recognition, outperforming loop-based alternatives simpl.. Radar and thermal imaging complement LiDAR in adverse weather, while piezoelectric arrays remain vital for weigh-in-motion. Edge-ready sensors that combine modalities collect richer data with lower lifecycle cost, a priority under federal SMART guidance

LiDAR's upward curve is reinforced by falling component prices, smaller form factors and automotive-grade reliability. Traditional loops struggle with pavement wear and lane additions, and their inability to detect cyclists limits suitability for multimodal grids. Infrared and magnetometer solutions hold niche roles where cost or site constraints dictate. A diverse supplier ecosystem is emerging, yet integration skill remains a differentiator as agencies favor turnkey analytics over raw feed delivery.

Intrusive installs made up 54% revenue in 2024 as legacy loops dominate signalized junctions, but portable sensors are forecast for 12.0% CAGR. The traffic sensors market increasingly rewards quick-deploy, solar-powered units that avoid lane closures and asphalt cutting. Oklahoma's USD 40 wireless node underscores cost competitiveness even for cash-constrained districts. Portable LiDAR kits now underpin work-zone situational awareness, easing contractor compliance with safety mandates.

Traffic managers prioritize flexibility to realign sensors with construction phases, events or pop-up bus lanes. Non-intrusive over-road gear delivers multi-lane coverage and diagnostics without disturbing pavement integrity. Long-term, loop retrofits shift toward radar-camera combos delivering higher data fidelity and lower lifetime spend.

The Traffic Sensor Market is Segmented by Sensor Type (Inductive Loop, and More), Application ( Weigh in Motion and More), Installation Method (Intrusive (In-Road) and More), Deployment Location (Urban Intersections and More), End-Use Sector (Government and Road Agencies and More), Connectivity Technology (Wired and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 35% 2024 revenue and posts a 12.1% CAGR through 2030. China's smart-city pilots, anchored in the Made in China 2025 program, keep urban infrastructure budgets flowing toward AI-enabled detection. Japan's advanced traffic systems sector targets USD 7.239 billion by 2033 as Ministry-approved projects integrate flow prediction and visualization. India's USD 1.4 trillion National Infrastructure Pipeline underlines rising demand for multimodal logistics monitoring .

North America commands mature install bases yet continues to invest in retrofit upgrades. USD 100 million annual SMART allocations and congestion pricing in New York spur edge-ready replacements. Retrofit-friendly, non-intrusive sensors dominate procurements that must minimize lane closures. Canada modernizes corridor management through federal-provincial cost sharing, whereas Mexico focuses on freight corridors linked to USMCA trade flows.

Europe links sensor projects to decarbonization targets. Horizon Europe and the EUR 1 billion Connected, Cooperative and Automated Mobility program fund multi-modal detection interoperability. Germany and the UK channel funds into rail and high-speed roadways that embed next-gen sensors suitable for future autonomous deployment. Middle East and Africa exhibit selective adoption tied to flagship smart-city schemes, though oil-exporting states fund toll and weigh-in-motion networks to safeguard heavy-load corridors.

- Kapsch TrafficCom AG

- Siemens AG

- FLIR (Teledyne)

- Iteris Inc.

- Q-Free ASA

- SWARCO AG

- International Road Dynamics

- Sensys Networks Inc.

- Kistler Group

- Bosch Security & Safety Systems

- Axis Communications

- Smartmicro GmbH

- SICK AG

- EFKON GmbH

- Citilog (Swarco)

- Raytheon Technologies

- Sensata Technologies

- LeddarTech Inc.

- IHI Corporation

- Acyclica (FLIR)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanisation and Congestion Pressure

- 4.2.2 Smart-City and ITS Funding Surge

- 4.2.3 Mandated Real-Time Data for Tolling and Congestion Pricing

- 4.2.4 Electrification-Linked Grid-Aware Traffic Management

- 4.2.5 Edge-AI Low-Power Non-Intrusive Sensors

- 4.2.6 Multimodal Micromobility Detection Standards

- 4.3 Market Restraints

- 4.3.1 High Up-Front Deployment CAPEX

- 4.3.2 Data-Privacy & Cyber-Security Compliance Costs

- 4.3.3 Climate-Driven Sensor Degradation (Heat and Salinity)

- 4.3.4 Fragmented Protocols Hindering Interoperability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Inductive Loop

- 5.1.2 Piezoelectric

- 5.1.3 Bending Plate

- 5.1.4 Magnetometer

- 5.1.5 Image / Video

- 5.1.6 Radar-Based

- 5.1.7 Infrared

- 5.1.8 LiDAR

- 5.2 By Installation Method

- 5.2.1 Intrusive (In-Road)

- 5.2.2 Non-Intrusive (Over-Road / Roadside)

- 5.2.3 Portable / Temporary

- 5.3 By Application

- 5.3.1 Traffic Monitoring and Flow Optimisation

- 5.3.2 Weigh-In-Motion

- 5.3.3 Vehicle Classification and Profiling

- 5.3.4 Automated and Dynamic Tolling

- 5.3.5 Incident Detection and Safety Analytics

- 5.4 By Deployment Location

- 5.4.1 Urban Intersections

- 5.4.2 Highways and Expressways

- 5.4.3 Bridges and Tunnels

- 5.4.4 Parking Facilities

- 5.5 By End-Use Sector

- 5.5.1 Government and Road Agencies

- 5.5.2 Toll Operators / PPP Concessions

- 5.5.3 Smart-City Solution Integrators

- 5.5.4 Logistics and Fleet Operators

- 5.6 By Connectivity Technology

- 5.6.1 Wired (CAN, Ethernet)

- 5.6.2 Wireless (DSRC / C-V2X)

- 5.6.3 Cellular-IoT (NB-IoT / LTE-M / 5G)

- 5.6.4 LPWAN (LoRa / Sigfox)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Italy

- 5.7.3.6 Rest of Europe

- 5.7.4 APAC

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 Australia

- 5.7.4.5 Rest of APAC

- 5.7.5 Middle East and Africa

- 5.7.5.1 GCC

- 5.7.5.2 South Africa

- 5.7.5.3 Rest of Middle East and Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Kapsch TrafficCom AG

- 6.3.2 Siemens AG

- 6.3.3 FLIR (Teledyne)

- 6.3.4 Iteris Inc.

- 6.3.5 Q-Free ASA

- 6.3.6 SWARCO AG

- 6.3.7 International Road Dynamics

- 6.3.8 Sensys Networks Inc.

- 6.3.9 Kistler Group

- 6.3.10 Bosch Security & Safety Systems

- 6.3.11 Axis Communications

- 6.3.12 Smartmicro GmbH

- 6.3.13 SICK AG

- 6.3.14 EFKON GmbH

- 6.3.15 Citilog (Swarco)

- 6.3.16 Raytheon Technologies

- 6.3.17 Sensata Technologies

- 6.3.18 LeddarTech Inc.

- 6.3.19 IHI Corporation

- 6.3.20 Acyclica (FLIR)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment