PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842596

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842596

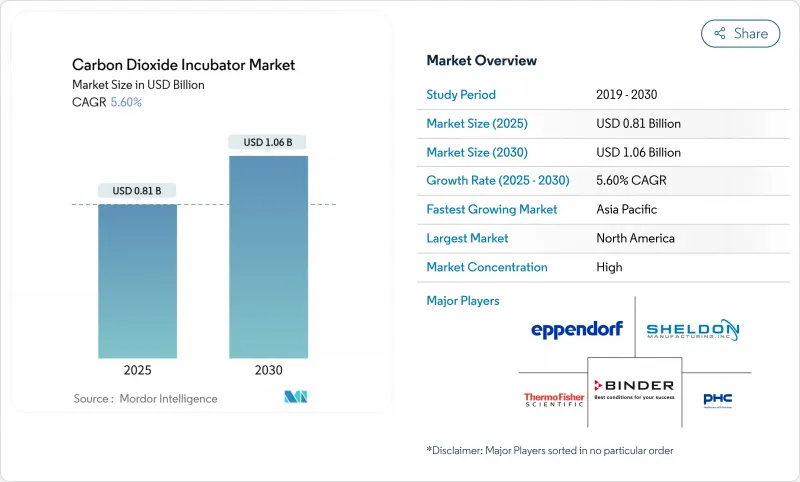

Carbon Dioxide Incubator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The CO2 incubator market stands at USD 808.36 million in 2024 and is projected to reach USD 1,061.51 million by 2030, advancing at a 5.6% CAGR.

Consistent expansion in cell and gene therapy pipelines, tighter contamination-control regulations, and laboratory automation initiatives sustain demand even in budget-constrained academic settings. Higher biopharmaceutical R&D outlays, the move toward allogeneic cell-therapy manufacturing, and energy-efficiency rules that favor direct-heat designs further reinforce the growth outlook. Multinational suppliers respond with advanced sensors, remote monitoring, and AI-ready interfaces that align with self-driving laboratory concepts. Regional momentum differs: mature North American facilities focus on upgrade cycles while fast-growing Asian sites add first-time capacities, collectively shaping the CO2 incubator market trajectory.

Global Carbon Dioxide Incubator Market Trends and Insights

Rising Demand for Cell & Gene-Therapy Process Development

Escalating therapy pipelines in oncology and rare diseases raise the need for incubation environments that guarantee tight temperature and gas uniformity. Sartorius projects biopharma growth near 10% CAGR for 2024-2028, with cell and gene therapies outpacing traditional biologics. As programs transition from autologous to allogeneic formats, batch sizes increase, driving procurement of larger, contamination-free chambers. Manufacturers embed traceability software to satisfy evolving GMP-level documentation. The CO2 incubator market thereby gains recurring demand from both development and commercial-scale facilities.

Surge in Biopharma R&D Expenditure Worldwide

Despite selective funding headwinds, global R&D pipelines remain robust, and major suppliers continue to post multibillion-dollar revenues. Thermo Fisher reported USD 10.36 billion in Q1 2025, underscoring sustained purchasing power among commercial labs. Higher spending priorities include automation platforms and connected equipment, prompting incubator designs that transmit real-time performance data. AI-enabled monitoring reduces manual checks, helping laboratories meet throughput goals while maintaining compliance.

High Capital & Maintenance Costs of Advanced Units

Leading models integrate UV sterilization, HEPA filtration, and IoT-ready sensors, raising list prices and service contracts. Bio-Rad cited softer instrument demand from academia in Q1 2025, linking slower upgrades to limited grant cycles. Energy-efficiency redesigns, required under new DOE rules effective 2029, also inflate manufacturing expenses. Smaller facilities defer purchases, stretching replacement timelines.

Other drivers and restraints analyzed in the detailed report include:

- Growing Global IVF Procedure Volumes

- Expansion of Cell-Based Vaccine Manufacturing

- Persistent Contamination-Risk Perception Among Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-jacketed systems captured 45.45% of the CO2 incubator market in 2024 thanks to unmatched thermal inertia that protects sensitive cultures during door openings. Yet energy-focused procurement policies spur rising preference for direct-heat units, projected to grow 6.23% annually through 2030 as laboratories prioritize lower running costs and simpler upkeep. Upcoming U.S. energy-conservation standards, set for compliance in 2029, will likely speed conversion to direct-heat architecture .

Direct-heat models eliminate water reservoirs, reducing contamination vectors and downtime. Suppliers now integrate adaptive PID controls and miniaturized ScAlN-based CO2 sensors that improve recovery times. Tri-gas variants also register accelerating demand for hypoxic research. Portfolio breadth positions vendors to upsell accessories and service plans, reinforcing the CO2 incubator market growth path.

Chambers between 100 L and 200 L yielded 41.23% of 2024 revenue, confirming their sweet spot between sample throughput and lab-space economics. This segment benefits from retrofits in existing pharmaceutical suites, where infrastructure constraints limit adoption of larger formats. Units below 100 L, however, represent the fastest expanding niche at a 6.89% CAGR, reflecting the proliferation of precision-medicine and point-of-care workflows that require localized, small-batch culture environments.

Automation pushes capacity selection toward modularity. Self-driving laboratory prototypes reveal how multiple compact incubators can operate in parallel, trading volume for flexibility while feeding robotic handlers. As a result, the CO2 incubator market size for sub-100 L systems could widen beyond traditional academic demand into hospital and diagnostics settings. Vendors answer with stackable footprints and cloud dashboards that balance productivity and footprint.

The Carbon Dioxide Incubators Market Report Segments Into by Product Type (Water Jacketed CO2 Incubators, Air Jacketed CO2 Incubators and More), by Capacity (less Than 100 L, 100-200 L and More), by Application (Pharmaceutical & Biotechnology Companies, Contract Development & Manufacturing Organisations (CDMOs)), and by Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 38.89% of 2024 revenue, reflecting deep biopharmaceutical supply chains, well-funded universities, and early adoption of energy-efficient retrofits. Replacement demand dominates, with buyers trading older water-jacketed units for direct-heat models that meet forthcoming DOE standards. Service networks and aftermarket parts availability further cement vendor positions.

Europe retains a sizable share through strict contamination-control rules and sustainability directives. The 2024 EU ecodesign regulation mandates durability and repairability criteria, nudging buyers toward premium models with documented lifecycle assessments. Pharmaceutical clusters in Germany, Ireland, and Scandinavia anchor recurring demand, while government grants encourage deployment of smart sensors for energy tracking.

Asia-Pacific shows the sharpest trajectory at 7.45% CAGR as China, India, and South-East Asia scale biologics manufacturing and fertility clinics. Lower labor costs attract CDMO facilities that install large fleets of incubators, favouring suppliers with regional service centers. Local regulations increasingly mirror Western GMP norms, accelerating adoption of single-use interiors and advanced decontamination functions. Combined, these dynamics reinforce the CO2 incubator market momentum across emerging economies.

- Thermo Fisher Scientific

- Eppendorf

- Panasonic Healthcare Co., Ltd. (PHC)

- Binder

- Sheldon Manufacturing Inc. (Shellab)

- NuAire Inc.

- Memmert

- LEEC

- Esco Micro Pte. Ltd.

- MMM Medcenter Einrichtungen GmbH

- Caron Products & Services Inc.

- Labogene ApS

- Heal Force Bio-Medical Co. Ltd.

- Benchmark Scientific

- Taicang Hou Waining Laboratory Equipment

- Thomas Scientific LLC

- Labocon Systems Ltd.

- SANYO Electric Biomedical Co. Ltd.

- Stericox Sterilizer & Autoclave

- BIOBASE Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for cell & gene-therapy process development

- 4.2.2 Surge in biopharma R&D expenditure worldwide

- 4.2.3 Growing global IVF procedure volumes

- 4.2.4 Expansion of cell-based vaccine manufacturing

- 4.2.5 Shift toward automated micro-incubators for HT screening

- 4.2.6 Regulatory push for single-use, contamination-free chambers

- 4.3 Market Restraints

- 4.3.1 High capital & maintenance costs of advanced units

- 4.3.2 Persistent contamination-risk perception among labs

- 4.3.3 Stringent energy-efficiency directives for legacy models

- 4.3.4 Supply-chain dependence on specialty CO2 sensors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD Million)

- 5.1 By Product Type

- 5.1.1 Water-Jacketed CO2 Incubator

- 5.1.2 Air-Jacketed CO2 Incubator

- 5.1.3 Direct-Heat CO2 Incubator

- 5.1.4 Multi-Gas (Tri-Gas) Incubator

- 5.1.5 Portable / Benchtop Incubator

- 5.1.6 Customized & Other Types

- 5.2 By Capacity

- 5.2.1 Less than 100 L

- 5.2.2 100 - 200 L

- 5.2.3 More than 200 L

- 5.3 By Application

- 5.3.1 Cell & Tissue Culture

- 5.3.2 Stem-Cell Research

- 5.3.3 Cancer & Immunology Research

- 5.3.4 In-Vitro Fertilisation (IVF)

- 5.3.5 Microbiology & Diagnostics

- 5.3.6 Other Emerging Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Development & Manufacturing Organisations (CDMOs)

- 5.4.3 Research & Academic Institutes

- 5.4.4 Clinical & IVF Laboratories

- 5.4.5 Food-Testing & Environmental Labs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Eppendorf SE

- 6.3.3 Panasonic Healthcare Co., Ltd. (PHC)

- 6.3.4 Binder GmbH

- 6.3.5 Sheldon Manufacturing Inc. (Shellab)

- 6.3.6 NuAire Inc.

- 6.3.7 Memmert GmbH + Co. KG

- 6.3.8 LEEC Ltd.

- 6.3.9 Esco Micro Pte. Ltd.

- 6.3.10 MMM Medcenter Einrichtungen GmbH

- 6.3.11 Caron Products & Services Inc.

- 6.3.12 Labogene ApS

- 6.3.13 Heal Force Bio-Medical Co. Ltd.

- 6.3.14 Benchmark Scientific Inc.

- 6.3.15 Taicang Hou Waining Laboratory Equipment

- 6.3.16 Thomas Scientific LLC

- 6.3.17 Labocon Systems Ltd.

- 6.3.18 SANYO Electric Biomedical Co. Ltd.

- 6.3.19 Stericox Sterilizer & Autoclave

- 6.3.20 BIOBASE Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment