PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842570

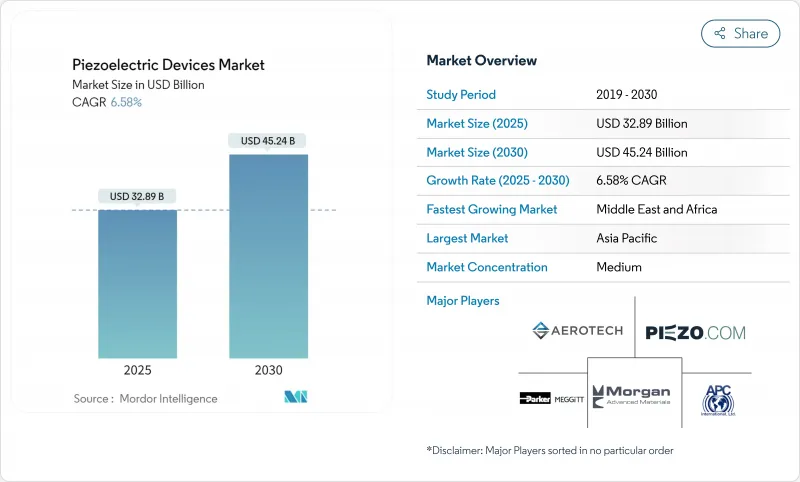

Piezoelectric Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The piezoelectric devices market size reached USD 32.9 billion in 2025 and is forecast to climb to USD 45.24 billion by 2030, reflecting a 6.58% CAGR.

Expansion stems from the miniaturization of 5G RF filters, rising automotive electrification, and Industry 4.0 retrofits that rely on robust, energy-efficient piezo components. The adoption of aluminum scandium nitride for bulk acoustic wave filters enables smartphone frequencies above 6 GHz, while the European Union's lead-free agenda accelerates the shift to potassium sodium niobate and bismuth sodium titanate despite their higher manufacturing costs. Asia-Pacific leads demand through large-scale consumer electronics output, and Middle East and Africa shows the fastest growth on oil-and-gas energy harvesting projects. Competitive intensity is moderate because vertically integrated suppliers such as TDK, Murata, and Kyocera secure upstream materials and downstream capacity, yet supply risks around niobium and lithium introduce volatility for defense and aerospace users.

Global Piezoelectric Devices Market Trends and Insights

Miniaturization of Piezo-MEMS RF Filters for 5G Smartphones (Asia)

Bulk acoustic wave filters built on aluminum scandium nitride now achieve frequencies above 6 GHz with coupling coefficients 40% higher than standard aluminum nitride, while maintaining thermal stability to 400 °C. These advances shrink die footprints to 0.83 X 0.75 mm2 and keep insertion losses below 1.5 dB, preserving smartphone battery life. Three-dimensional nanomechanical resonators further consolidate multiband functions onto single chips, creating scalable solutions for ultrawide-band connectivity. Asian wafer-level sealed silicon cavity platforms have achieved quality factors above 439, reducing production steps and cost. As 6G and millimeter-wave initiatives gather pace, demand rises for lithium niobate-based ultra-small filter chips, reinforcing Asia-Pacific's technology leadership.

Electrified Fuel-Injection and ADAS Piezo Actuators in European Premium Cars

Copper-electroded EPCOS multilayer actuators withstand more than 1 billion cycles at 170 °C, offering 20% performance gains over silver-palladium units while trimming material expenses. DENSO's i-ART system integrates microprocessors with piezo injectors to tailor fuel delivery in real time, enhancing engine efficiency under stricter emission norms.] Piezo sensors in semi-active suspension modules support magnetorheological dampers that raise ride comfort and stability for electrified platforms. Frame-type actuators transmit forces over 300 times higher than inertial models, giving advanced driver-assistance systems quicker mechanical response. Haptic feedback modules using PowerHap stacks now move 2 kg automotive displays with precise tactile cues that bolster human-machine interaction.

EU Lead-Free Directive Increasing Cost of PZT Substitutes

The Restriction of Hazardous Substances mandate propels the migration from PZT to lead-free ceramics that carry 15-20% higher production costs and complicate global supply strategies. KNN-based textured ceramics recently reached 550 pC/N piezo coefficients with less than 1.2% variability between 25 °C and 150 °C, making them competitive for performance-critical uses. Recycling methods that reclaim oxides via upside-down composite processing slash energy demand to 1% of virgin production and keep sensing quality intact. Manufacturers must maintain twin supply chains to serve PZT-dependent regions while scaling pristine lines for EU buyers, raising overheads. Cost differentials slow substitution in price-sensitive consumer electronics even as regulatory deadlines loom within two years.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Retrofit Demand for Piezo Sensors in United States Discrete Manufacturing

- Smart Ultrasonic Meter Roll-outs in South-Korea and China Utilities

- Price Volatility from Single-Source Niobium and Lithium Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensors captured 32.1% of piezoelectric devices market share in 2024, reflecting their cross-industry ubiquity in smartphones, vehicles, and industrial monitoring. Energy harvesters form the fastest-growing cohort at a 9.1% CAGR, aligned with self-powered IoT rollouts that favor maintenance-free nodes. Actuators and motors hold the second-largest slice by revenue, benefiting from EV adoption and precision manufacturing. Resonators see renewed traction as 5G deployment raises network synchronization requirements. The segment's acceleration mirrors break-throughs in piezoelectric nanogenerators that pair silicone rubber composites with power densities of 1.56 pW/cm2 under daily flexing. Hybrid devices now combine sensing, actuation, and harvesting within a single stack, offering compact solutions for autonomous robots. Generators embedded in floor tiles yield 249.6 mW under foot traffic at roughly USD 10.2 per tile, illustrating low-entry energy harvesting for smart buildings.

Demand convergence places upward pressure on high-temperature lead-free materials and low-cost polymer blends. Piezoelectric transformers boasting 88% conversion efficiency at 50 kHz enable RF-energy harvesting for distant sensor nodes As manufacturers integrate edge AI, noise-filtered measurements and two-way feedback loops become essential, preserving the centrality of sensing devices within the piezoelectric devices market.

Ceramics accounted for 67.4% of 2024 revenue, maintained by PZT's mature supply chain and high electromechanical coupling. Polymers, especially PVDF, are growing fastest at an 8.7% CAGR thanks to flexible wearables and biomedical implants. Single-crystal options deliver premium performance for aerospace and defense, while composite architectures merge disparate advantages. Wet-spun PVDF fibers now register 0.88 V outputs under 50 N compression with R2 = 0.996 linearity, extending utility into soft robotics.

MgSiN2 thin films with a 5.9 eV bandgap show converse coefficients of 2.3 pm/V, broadening piezo integration in nanoelectromechanical systems. Lead-free Ba0.85Ca0.15Ti0.9Zr0.1O3 ceramics top 650 pC/N while keeping Curie temperatures of 96.5 °C, addressing EU compliance without severe trade-offs. Y-doped ZnO exhibits an 8.5-fold output jump through carrier-concentration control, pushing oxide semiconductors toward filter and sensor roles. These parallel advances suggest the piezoelectric devices market will remain ceramic-centric yet increasingly diversified.

The Piezoelectric Devices Market Report is Segmented by Product Type (Actuators and Motors, Sensors, Transducers, and More), Material (Ceramics, Single-Crystal, Polymers, and More), Operating Mode (Compression/D33 Mode, Shear/D15 Mode, and More), End-User Industry (IT and Telecommunication, Consumer Electronics, Healthcare and Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.8% of global revenue in 2024, driven by scale advantages in handset assembly, automotive electrification, and fast 5G rollouts. China and South Korea advance smart ultrasonic meters and miniaturized RF filters, while Japan's Murata, TDK, and Kyocera channel deep ceramics expertise into higher-margin multilayer components. India and Southeast Asia attract sensor assembly for cost-sensitive goods, whereas Australia's mining firms deploy energy harvesting for asset monitoring. Rising labor costs spur automation investments, reinforcing premium piezo demand.

North America ranks second in value, underpinned by defense and aerospace programs that require hypersonic-grade ceramics. The Department of Defense earmarked SBIR 24.1 funds for additively manufactured textured piezo components, sparking domestic R&D. Canadian resource sites specify rugged harvesters for remote wells, and US chip fabs expand precision-stage adoption. Physik Instrumente opened a 120,000 sq ft Massachusetts plant to meet 30-50% annual US demand growth. Mexico's vehicle plants integrate piezo injectors and ADAS haptic modules, given supply chain proximity.

Europe leverages stringent environmental rules and luxury-car production to drive lead-free ceramics and next-gen actuators. German OEMs embed piezo suspensions and injectors; Nordic utilities incorporate grid sensors; France's aerospace sector demands high-temperature single crystals. The Middle East and Africa region posts the highest CAGR at 8.5% to 2030 as Gulf pipelines, smart cities, and solar parks deploy pipeline vibration harvesters and infrastructure flow meters. Supply diversification efforts in Africa could evolve into upstream material advantages over the forecast horizon.

- APC International, Ltd.

- Physik Instrumente (PI) GmbH and Co. KG

- Morgan Advanced Materials plc

- CTS Corporation (incl. Noliac)

- CeramTec GmbH

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Kyocera Corporation

- Piezotech S.A.S. (Arkema Group)

- Piezomechanik Dr. Lutz Pickelmann GmbH

- Piezosystem Jena GmbH

- Mad City Labs, Inc.

- Aerotech, Inc.

- Johnson Matthey Piezo Products GmbH

- Kistler Group

- Piezo.com (Meggitt PLC)

- Parker Hannifin - Meggitt Sensing

- Mide Technology (QinetiQ North America)

- TRS Technologies, Inc.

- Triumph Group - Transducer Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturization of Piezo-MEMS RF Filters for 5G Smartphones (Asia)

- 4.2.2 Electrified Fuel-Injection and ADAS Piezo Actuators in European Premium Cars

- 4.2.3 Industry 4.0 Retrofit Demand for Piezo Sensors in United States Discrete Manufacturing

- 4.2.4 Smart Ultrasonic Meter Roll-outs in South-Korea and China Utilities

- 4.2.5 Micro-Vibration Energy Harvesting for Remote Oil and Gas Pipelines (Middle East)

- 4.2.6 Federal Funding for Hypersonic-Grade Piezo Ceramics in United States Defense

- 4.3 Market Restraints

- 4.3.1 EU Lead-Free Directive Increasing Cost of PZT Substitutes

- 4.3.2 Price Volatility from Single-Source Niobium and Lithium Supply

- 4.3.3 Capital-Intensive Multi-Axis Stage Production Limiting SME Entry (JP/DE)

- 4.3.4 Temperature Limits of Polymer Piezo Films in Aero-engines

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Actuators and Motors

- 5.1.2 Sensors

- 5.1.3 Transducers

- 5.1.4 Generators

- 5.1.5 Energy Harvesters

- 5.1.6 Resonators

- 5.2 By Material

- 5.2.1 Ceramics

- 5.2.2 Single-Crystal

- 5.2.3 Polymers (e.g., PVDF)

- 5.2.4 Composites/Others

- 5.3 By Operating Mode

- 5.3.1 Compression/d33 Mode

- 5.3.2 Shear/d15 Mode

- 5.3.3 Bending/d31 Mode

- 5.3.4 Thickness-Mode Ultrasonic

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunication

- 5.4.2 Consumer Electronics

- 5.4.3 Manufacturing and Industrial Automation

- 5.4.4 Automotive and Transportation

- 5.4.5 Healthcare and Medical Devices

- 5.4.6 Aerospace and Defense

- 5.4.7 Energy and Utilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, Tech-Licensing)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 APC International, Ltd.

- 6.4.2 Physik Instrumente (PI) GmbH and Co. KG

- 6.4.3 Morgan Advanced Materials plc

- 6.4.4 CTS Corporation (incl. Noliac)

- 6.4.5 CeramTec GmbH

- 6.4.6 TDK Corporation

- 6.4.7 Murata Manufacturing Co., Ltd.

- 6.4.8 Kyocera Corporation

- 6.4.9 Piezotech S.A.S. (Arkema Group)

- 6.4.10 Piezomechanik Dr. Lutz Pickelmann GmbH

- 6.4.11 Piezosystem Jena GmbH

- 6.4.12 Mad City Labs, Inc.

- 6.4.13 Aerotech, Inc.

- 6.4.14 Johnson Matthey Piezo Products GmbH

- 6.4.15 Kistler Group

- 6.4.16 Piezo.com (Meggitt PLC)

- 6.4.17 Parker Hannifin - Meggitt Sensing

- 6.4.18 Mide Technology (QinetiQ North America)

- 6.4.19 TRS Technologies, Inc.

- 6.4.20 Triumph Group - Transducer Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment