PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842599

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842599

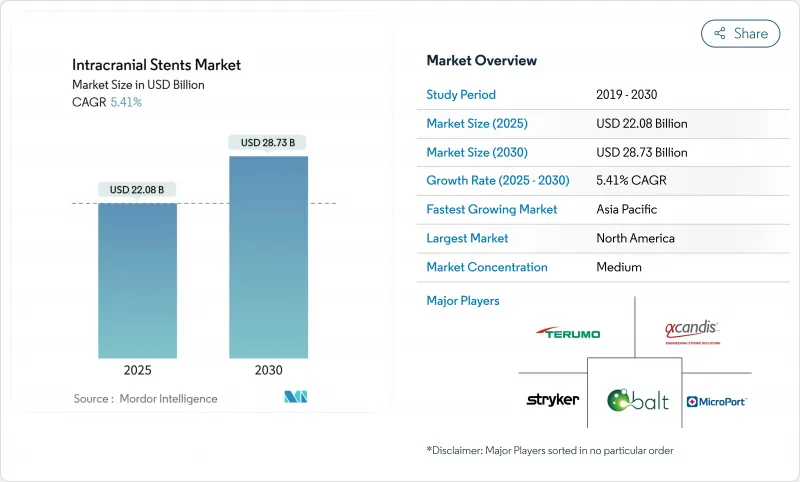

Intracranial Stents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The intracranial stents market stands at USD 22.08 billion in 2025 and is forecast to reach USD 28.73 billion by 2030, advancing at a 5.41% CAGR.

Uptake is propelled by an aging population, steady gains in flow-diversion technology, and wider reimbursement that collectively expand candidacy for minimally invasive neurovascular care.Flow-diverter breakthroughs now let physicians treat aneurysms once deemed inoperable while shortening procedural steps, a change that is reshaping everyday practice. Artificial-intelligence guidance, growing self-expanding stent familiarity, and coating innovations further raise success rates and lower complication profiles. At the same time, stroke-center accreditations and outpatient migration are leaning the market toward capacity-optimized, technology-enabled growth, especially in Asia-Pacific where infrastructure projects are accelerating.

Global Intracranial Stents Market Trends and Insights

Increasing Demand for Minimally Invasive Intracranial Procedures

Radial-access approaches now dominate current training modules because they lower vascular complication rates and trim recovery times without undermining procedural safety. Flow-diverting stents exemplify this change by replacing multi-stage coil embolization with single-device deployment, reducing catheter time and radiation exposure. Certification of thrombectomy-capable stroke centers in the United States is cementing standardized use, and the same-day-discharge model inside ambulatory surgery centers aligns perfectly with value-based payment initiatives.

Growing Prevalence of Cerebrovascular Disorder & Aging Demographics

Population aging raises the baseline incidence of aneurysms and intracranial stenosis, expanding the global candidate pool for stenting frontiersin.org. AI-imaging tools now detect silent aneurysms earlier, while five-year occlusion rates of 96% for flow-diverters confirm durable performance and reinforce broader guidelines jnis.bmj.com. In China, 25,438 patients were enrolled for unruptured aneurysm care, with 73.6% managed endovascularly, illustrating huge latent demand.

Scarcity of Highly-Skilled Neuro-Interventionalists

Training demands of 250 cumulative cases, including 25 stent placements, slow workforce expansion and leave many secondary hospitals understaffed. High-volume hubs such as Penn Medicine handle over 2,000 interventions annually, but talent remains clustered in urban centers, leading to access disparities for rural or frontier markets. AI guidance may ease skill gaps, yet large randomized trials and regulatory review are still pending.

Other drivers and restraints analyzed in the detailed report include:

- Improving Healthcare Infrastructure and Expanding Reimbursement Coverage

- Technological Advancement and Product Innovation

- Post-Procedural In-Stent Restenosis & Thrombosis Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The intracranial stents market size for flow-diverters is projected to expand at 9.12% CAGR between 2025-2030, reflecting strong physician preference for single-device aneurysm occlusion and reduced retreatment burden. Self-expanding devices nevertheless control 45.25% 2024 volume thanks to their broad indication list and operator familiarity.

Fourth-generation flow-diverters such as Pipeline Vantage now achieve 81.7% six-month occlusion, while hydrophilic coatings have lowered thromboembolic complications to 4.7%, narrowing the safety gap with coils. Balloon-expandable models retain niche roles in tortuous pediatric cases where exact placement is critical, and stent-assisted coils continue to bridge practice for operators transitioning toward full flow diversion.

Nitinol-based devices accounted for 59.15% of the intracranial stents market share in 2024, benefiting from shape-memory reliability and long clinical track records. Yet polymer and bioresorbable alternatives are growing at 8.56% CAGR as surgeons aim to avoid lifelong metal in young or low-risk patients.

Iron-based resorbables are undergoing corrosion-rate optimization, while polydioxanone scaffolds from cardiovascular trials provide proof of two-month support before safe dissolution. Cobalt-chromium remains favored for visualization in complex reconstructions. This material shift adds new procurement questions for providers weighing up-front cost versus lifetime risk mitigation.

The Intracranial Stents Market Report is Segmented by Type (Self-Expanding Stents, Balloon Expanding Stents, and More), Material (Nitinol, Cobalt-Chromium and More), Application (Intracranial Stenosis, Brain Aneurysm and More), End-User (Hospitals, Ambulatory Surgery Centers and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the intracranial stents market in 2024 with 36.34% revenue, anchored by comprehensive stroke-center networks, favorable reimbursement, and a robust fellowship pipeline that supplies skilled operators. Device manufacturers often pilot next-generation coatings and AI software in United States or Canadian centers before global roll-out, accelerating domestic adoption cycles.

Europe maintains steady growth through regulatory harmonization and cross-border clinical trials such as the COATING study, which evaluates polymer-coated flow-diverters across multiple countries. National health systems in Germany, France, and the Nordic region have also upgraded stroke guidelines to include flow-diversion for complex aneurysms, securing reimbursement faster than past device classes.

Asia-Pacific is the fastest-growing region at 8.01% CAGR, propelled by public investment in stroke centers and a large untreated aneurysm population. The China Treatment Trial for Unruptured Intracranial Aneurysm highlights demand scale, enrolling over 25,000 patients with an endovascular treatment rate above 70%. India and Indonesia follow with capacity pledges for new neuro-cath labs, while Japan and South Korea serve as early adopters of polymer-coated stents due to national reimbursement clarity.

The Middle East and Africa are at an earlier adoption curve but benefit from medical-city initiatives in Saudi Arabia and United Arab Emirates that import high-end imaging suites and training partnerships. South America shows dual-speed dynamics: Brazil and Colombia grow quickly under private-payer segments, while smaller economies lag amid budget constraints.

- Wallaby Medical

- Stryker

- Terumo Corp.

- MicroPort

- Acandis

- Balt Group

- Phenox

- Medtronic

- Rapid Medical

- InspireMD

- Boston Scientific

- TonBridge Medical

- Lepu Medical Technology(Beijing)Co.,Ltd

- Sino Medical Sciences Technology Inc.

- Contego Medical, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Minimally-Invasive Intracranial Procedures

- 4.2.2 Growing Prevalence of Cerebrovascular Disorder & Ageing Demographics

- 4.2.3 Improving Healthcare Infrastructure and Expanding Reimbursement Coverage

- 4.2.4 Technological Advancement and Product Innovation

- 4.2.5 Growing Awareness and Early Diagnosis of Neurovascular Disorders

- 4.2.6 AI-Guided Neuro-Interventional Planning Improving Treatment Candidacy

- 4.3 Market Restraints

- 4.3.1 Scarcity Of Highly-Skilled Neuro-Interventionalists

- 4.3.2 Post-Procedural In-Stent Restenosis & Thrombosis Risk

- 4.3.3 Cost-Containment Pressures In Emerging Public Health Systems

- 4.3.4 Limited Long-Term Clinical Evidence For Next-Gen Bio-Resorbable Designs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Type

- 5.1.1 Self-expanding Stents

- 5.1.2 Balloon-expanding Stents

- 5.1.3 Stent-assisted Coil Embolization Systems

- 5.1.4 Flow-diverter Stents

- 5.2 By Material

- 5.2.1 Nitinol

- 5.2.2 Cobalt-Chromium

- 5.2.3 Polymer / Bioresorbable

- 5.3 By Application

- 5.3.1 Intracranial Stenosis

- 5.3.2 Brain Aneurysm

- 5.3.3 Arterio-Venous Malformation (AVM)

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Specialty Neurology Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Wallaby Medical

- 6.3.2 Stryker Corp.

- 6.3.3 Terumo Corp.

- 6.3.4 MicroPort Scientific

- 6.3.5 Acandis GmbH

- 6.3.6 Balt Group

- 6.3.7 phenox GmbH

- 6.3.8 Medtronic plc

- 6.3.9 Rapid Medical

- 6.3.10 InspireMD

- 6.3.11 Boston Scientific Corporation

- 6.3.12 TonBridge Medical

- 6.3.13 Lepu Medical Technology(Beijing)Co.,Ltd

- 6.3.14 Sino Medical Sciences Technology Inc.

- 6.3.15 Contego Medical, Inc

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment