PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842478

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842478

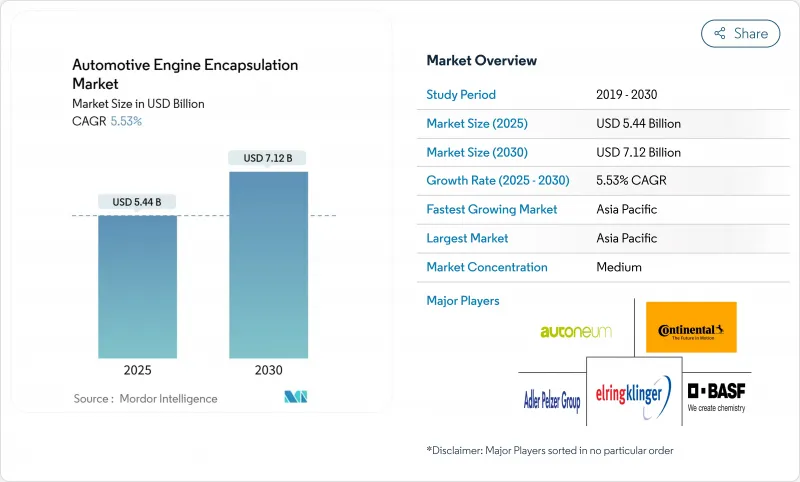

Automotive Engine Encapsulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The automotive engine encapsulation size market is valued at USD 5.44 billion in 2025 and is projected to reach USD 7.12 billion by 2030, reflecting a robust 5.53% CAGR.

Demand accelerates as Euro 7 regulations tighten cold-start CO2 limits, premium brands chase library-quiet cabins, and hybrid powertrains require sophisticated under-hood thermal control. Automakers adopt gigacasting and digital-twin design loops that merge structural, thermal, and acoustic functions, cutting component counts while boosting thermal efficiency. Material strategies pivot toward recyclable thermoplastics to meet circular-economy mandates, and carbon-fiber cost declines open lightweight options for mid-volume models. Suppliers form alliances with battery-thermal specialists to bridge ICE and EV requirements as the automotive engine encapsulation market navigates the combustion-to-electric transition.

Global Automotive Engine Encapsulation Market Trends and Insights

Stricter Post-Euro 7 Cold-Start CO2 Targets

Euro 7 takes effect for new vehicle types in November 2026 and extends compliance to 200,000 km, putting cold-start emissions under unprecedented scrutiny. Automakers now need encapsulation that accelerates warm-up times and dampens engine noise across ambient ranges from -7°C to 35°C. The requirement pushes hybrid material stacks that blend carbon-fiber structures with phase-change layers, securing emission compliance without sacrificing acoustics.

Premium-Brand Shift to Library-Quiet ICE Cabins

Luxury marques target idle cabin noise below 40 dB, mirroring silent EV experiences. Multi-layer encapsulation with aerogel barriers achieves noise reduction coefficients above 0.9 while sustaining thermal insulation. Programs now extend beyond engines to transmission tunnels, treating the full powertrain as one acoustic source for a unified solution.

Rapid BEV Power-Train Mix Diluting ICE Volume

BEV penetration in new car registration across Europe hit 15.40% in 2024 and is forecast to be above 50% by 2030, shrinking demand for ICE-specific encapsulation. Suppliers must reinvest profits from declining ICE programs into EV-thermal products or face margin erosion.

Other drivers and restraints analyzed in the detailed report include:

- Battery Pre-Conditioning Needs in PHEVs

- Lightweight Carbon-Fiber Cost Curve Inflection

- Petro-Chemical Price Volatility for Polymer Foams

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine-mounted encapsulations led the automotive engine encapsulation market with a 51.71% share in 2024. These modules excel at vibration isolation because they sit directly on the power unit, enabling rapid warm-up and line-side installation. Body-mounted designs are accelerating at 7.56% CAGR and increasingly cast into large underbody sections, supporting platform consolidation and lowering assembly time.

Body-mounted encapsulation integrates acoustic barriers with structural members, improving stiffness while sealing the engine bay. This format dovetails with gigacast underbodies that eliminate multiple brackets and fasteners. Suppliers must formulate materials that tolerate die-casting thermal cycles without delamination. Consequently, the automotive engine encapsulation market size for body-mounted solutions is projected to expand steadily through 2030.

Gasoline engines accounted for 65.91% automotive engine encapsulation market size in 2024, supported by their prevalence in global passenger fleets. Encapsulation for gasoline units emphasizes rapid warm-up and idle noise suppression.

Electric powertrains exhibit the briskest 7.87% CAGR because hybrids and range-extended models blend battery cooling with combustion insulation. Suppliers engineer dual-purpose barriers that protect cells from engine heat spikes while muting inverter whine. Diesel remains for torque-intensive use cases but faces cost headwinds due to after-treatment complexity.

The Automotive Engine Encapsulation Market Report is Segmented by Product Type (Engine-Mounted and Body-Mounted), Fuel Type (Gasoline, Diesel, and More), Material Type (Carbon Fiber, Polyurethane, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM-Fitted and Aftermarket), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the automotive engine encapsulation market with 48.55% share in 2024 and is advancing at 8.52% CAGR. China's dominance derives from vast vehicle output and policy-driven hybrid growth that prolongs ICE encapsulation demand even in an EV-centric roadmap. India's production-linked incentives lure suppliers to localize encapsulation, combining cost competitiveness with duty advantages.

Europe ranks second as Euro 7 catalyzes advanced solutions for cold-start emissions, plus widespread hybrid adoption that prolongs ICE relevance. Carbon-fiber and digital-twin tools mature here first, then migrate globally, reinforcing the region's thought leadership. North America grows steadily on the back of SUV and pickup sales that use larger powertrains, which need robust thermal-acoustic barriers.

The Middle East and Africa, and South America remain emerging pockets. They rely on imported NVH kits or CKD assembly, yet rising local output attracts suppliers establishing greenfield plants. Altogether, the automotive engine encapsulation market continues regional consolidation around APAC capacity while Europe drives specification trends embraced worldwide.

- Autoneum Holding AG

- Continental AG

- ElringKlinger AG

- BASF SE

- 3M Company

- Rochling Group

- Adler Pelzer Group

- Trocellen Automotive

- Woco Group

- SA Automotive

- Charlotte Baur Formschaumtechnik GmbH

- Sumitomo Riko Co. Ltd

- Sika Automotive

- Pritex Ltd

- UGN Inc.

- Langfang Sound (China)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter post-Euro 7 cold-start CO2 targets

- 4.2.2 Premium-brand shift to "library-quiet" ICE cabins

- 4.2.3 Battery pre-conditioning needs in PHEVs

- 4.2.4 Lightweight carbon-fiber cost curve inflection

- 4.2.5 Gigacasting enabling larger body-mounted encapsulations

- 4.2.6 OEM digital twins optimising under-hood thermal maps

- 4.3 Market Restraints

- 4.3.1 Rapid BEV power-train mix diluting ICE volumes

- 4.3.2 Petro-chemical price volatility for polymer foams

- 4.3.3 Limited recyclability of multi-layer NVH composites

- 4.3.4 Engine-bay packaging conflicts in downsized ICEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers / Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Engine-Mounted

- 5.1.2 Body-Mounted

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Electric

- 5.3 By Material Type

- 5.3.1 Carbon Fiber

- 5.3.2 Polyurethane

- 5.3.3 Polypropylene

- 5.3.4 Polyamide

- 5.3.5 Glasswool

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Sales Channel

- 5.5.1 OEM-Fitted

- 5.5.2 Aftermarket

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Autoneum Holding AG

- 6.4.2 Continental AG

- 6.4.3 ElringKlinger AG

- 6.4.4 BASF SE

- 6.4.5 3M Company

- 6.4.6 Rochling Group

- 6.4.7 Adler Pelzer Group

- 6.4.8 Trocellen Automotive

- 6.4.9 Woco Group

- 6.4.10 SA Automotive

- 6.4.11 Charlotte Baur Formschaumtechnik GmbH

- 6.4.12 Sumitomo Riko Co. Ltd

- 6.4.13 Sika Automotive

- 6.4.14 Pritex Ltd

- 6.4.15 UGN Inc.

- 6.4.16 Langfang Sound (China)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment