PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842512

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842512

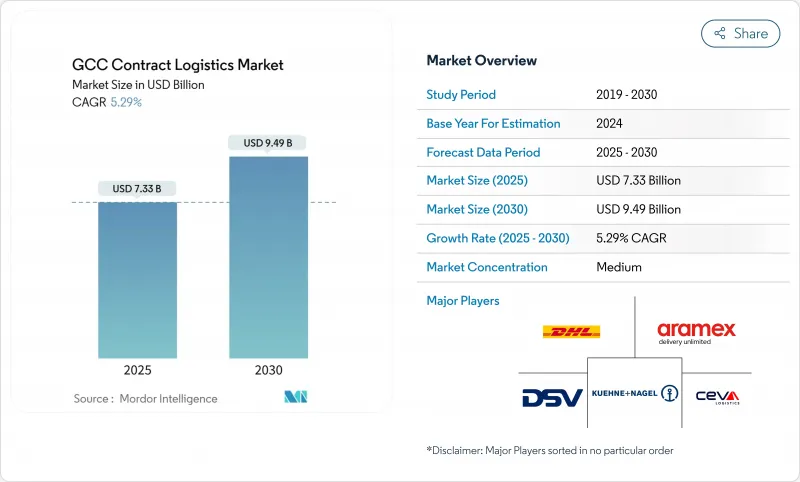

GCC Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The GCC Contract Logistics market stands at USD 7.33 billion in 2025 and is set to reach USD 9.49 billion by 2030, reflecting a 5.29% CAGR over the forecast period.

Regional governments are channeling record infrastructure spending into free trade zones, multimodal corridors, and digital trade platforms, positioning contract logistics as a cornerstone of diversified economic growth. Accelerating e-commerce, large-scale industrial projects under Saudi Vision 2030, and rising healthcare shipment volumes are amplifying demand for sophisticated fulfillment, cold-chain, and value-added services. Competitive intensity is increasing as global integrated logistics players add robotics and data-driven solutions while regional specialists leverage local knowledge to secure long-term partnerships. Despite strong momentum, cabotage rules and a chronic shortage of Grade-A warehouses continue to inflate operating costs and curb network optimization.

GCC Contract Logistics Market Trends and Insights

Rapid e-commerce fulfillment growth in KSA and UAE

Online orders in the MENA region climbed 30% in 2024, with the UAE's average order value moving from USD 30 to USD 35.6. Around 42% of e-commerce firms still list last-mile efficiency as the chief obstacle. Contract logistics providers are building regional fulfillment centers, adding parcel sortation automation, and integrating cross-border routing tools to cut delivery windows while controlling cost.

Vision 2030 industrial diversification projects require integrated logistics

Saudi Arabia approved USD 50 billion of projects under Vision 2030 in 2024 and earmarked funding for 59 national logistics centers. NIDLP allocates a further USD 36 billion for logistics infrastructure, plus USD 28 billion for industrial zones. These capital programs demand turnkey contract logistics capable of synchronized inbound, storage, and outbound flows. Operators embedded at project sites report rising localization targets, with 68% of companies prioritizing supply-chain localization for resilience.

Cabotage restrictions are hindering cross-border network optimization

Regional rules barring foreign tractors from domestic moves raise cross-border costs 18-23% and add 36 hours to multi-border transits. Temperature-sensitive cargo suffers most. Providers adopt hub-and-spoke models, yet still face double handling at borders. Regulatory harmonization lags physical links such as the Gulf Railway, muting potential productivity gains.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of free trade zones enhances warehousing demand

- Government-led cold-chain investment boosting temperature-controlled logistics

- Shortage of Grade-A warehousing is increasing operating costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Warehousing and distribution captured 47% of GCC Contract Logistics market share in 2024 on the back of the region's role as a crossroads between Asia, Europe, and Africa. GCC Ongoing investments include Saudi Arabia's USD 2.66 billion program to build 18 logistics zones by 2030. Robotics and high-bay automation are raising throughput and labor productivity, enabling faster cycle times that retailers and manufacturers demand. Yet limited Grade-A capacity still inflates costs for temperature-controlled storage, keeping barriers high for new entrants and supporting premium pricing.

Value-added services are projected to expand at 7.80% CAGR through 2030 as 3PLs bundle kitting, light assembly, and customization into comprehensive solutions. High-tech adoption drives this growth: DHL is deploying 1,000 additional Boston Dynamics robots after investing EUR 1 billion (USD 1.16 billion) in automation. Swisslog is promoting AutoStore robots that align with Saudi Vision 2030's innovation push. As clients pivot from transactional storage to integrated value chains, providers that integrate IT visibility, co-packing, and compliance support gain share.

The Gulf Cooperation Council (GCC) Contract Logistics Market Report is Segmented by Service (Transportation Management, Warehouse and Distribution and More), by End-User Industry (Consumer Goods and Retail and More), by Contract Duration (Short-Term and Long Term), and by Country (Saudi Arabia, United Arab Emirates, Qatar and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- DHL Supply Chain (Deutsche Post DHL Group)

- Aramex PJSC

- CEVA Logistics

- Kuehne + Nagel International AG

- DSV Solutions

- Yusen Logistics

- Gulf Warehousing Company (GWC)

- Al Futtaim Logistics

- Almajdouie Logistics

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Bahri Logistics

- FedEx Logistics

- UPS Supply Chain Solutions

- Gulf Agency Company (GAC)

- Mohebi Logistics

- Integrated National Logistics

- Hala Supply Chain Services

- GEODIS

- CJ Logistics Corporation

- SAL Saudi Logistics Services Co.

- NAQEL Express

- LogiPoint (Red Sea Gateway Logistics)

- RSA Global

- Kanoo Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid E-commerce Fulfillment Growth in KSA and UAE

- 4.2.2 Vision 2030 Industrial Diversification Projects Requiring Integrated Logistics

- 4.2.3 Expansion of Free Trade Zones Enhancing Warehousing Demand

- 4.2.4 Government-Led Cold-Chain Investment Boosting Temperature-Controlled Logistics

- 4.2.5 Gulf Railway Development Enabling Multimodal Contract Logistics

- 4.2.6 In-Country Value (ICV) Mandates Driving Outsourcing to Local 3PLs

- 4.3 Market Restraints

- 4.3.1 Cabotage Restrictions Hindering Cross-Border Network Optimization

- 4.3.2 Shortage of Grade-A Warehousing Increasing Operating Costs

- 4.3.3 Fragmented Customs Procedures Extending Lead Times

- 4.4 Value / Supply-Chain Analysis

- 4.5 Key Government Regulations and Initiatives

- 4.6 Technology Snapshot (IoT, AI, etc.)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitute Services

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

- 4.8 Insights on E-commerce Contract Logistics

- 4.9 Reverse Logistics / After-Sales Services

- 4.10 Spotlight on Freight Rates for Key Lanes

- 4.11 Insights on Free Trade Zones in GCC

- 4.12 Impact Analysis of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service

- 5.1.1 Transportation Management

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.2.1 Cold Chain/Temperature-Controlled

- 5.1.2.2 Non-Cold Chain/Non-Temperature-Controlled

- 5.1.3 Value-Added Services (Kitting, Packaging, Assembly, etc.)

- 5.1.1 Transportation Management

- 5.2 By End-User Industry

- 5.2.1 Manufacturing and Automotive

- 5.2.2 Consumer Goods and Retail (incl. E-commerce)

- 5.2.3 High-Tech and Electronics

- 5.2.4 Healthcare and Pharmaceuticals

- 5.2.5 Oil, Gas and Chemicals

- 5.2.6 Other End Users

- 5.3 By Contract Duration

- 5.3.1 Short-Term (Less Than 1 Year)

- 5.3.2 Long-Term (Greater than or equal to 1 Year)

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Oman

- 5.4.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain (Deutsche Post DHL Group)

- 6.4.2 Aramex PJSC

- 6.4.3 CEVA Logistics

- 6.4.4 Kuehne + Nagel International AG

- 6.4.5 DSV Solutions

- 6.4.6 Yusen Logistics

- 6.4.7 Gulf Warehousing Company (GWC)

- 6.4.8 Al Futtaim Logistics

- 6.4.9 Almajdouie Logistics

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 Rhenus Logistics

- 6.4.12 Bahri Logistics

- 6.4.13 FedEx Logistics

- 6.4.14 UPS Supply Chain Solutions

- 6.4.15 Gulf Agency Company (GAC)

- 6.4.16 Mohebi Logistics

- 6.4.17 Integrated National Logistics

- 6.4.18 Hala Supply Chain Services

- 6.4.19 GEODIS

- 6.4.20 CJ Logistics Corporation

- 6.4.21 SAL Saudi Logistics Services Co.

- 6.4.22 NAQEL Express

- 6.4.23 LogiPoint (Red Sea Gateway Logistics)

- 6.4.24 RSA Global

- 6.4.25 Kanoo Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment