PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939722

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939722

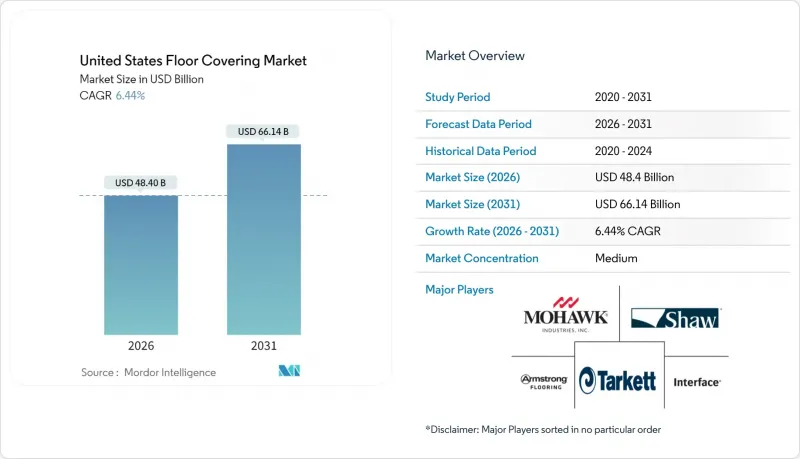

United States Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The US flooring market was valued at USD 45.47 billion in 2025 and estimated to grow from USD 48.4 billion in 2026 to reach USD 66.14 billion by 2031, at a CAGR of 6.44% during the forecast period (2026-2031).

Residential renovation activity, resilient product innovation, and strong population growth in Sunbelt states underpin the current momentum of the US flooring market. Demand is reinforced by tax-advantaged commercial retrofits that offset the drag from high borrowing costs. Scale manufacturers concentrate on waterproof and scratch-resistant technologies, while direct-to-consumer e-commerce rapidly reshapes go-to-market models. Sustained raw-material inflation and an acute installer shortage remain the key cost pressures that temper the otherwise upbeat outlook of the US flooring market.

United States Floor Covering Market Trends and Insights

IRA-Backed Commercial Retrofit Tax Incentives Accelerating Flooring Upgrades

Expanded eligibility for tax-exempt entities unlocks demand from government and nonprofit facilities that have historically delayed floor replacements. Retrofits dovetail with post-pandemic reconfiguration of interiors, so flooring upgrades that deliver both acoustic and thermal performance rise to the top of specification lists. Design firms are aligning bids with tax schedules, creating a steady backlog for installers in dense commercial districts. The change supports premium resilient and carpet-tile platforms that incorporate recycled content while meeting energy targets.

Flexible Workspace Boom Driving Modular Flooring Demand in Offices and Co-working Hubs

Hybrid work models catalyze demand for modular flooring that can be lifted and re-laid when seating plans change. Carpet tile volumes surpassed pre-pandemic commercial forecasts as operators seek quick-turn solutions during lease renegotiations. Resimercial aesthetics blend soft textures with hard-surface accents so designers specify collections that balance underfoot comfort with chair-castor durability. Acoustic backing systems mitigate noise in open plans and support wellness certifications. Smaller installation zones favour click-lock systems that minimize downtime, a feature prized by co-working providers that monetize space churn. Suppliers are therefore investing in dye-infusion print technologies that enable rapid customization without extending lead times.

High Interest Rates Suppressing New Office and Retail Build-outs

Transaction volumes in commercial real estate fell 37% in 2023 and a further 14% in 2024 . Developers defer speculative ground-ups, curbing floor covering demand in large core-shell projects. Vacancies in legacy office towers extend retrofit cycles, pushing landlords to phase upgrades rather than execute full-floor replacements. Retail capital expenditure is similarly cautious as e-commerce captures discretionary spending. The US flooring market thus shifts focus toward refurbishment programs that can proceed under constrained budgets. Suppliers bundle value-engineered lines with financing support, yet volume shortfalls in gateway cities continue to temper overall growth.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Construction Surge Requiring Low-VOC Resilient Surfaces

- E-commerce Warehouse Expansion Increasing Durable Hard-Surface Installations

- Skilled Installer Shortage Elevating Labor Costs and Project Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carpets and rugs retained 35.62% of the US flooring market in 2025 due to acoustic benefits in multifamily housing and offices. However, resilient flooring is forecast to grow at a 7.80% CAGR, almost 1.4 percentage points above the overall US flooring market. Luxury vinyl tile and rigid core collections spearhead adoption because they deliver waterproof performance and easy maintenance. The shift pulls share from non-resilient hard surfaces such as site-finished wood and ceramic in entry-level price tiers. Notably, PVC-free resilient lines led by Mohawk's PureTech have broadened acceptance among sustainability-focused buyers.

In 2024, the resilient category also benefited from cost stabilization in calcium carbonate fillers, supporting aggressive promotional pricing during peak remodeling season. As a result, SPC click-lock planks featured prominently in direct-to-consumer bundles marketed through social platforms. Manufacturers augment margins through proprietary wear layers that qualify for extended warranties, a feature that resonates with homeowners concerned about long-term value.

The US Floor Covering Market Segments Into by Product Type (Carpet and Rugs, Resilient Flooring Luxury Vinyl Tile (LVT), and More), End-User (Residential, and Commercial Office), Distribution Channel (Specialty Flooring Retailers, Big-Box Home Centers, and More), Region (Northeast, Southeast, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shaw Industries Group Inc.

- Tarkett S.A.

- Armstrong Flooring Inc.

- Interface Inc.

- Mannington Mills Inc.

- Gerflor Group

- Forbo Flooring Systems

- LG Hausys (Hanwha)

- Beaulieu International Group

- The Dixie Group Inc.

- Milliken & Company

- Engineered Floors LLC

- Karndean Designflooring

- Roppe Corporation

- Congoleum Corporation

- AHF Products (Bruce)

- Somerset Hardwood Flooring

- Quick-Step USA

- LL Flooring Holdings Inc.

- COREtec Floors

- Tandus Centiva (Tarkett)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

5 Market Overview

- 5.1 Market Drivers

- 5.1.1 IRA-Backed Commercial Retrofit Tax Incentives Accelerating Flooring Upgrades

- 5.1.2 Flexible Workspace Boom Driving Modular Flooring Demand in Offices & Co-working Hubs

- 5.1.3 Healthcare Construction Surge Requiring Low-VOC Resilient Surfaces

- 5.1.4 E-commerce Warehouse Expansion Increasing Durable Hard-Surface Installations

- 5.1.5 Growth in Residential Construction and Renovation Activity

- 5.1.6 Rising Consumer Preferences for Sustainability and Low Maintenance

- 5.2 Market Restraints

- 5.2.1 High Interest Rates Suppressing New Office & Retail Build-outs

- 5.2.2 Petrochemical Feedstock Volatility Compressing Vinyl & Rubber Margins

- 5.2.3 Skilled Installer Shortage Elevating Labor Costs & Project Delays

- 5.2.4 Landfill Diversion Mandates Raising Carpet End-of-Life Costs

- 5.3 Value / Supply-Chain Analysis

- 5.4 Regulatory Outlook

- 5.5 Technological Outlook

- 5.6 Porter's Five Forces

- 5.6.1 Bargaining Power of Suppliers

- 5.6.2 Bargaining Power of Buyers

- 5.6.3 Threat of New Entrants

- 5.6.4 Threat of Substitutes

- 5.6.5 Industry Rivalry

- 5.7 Pricing Analysis

6 Market Size & Growth Forecasts (Value)

- 6.1 By Product Type

- 6.1.1 Carpets & Rugs

- 6.1.1.1 Broadloom Carpet

- 6.1.1.2 Carpet Tiles

- 6.1.1.3 Area Rugs

- 6.1.2 Resilient Flooring

- 6.1.2.1 Luxury Vinyl Tile (LVT)

- 6.1.2.2 Vinyl Sheet & VCT

- 6.1.2.3 Rubber Flooring

- 6.1.2.4 Linoleum

- 6.1.3 Non-Resilient Hard Surface

- 6.1.3.1 Ceramic & Porcelain Tile

- 6.1.3.2 Natural Stone Tile

- 6.1.3.3 Solid Wood Flooring

- 6.1.3.4 Engineered Wood Flooring

- 6.1.3.5 Laminate Flooring

- 6.1.3.6 Bamboo & Cork Flooring

- 6.1.1 Carpets & Rugs

- 6.2 By End-User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.2.1 Retail

- 6.2.2.2 Hospitality & Leisure

- 6.2.2.3 Healthcare

- 6.2.2.4 Education

- 6.2.2.5 Public & Institutional

- 6.2.2.6 Others

- 6.3 By Distribution Channel

- 6.3.1 Specialty Flooring Retailers

- 6.3.2 Big-Box Home Centers

- 6.3.3 Independent Contractors / Dealers

- 6.3.4 Direct-to-Consumer E-commerce

- 6.3.5 Wholesale / Distributors

- 6.4 By Region (U.S.)

- 6.4.1 Northeast

- 6.4.2 Southeast

- 6.4.3 Midwest

- 6.4.4 Southwest

- 6.4.5 West

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)Mohawk Industries Inc.

- 7.4.1 Shaw Industries Group Inc.

- 7.4.2 Tarkett S.A.

- 7.4.3 Armstrong Flooring Inc.

- 7.4.4 Interface Inc.

- 7.4.5 Mannington Mills Inc.

- 7.4.6 Gerflor Group

- 7.4.7 Forbo Flooring Systems

- 7.4.8 LG Hausys (Hanwha)

- 7.4.9 Beaulieu International Group

- 7.4.10 The Dixie Group Inc.

- 7.4.11 Milliken & Company

- 7.4.12 Engineered Floors LLC

- 7.4.13 Karndean Designflooring

- 7.4.14 Roppe Corporation

- 7.4.15 Congoleum Corporation

- 7.4.16 AHF Products (Bruce)

- 7.4.17 Somerset Hardwood Flooring

- 7.4.18 Quick-Step USA

- 7.4.19 LL Flooring Holdings Inc.

- 7.4.20 COREtec Floors

- 7.4.21 Tandus Centiva (Tarkett)

- 7.5 Market Opportunities & Future Outlook

- 7.5.1 White-Space & Unmet-Need Assessment