PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842501

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842501

Industrial Wireless Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

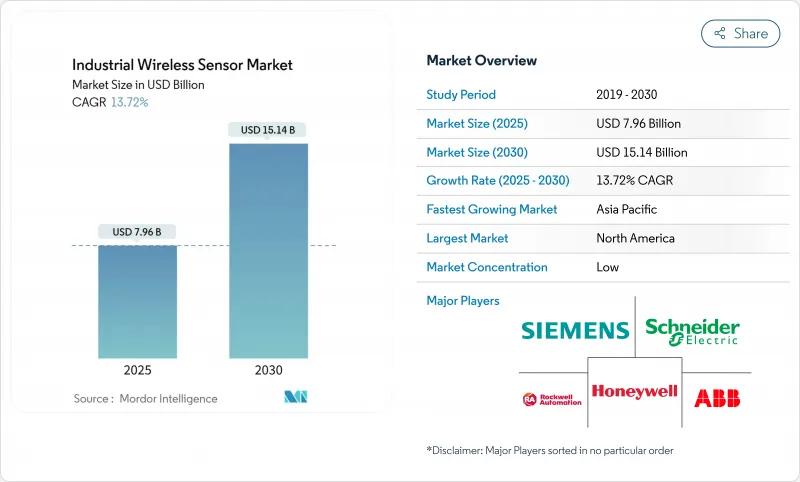

The industrial wireless sensors market size generated USD 7.96 billion in 2025 and will reach USD 15.14 billion by 2030, reflecting a 13.72% CAGR.

The expansion signals how digitalization, edge computing, and low-power wide-area networking push wireless sensing from pilot projects into core operational infrastructure. Falling chipset prices lower the total cost of ownership, while protocol innovation reduces integration risk, positioning the industrial wireless sensors market as an attractive investment priority for asset-intensive industries worldwide. Vendors continue to improve cyber-secure, battery-agnostic designs, enabling monitoring in previously inaccessible areas and unlocking data-driven maintenance strategies. This momentum accelerates platform convergence in which sensors, gateways, and analytics merge to create unified edge-to-cloud architectures that shorten decision cycles and raise asset value.

Global Industrial Wireless Sensor Market Trends and Insights

Edge-to-Cloud Analytics Demand Surge

Industrial operators now send only distilled insights instead of raw data to enterprise platforms, easing bandwidth burdens and cutting latency. Ultracompact sensors with embedded AI algorithms from firms such as TDK run machine-learning routines locally, shrinking transmitted payloads by up to 90%. Private 5G networks pair with edge servers to deliver sub-millisecond responsiveness for motion control, a milestone that broadens industrial wireless sensors market applicability into closed-loop automation. Factories deploying edge-to-cloud frameworks report 20-25% productivity gains through real-time anomaly detection. The capability aligns with sustainability goals by reducing compute energy requirements and enables predictive maintenance strategies that detect failures days in advance.

Retrofit Digitalization of Brown-Field Plants

Legacy facilities avoid disruptive rewiring costs by adding wireless nodes to equipment already running at capacity. ISA data show retrofit projects using wireless instrumentation achieve payback periods 60% shorter than wired equivalents. European chemical producers install vibration nodes on pumps and compressors to extend operating life and satisfy strict emission rules. Wireless attributes are compelling in hazardous zones where replacing or adding cables demands explosion-proof conduits, making wireless sensors a low-risk path to compliance. As brownfield estates outnumber new builds, retrofit activity will sustain double-digit volume growth across the industrial wireless sensors market well into the next decade.

Reliability Concerns in RF-Noisy Industrial Sites

Variable-frequency drives, welding lines, and power converters emit electromagnetic interference that degrades packet success rates beyond 90% reliability thresholds in some factories. Operators resort to redundant networks or revert to wired links for safety-critical loops. Mesh topologies, frequency hopping, and advanced antennas mitigate disruptions yet add cost and complexity. As interference remains prevalent in metals and automotive plants, operators apply strict qualification tests before approving wireless for real-time control, a cautionary stance that tempers portions of the industrial wireless sensors market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Low-Power Wide-Area (LPWA) Chipset Price Collapse

- Shift to Predictive Maintenance Service Models

- Scarcity of OT-Centric Cybersecurity Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure devices secured 27% industrial wireless sensors market share in 2024, reflecting their mandatory use for pipeline integrity and safety across process industries. Continuous pressure tracking avoids catastrophic leaks and satisfies stringent regulatory audits, justifying accelerated wireless retrofits where cabling through Class I Div 1 zones is cost-prohibitive. Vibration nodes grow fastest at 19.4% CAGR as predictive maintenance evolves from early pilots to corporate-wide standards, driving multi-sensor installations on rotating assets.

Temperature, flow, and gas categories secure broad adoption for environmental and quality control, while humidity and level units address niche but rising regulatory mandates in food, pharma, and tank storage. Imaging and biosensing remain nascent yet illustrate how edge AI will broaden sensing modalities within the industrial wireless sensors industry over the coming decade. Industrial buyers favor modular form factors and intrinsically safe housings that slash installation labor by up to 40%. Vendors now embed edge analytics to rank alarm severity, reducing false positives and maintenance tickets.

Wi-Fi retained a 45.2% share due to its ubiquity in enterprise networks and alignment with IT security controls. Plants often deploy Wi-Fi in control rooms and indoor process areas where bandwidth enables high-definition video or advanced analytics streams. Yet LPWAN's 24.7% CAGR indicates shifting preferences toward kilometer-scale coverage with multi-year battery life, critical for mines and pipeline corridors.

WirelessHART stays entrenched in petrochemical sites because it overlays existing HART loops, safeguarding decades of capital investment. ISA100.11a appeals to deterministic control scenarios despite higher engineering expense. Bluetooth and Zigbee service short-range mobile worker and building automation use cases. 5G NR industrial slices debut in ultra-low latency motion control, yet ecosystem maturity will dictate adoption pace.

The Industrial Wireless Sensor Market is Segmented by Product Type (Temperature Sensor, Pressure Sensor, Gas Sensor, and More), Communication Protocol (WirelessHART, ISA100. 11a, and More), Power Source (Battery-Powered, Energy-Harvesting, and More), End-User Industry (Manufacturing, Oil and Gas, Energy and Power, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved a 34.8% revenue share in 2024, supported by sprawling oil pipelines, shale assets, and established brown-field factories embracing Industry 4.0 retrofits. U.S. policy spurs private 5G networks, and federal tax incentives for digital infrastructure accelerate deployments. Canadian miners deploy LoRaWAN over thousands of square kilometers to supervise autonomous haulage fleets, while Mexican maquiladoras adopt wireless nodes to enhance production traceability under nearshoring contracts.

Asia Pacific records the fastest 14.2% CAGR and will surpass North America before 2029. China targets 10,000 fully connected factories by 2027, requiring millions of sensors for process, environmental, and predictive functions. Local OEMs offer cost-optimized LPWAN devices, lowering entry barriers for tier-two manufacturers. Japanese automotive and electronics giants refine just-in-time workflows through edge-enabled sensors that spot quality drifts early.

Europe grows steadily as Industrie 4.0 policies and the EU Green Deal compel factories to audit energy and emissions. German process plants integrate WirelessHART with OPC UA gateways for holistic visibility. Nordic wind and solar farms blanket turbines with vibration and strain sensors to pre-empt mechanical faults under harsh climate loads. The continent maintains stringent cybersecurity mandates, elevating demand for IEC 62443-validated devices.

- ABB Ltd.

- Rockwell Automation Inc.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- STMicroelectronics N.V.

- Emerson Electric Co.

- General Electric Co.

- Texas Instruments Inc.

- NXP Semiconductors N.V.

- BAE Systems plc

- Yokogawa Electric Corp.

- Banner Engineering Corp.

- Phoenix Contact GmbH and Co. KG

- Advantech Co., Ltd.

- Cisco Systems, Inc.

- Analog Devices, Inc.

- TE Connectivity Ltd.

- Robert Bosch GmbH (Bosch Sensortec)

- Sensirion AG

- Endress+Hauser Group

- Hitachi Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Edge-to-Cloud analytics demand surge

- 4.2.2 Retrofit digitalization of brown-field plants

- 4.2.3 Low-power wide-area (LPWA) chipset price collapse

- 4.2.4 Shift to predictive maintenance service-models

- 4.2.5 Cybersecure sensor-to-cloud gateways (IEC 62443) uptake

- 4.2.6 Decarbonization mandates in hard-to-abate sectors

- 4.3 Market Restraints

- 4.3.1 Reliability concerns in RF-noisy industrial sites

- 4.3.2 Scarcity of OT-centric cybersecurity talent

- 4.3.3 Battery-life replacement OPEX in large-scale roll-outs

- 4.3.4 Fragmented protocol ecosystem slowing standards

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Temperature Sensor

- 5.1.2 Pressure Sensor

- 5.1.3 Flow Sensor

- 5.1.4 Gas Sensor

- 5.1.5 Humidity Sensor

- 5.1.6 Vibration Sensor

- 5.1.7 Level Sensor

- 5.1.8 Imaging Sensor

- 5.1.9 Biosensor

- 5.1.10 Other Product Types

- 5.2 By Communication Protocol

- 5.2.1 WirelessHART

- 5.2.2 ISA100.11a

- 5.2.3 Wi-Fi

- 5.2.4 Bluetooth / BLE

- 5.2.5 Zigbee

- 5.2.6 6LoWPAN / Thread

- 5.2.7 LPWAN (LoRa, Sigfox)

- 5.2.8 5G NR (Rel-17 Industrial)

- 5.3 By Power Source

- 5.3.1 Battery-Powered

- 5.3.2 Energy-Harvesting

- 5.3.3 Wired-Powered Gateways

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.1.1 Automotive

- 5.4.1.2 Food and Beverage

- 5.4.1.3 Chemicals

- 5.4.1.4 Pharmaceuticals

- 5.4.1.5 Electronics and Semiconductor

- 5.4.2 Oil and Gas

- 5.4.3 Energy and Power

- 5.4.4 Mining and Metals

- 5.4.5 Healthcare Facilities

- 5.4.6 Smart Buildings and Infrastructure

- 5.4.7 Other Industries

- 5.4.1 Manufacturing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Rockwell Automation Inc.

- 6.4.3 Honeywell International Inc.

- 6.4.4 Siemens AG

- 6.4.5 Schneider Electric SE

- 6.4.6 STMicroelectronics N.V.

- 6.4.7 Emerson Electric Co.

- 6.4.8 General Electric Co.

- 6.4.9 Texas Instruments Inc.

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 BAE Systems plc

- 6.4.12 Yokogawa Electric Corp.

- 6.4.13 Banner Engineering Corp.

- 6.4.14 Phoenix Contact GmbH and Co. KG

- 6.4.15 Advantech Co., Ltd.

- 6.4.16 Cisco Systems, Inc.

- 6.4.17 Analog Devices, Inc.

- 6.4.18 TE Connectivity Ltd.

- 6.4.19 Robert Bosch GmbH (Bosch Sensortec)

- 6.4.20 Sensirion AG

- 6.4.21 Endress+Hauser Group

- 6.4.22 Hitachi Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment