PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842581

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842581

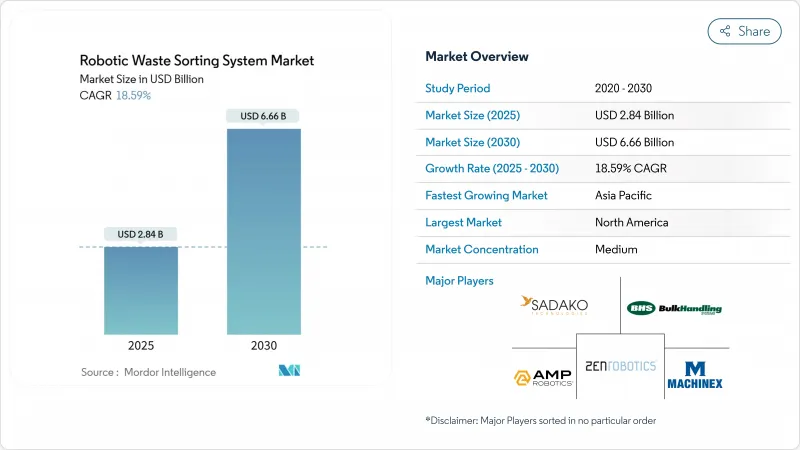

Robotic Waste Sorting System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The robotic waste sorting system market size stood at USD 2.84 billion in 2025 and is projected to reach USD 6.66 billion by 2030, reflecting an 18.59% CAGR during the forecast period.

Growth momentum in the robotic waste sorting system market is driven by tightening landfill-diversion rules, producer responsibility mandates, and sustained investment in artificial-intelligence hardware. Automated sorting has become a strategic response to labor scarcity at Material Recovery Facilities (MRFs) and to China's restrictions on low-grade imports, both of which have raised the value of high-purity recyclables. Rapid improvements in multi-sensor fusion now allow robots to recognize more than 500 waste categories with 99% accuracy, lifting recovery rates and lowering residual disposal fees. Service-based leasing is gaining traction, easing capital constraints, while cybersecurity spending is rising as interconnected fleets expose facilities to industrial control threats. As a result, the robotic waste sorting system market continues to shift from pilot projects to core infrastructure investment strategies across advanced economies.

Global Robotic Waste Sorting System Market Trends and Insights

Stricter Landfill Diversion and EPR Regulations

Extended Producer Responsibility rules shift cost burdens from municipalities to brand owners, and the EU's 2024 packaging measure requires all packaging to be recyclable and to hit specific recycled-content thresholds by 2030 and 2040, accelerating automation adoption. Municipalities and producers now deploy robots to secure higher material purity and avoid EPR penalties. The OECD notes that variable EPR fees reward companies that design recyclable products, which further sharpens demand for precision sortation. Facilities deploying robotic systems report recovery-rate jumps of 20 percentage points within 12 months of commissioning. These returns strengthen the robotic waste sorting system market as new regional mandates replicate the EU model.

Ban on Low-Grade Waste Imports by China and Others

China's National Sword policy requires sub-0.5% contamination, forcing Western MRFs to upgrade equipment to regain export revenue. Robots provide the accuracy needed to meet the new quality bar, and payback periods have fallen to under 24 months in high-volume plants. Similar bans in Malaysia, Thailand, and Vietnam magnify the driver. Consequently, the robotic waste sorting system market has realigned toward domestic capacity investment, with North American operators adding AI sorters at mixed-plastic lines to recapture commodity margins lost after 2018.

High Capex and Payback Uncertainty

Complete robotic lines cost USD 2-5 million, equal to 8-12 months of revenue for a 100,000-tonne MRF. Commodity-price swings elongate payback, delaying investment in emerging markets. Leasing and Robotics-as-a-Service (RaaS) are mitigating this restraint by shifting spending from capex to opex, yet access to dollar-denominated leases remains limited outside developed economies. The robotic waste sorting system industry therefore advances unevenly across regions with different capital-access profiles.

Other drivers and restraints analyzed in the detailed report include:

- Labor Shortages and Rising MRF Operating Costs

- Surge in Recycled-Content Packaging Mandates

- Cyber-Security Exposure of IIoT Robots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Municipal MRFs managed 38.5% of the robotic waste sorting system market in 2024, reflecting the largest installed base and the highest mix-waste volumes. As these plants target contamination thresholds below 1%, managers install AI robots on residual lines to boost purity and reduce landfill levies. The robotic waste sorting system market size for Municipal MRFs is projected to grow at a steady 15% CAGR through 2030, supported by state-level funding programs in the United States and provincial grants in Canada.

Plastic Re-processors, while smaller in absolute terms, are accelerating at 21.4% CAGR. The segment captures demand from consumer-packaged-goods brands pursuing closed-loop strategies. Robots specialize in polymer separation, extracting color-sorted PET and HDPE that command price premiums of up to 30% over mixed-bale equivalents. As a result, Plastic Re-processors are expected to hold a 22% robotic waste sorting system market share by 2030, narrowing the gap with Municipal MRFs.

Plastics accounted for 39% of revenue in 2024 and continue to exhibit the fastest uptake. AI systems now identify multilayer films and colored PET with near-laboratory precision. In value-chain terms, each percentage-point reduction in plastic bale contamination lifts resale prices by USD 25 per tonne, supporting investment cases. Paper and cardboard remain a stable category as optical scanners adjust for ink and residue. Metals enjoy robust capture using eddy currents, yet robots add value by isolating high-grade aluminum alloys. Glass sorting gains from AI color-detection models that lift recovery from 70% to 85% in Scandinavian plants.

The robotic waste sorting system market size for plastics alone is projected to exceed USD 2.6 billion by 2030, equal to 39% of global value. Robots' ability to sort complex resins positions the segment for sustained double-digit expansion.

Robotic Waste Sorting System Market is Segmented by End-Use Facility (Municipal MRFs, Industrial and Commercial Recycling Plants, and More), Waste Type Sorted (Plastics, Paper and Cardboard, and More), Component (Hardware, Software, Services), Sorting Technology (AI Vision-Only, NIR / Hyperspectral Optical, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 33% of global revenue in 2024, with early robot adopters scaling fleets to offset labor churn and to hit recycling-rate mandates in California, Oregon, and Colorado. Waste Management alone invested USD 1.4 billion in AI-enabled facilities between 2024 and early 2025. The region hosts over 400 AMP Robotics units, and robotic waste sorting system market size in the United States is projected to exceed USD 2 billion by 2030.

Asia-Pacific is the fastest-growing region at 18.7% CAGR. China's domestic policy pivot from importer to recycler triggered a surge in capacity adds, including ZenRobotics construction-waste lines in Shanghai. Japan's municipal plants deploy AI glass sorters that lift recovery rates for amber and flint cullet, supporting the country's bottle-to-bottle targets. South Korea's ATron robots demonstrate 99.3% precision and showcase export potential across ASEAN. Consequently, Asia-Pacific's share of the robotic waste sorting system market is forecast to rise from 27% in 2025 to 33% in 2030.

Europe benefits from mature EPR regulations that fund capital investment. Denmark's autonomous construction-waste plant achieves 98% purity for recycled aggregates, setting new circular-economy benchmarks. Spain's first AI sorting initiative under Urbaser signals wider Iberian adoption. Although growth is steadier than in Asia-Pacific, the region remains a technology test bed, sustaining a high concentration of pilot projects and patents that inform global standards for the robotic waste sorting system market.

- AMP Robotics Corporation

- ZenRobotics Ltd

- TOMRA Systems ASA

- Bulk Handling Systems (BHS)

- Machinex Industries Inc

- Waste Robotics Inc

- Sadako Technologies

- General Kinematics

- Pellenc ST

- Green Machine LLC

- STADLER Anlagenbau

- Bollegraaf Group

- Everest Labs

- Glacier AI

- Greyparrot

- JONO Environmental

- FANUC Corp.

- ABB Ltd.

- KUKA AG

- SUEZ Group (AI sorting JV)

- Veolia Environnement (robotic pilots)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter landfill diversion and EPR regulations

- 4.2.2 Ban on low-grade waste imports by China and others

- 4.2.3 Labour shortages and rising MRF operating costs

- 4.2.4 Surge in recycled-content packaging mandates

- 4.2.5 Demand for AI-enabled closed-loop data (under-reported)

- 4.2.6 OEM service-based robot leasing models (under-reported)

- 4.3 Market Restraints

- 4.3.1 High capex and payback uncertainty

- 4.3.2 Limited technical talent for OandM

- 4.3.3 Volatile secondary-commodity prices

- 4.3.4 Cyber-security exposure of IIoT robots (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End-use Facility

- 5.1.1 Municipal MRFs

- 5.1.2 Industrial and Commercial Recycling Plants

- 5.1.3 Construction and Demolition Facilities

- 5.1.4 Plastic Re-processors

- 5.1.5 E-waste Recyclers

- 5.2 By Waste Type Sorted

- 5.2.1 Plastics

- 5.2.2 Paper and Cardboard

- 5.2.3 Metals

- 5.2.4 Glass

- 5.2.5 Organic and Food Waste

- 5.2.6 Mixed CandD Debris

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services (Installation, OandM, Leasing)

- 5.4 By Sorting Technology

- 5.4.1 AI Vision-only

- 5.4.2 NIR / Hyperspectral Optical

- 5.4.3 3-D Laser and X-ray

- 5.4.4 Hybrid Multi-Sensor

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 ASEAN-6

- 5.5.4.7 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMP Robotics Corporation

- 6.4.2 ZenRobotics Ltd

- 6.4.3 TOMRA Systems ASA

- 6.4.4 Bulk Handling Systems (BHS)

- 6.4.5 Machinex Industries Inc

- 6.4.6 Waste Robotics Inc

- 6.4.7 Sadako Technologies

- 6.4.8 General Kinematics

- 6.4.9 Pellenc ST

- 6.4.10 Green Machine LLC

- 6.4.11 STADLER Anlagenbau

- 6.4.12 Bollegraaf Group

- 6.4.13 Everest Labs

- 6.4.14 Glacier AI

- 6.4.15 Greyparrot

- 6.4.16 JONO Environmental

- 6.4.17 FANUC Corp.

- 6.4.18 ABB Ltd.

- 6.4.19 KUKA AG

- 6.4.20 SUEZ Group (AI sorting JV)

- 6.4.21 Veolia Environnement (robotic pilots)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment