PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842513

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842513

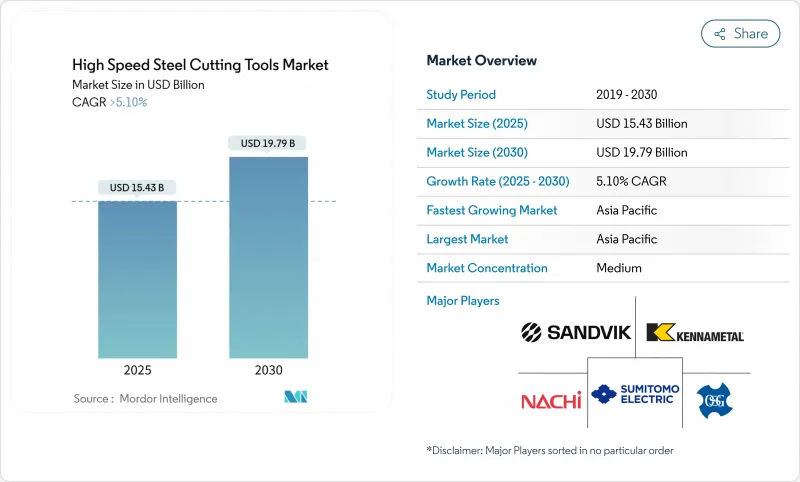

High Speed Steel Cutting Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The High Speed Steel Cutting Tools market size stands at USD 15.43 billion in 2025 and is on track to reach USD 19.79 billion by 2030, advancing at a 5.1% CAGR.

A resurgence of mid-volume machining, rapid industrialization in Asia, and wider use of powder metallurgy are the primary growth engines. Manufacturers are adopting cobalt-enriched grades for aerospace alloys, expanding e-commerce channels for DIY buyers, and refining adaptive CNC strategies that stretch tool life. Supply-side pressures remain, including volatile molybdenum and cobalt prices and the automotive sector's gradual pivot to carbide and PCD tools. Competitive moves center on targeted acquisitions, digital tool management, and carbon-neutral production commitments.

Global High Speed Steel Cutting Tools Market Trends and Insights

Demand for Low-cost Tooling in Emerging Asian Job Shops

Mounting numbers of tier-2 and tier-3 job shops across China, India, and ASEAN markets favor low initial tooling outlays. Conventional HSS tools meet that priority, especially as basic CNC adoption lets operators extend tool life by optimizing feeds and speeds. Chinese provincial support for indigenous machine-tool makers entrenches domestic sourcing, locking in repetitive demand cycles. The same trend spreads through India's automotive component clusters and Vietnam's electronics supply base, anchoring robust consumption for standard HSS milling cutters and drills.

DIY & Home-Improvement Retail Boom in North America

North American home-owners, hobbyists, and "prosumers" are driving double-digit online growth for consumer-grade HSS bits, taps, and hole saws. Tool makers now tailor geometries, coatings, and packaging to stand out on digital shelves, while power-tool brands bundle starter sets with cordless drills and compact lathes. Upskilled enthusiasts demanding industrial-style performance at modest price points have expanded the addressable segment, reinforcing the channel's 11.4% CAGR outlook.

Rapid Shift Toward Carbide & PCD Tools in Automotive

Electric vehicle platforms rely on thin-walled aluminum housings, composite brackets, and high-strength steel reinforcements. Carbide and PCD cutters deliver higher surface integrity and throughput on such materials, gradually displacing HSS in power-train, battery, and chassis lines. Automotive tooling decisions influence upstream tier suppliers and steel service centers, amplifying the drag on HSS demand, especially in Europe's high-volume plants.

Other drivers and restraints analyzed in the detailed report include:

- Re-shoring-led Adoption of Versatile HSS in North America & Europe

- Uptake of Cobalt-enriched M42 HSS for Aerospace Alloys

- Volatility in Molybdenum & Cobalt Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Milling cutters generated 32.4% of global 2024 revenue and anchor the High Speed Steel Cutting Tools market by virtue of their flexibility in face, slot, and profile machining. The segment benefits from continual refinement of radial chip thinning and high-efficiency roughing methods that raise metal-removal rates without compromising finish. Taps, in contrast, secure the quickest 6.8% CAGR through 2030 as thread-forming formats cut cycle times and avoid chip evacuation challenges. Chip-free threading aligns with automotive electronics housings and thin-section die-cast parts, pushing adoption across Asia and Eastern Europe.

Cost-sensitive job shops still prize HSS drills, reamers, and broaches for hole-making and finishing, while saws and countersinks meet niche needs in maintenance and repair. Digital design platforms now simulate chip flow, rake angle, and coolant delivery to customize cutting edges for each substrate. By leveraging such software, toolmakers unlock new shelf life even within standard HSS chemistries, reinforcing milling cutters' central role in the High Speed Steel Cutting Tools market.

Conventional M-series grades held 48% revenue share in 2024 thanks to broad availability and competitive pricing for mid-toughness jobs. Powder metallurgy variants command only 14.5% of output today, yet they capture disproportionate growth at 8.3% CAGR. Uniform carbide dispersion, refined grain boundaries, and reduced segregation give PM-HSS an edge when machining aerospace fasteners or medical implants where minimal chipping is critical. Cobalt-rich M42 and M35 maintain a strategic niche for heat-resistant alloys, bridging the cost gulf between PM and standard types.

The High Speed Steel Cutting Tools market size attached to PM-HSS is poised to expand as Europe resolves capacity gaps and as Asian players upscale domestic atomizing lines. Additive manufacturing trials also explore HSS powder blends with tailored hardness gradients, broadening future design possibilities and supporting long-term material-grade diversification across the High Speed Steel Cutting Tools market.

The High-Speed Steel Cutting Tools Market Report is Segmented by Tool Type (Drills and More), by Material Grade (Conventional HSS (M-Series) and More), by Production Process (Powder Metallurgy and More), by Distribution Channel (Direct OEM Sales and More), by End-User Industry (Oil & Gas and More) and by Geography (North America and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia leads the High Speed Steel Cutting Tools market with a 46.2% revenue share and a 6.3% CAGR forecast, thanks to China's electronics and machine-tool build-outs, India's automotive clusters, and Vietnamese assembly exports. Domestic tool makers now climb the value chain, adopting TiN and AlCrN coatings and pushing PM adoption, thereby reducing reliance on imports and cementing regional self-sufficiency.

North America ranks second and is revitalized by reshoring programs, defense offsets, and a thriving DIY culture. Hybrid machining cells in aerospace and energy plants require versatile cutters that thrive in adaptive CNC environments. E-commerce penetration also gives small workshops direct access to specialty taps and reamers, broadening High Speed Steel Cutting Tools market participation.

Europe sustains a technologically advanced yet capacity-constrained scenario. Limited PM-HSS supply elongates lead times for premium cutters. Nevertheless, German, French, and UK plants emphasize sustainable reconditioning and closed-loop recycling to hit carbon-reduction targets. Tool life monitoring and ISO 14001 programs elevate demand for data-rich HSS solutions despite carbide encroachment in automotive drivetrain lines.

South & Central America depend on Brazil's industrial base, while the Middle East leans on energy equipment refurbishment and ongoing infrastructure builds. Africa's demand cluster arises in South African mining supply and Egyptian component plants. Collectively, these emerging territories reflect the High Speed Steel Cutting Tools market's potential for diversification and localized value-add.

- Sandvik AB

- Kennametal Inc.

- OSG Corporation

- Sumitomo Electric Industries Ltd.

- Nachi-Fujikoshi Corp.

- Walter AG

- Erasteel SAS

- YG-1 Co. Ltd.

- Tiangong International Co. Ltd.

- Mitsubishi Materials Corp.

- Guhring KG

- Dormer Pramet

- Somta Tools (Pty) Ltd.

- Niagara Cutter LLC

- Arch Cutting Tools

- DeWALT (Stanley Black & Decker)

- Addison & Co. Ltd.

- Morse Cutting Tools

- Union Tool Co.

- Chongqing Zhengtai Tools

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Low-cost Tooling in Emerging Asian Job Shops

- 4.2.2 Re-shoring-led Adoption of Versatile HSS in North America & Europe

- 4.2.3 Uptake of Cobalt-enriched M42 HSS for Aerospace Alloys

- 4.2.4 DIY & Home-Improvement Retail Boom in North America

- 4.2.5 CNC-based Adaptive Machining Extending HSS Tool Life

- 4.3 Market Restraints

- 4.3.1 Volatility in Molybdenum & Cobalt Prices

- 4.3.2 Rapid Shift Toward Carbide & PCD Tools in Automotive

- 4.3.3 Carbon-neutrality-driven Tool-life Mandates

- 4.3.4 Limited European PM-HSS Capacity & Supply Bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Global Manufacturing Sector Outlook

- 4.8 Government Regulations Impacting Machining Industry

- 4.9 Steel Industry Snapshot

- 4.10 Technology Snapshot (Additive MFG, Nanocoatings)

- 4.11 Spotlight on Powder Metallurgy HSS

- 4.12 Insights on Tool Posts & Tool Holders

- 4.13 Sustainability & Circular-Economy Outlook

- 4.14 Global Disruptions and Supply Chain Resilience

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Tool Type

- 5.1.1 Milling Cutters

- 5.1.2 Drills

- 5.1.3 Taps

- 5.1.4 Reamers & Broaches

- 5.1.5 Others (Saws, Countersinks)

- 5.2 By Material Grade

- 5.2.1 Conventional HSS (M-Series)

- 5.2.2 High-Cobalt HSS (T-Series/M42/M35)

- 5.2.3 Powder-Metallurgy HSS (PM-HSS)

- 5.3 By Production Process

- 5.3.1 Conventional Forged

- 5.3.2 Powder Metallurgy

- 5.4 By Distribution Channel

- 5.4.1 Direct OEM Sales

- 5.4.2 Industrial Distributors

- 5.4.3 E-commerce/DIY Retail

- 5.5 By End-user Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Oil & Gas

- 5.5.3 Mining & Quarrying

- 5.5.4 Agriculture, Fishing & Forestry

- 5.5.5 Construction

- 5.5.6 Healthcare & Pharmaceutical

- 5.5.7 Energy Generation (Turbines & Nuclear)

- 5.5.8 Other End users (distributive trade, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves by Key Players in the Industry

- 6.2 Market Share Analysis (Key Players)

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Sandvik AB

- 6.3.2 Kennametal Inc.

- 6.3.3 OSG Corporation

- 6.3.4 Sumitomo Electric Industries Ltd.

- 6.3.5 Nachi-Fujikoshi Corp.

- 6.3.6 Walter AG

- 6.3.7 Erasteel SAS

- 6.3.8 YG-1 Co. Ltd.

- 6.3.9 Tiangong International Co. Ltd.

- 6.3.10 Mitsubishi Materials Corp.

- 6.3.11 Guhring KG

- 6.3.12 Dormer Pramet

- 6.3.13 Somta Tools (Pty) Ltd.

- 6.3.14 Niagara Cutter LLC

- 6.3.15 Arch Cutting Tools

- 6.3.16 DeWALT (Stanley Black & Decker)

- 6.3.17 Addison & Co. Ltd.

- 6.3.18 Morse Cutting Tools

- 6.3.19 Union Tool Co.

- 6.3.20 Chongqing Zhengtai Tools

7 Market Opportunities & Future Outlook