PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842629

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842629

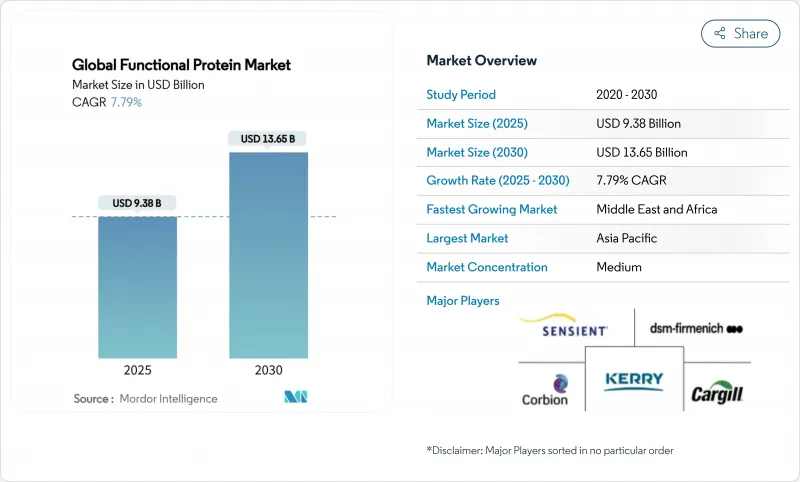

Global Functional Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The functional protein ingredients market has a market size of USD 9.38 billion in 2025 and is projected to expand to USD 13.65 billion by 2030, representing a compound annual growth rate (CAGR) of 7.79%.

The functional protein market growth reflects the intersection of health-conscious consumer behavior, regulatory modernization, and technological advancements in protein extraction and processing. The market demonstrates stability through its diverse applications across food and beverages, supplements, animal nutrition, and cosmetics sectors. Key developments in the protein ingredients industry include the regulatory approval of precision fermentation technologies, exemplified by Perfect Day's collaboration with Zydus Lifesciences to establish fermentation facilities in India. The FDA's elimination of the self-affirmed GRAS pathway indicates increased regulatory oversight, requiring manufacturers to pursue formal approval processes. The increasing demand for plant-based and alternative protein sources has accelerated research and development initiatives in the functional protein space. Additionally, manufacturers are investing in sustainable production methods to meet environmental concerns while maintaining product quality and functionality.

Global Functional Protein Market Trends and Insights

Rising Demand for Protein-Enriched Functional Food and Beverages

Consumer preferences are shifting toward protein-enriched food products across various categories, with 64% of consumers actively incorporating additional protein into their diets, according to Danone. This shift extends beyond traditional protein supplements into mainstream food products, as evidenced by Kellogg's introduction of High Protein Bites cereal, containing 21% plant-based protein, in the UK market. The increasing health consciousness among consumers and growing awareness of protein's role in maintaining overall wellness are key factors driving this trend. Arla Foods' development of ISO.Clear whey protein isolate enables protein fortification in beverages without affecting clarity, targeting the USD 125 billion fortified drinks market, which is expected to grow at a 5.1% CAGR. The functional beverage segment is experiencing advancement through precision fermentation proteins, exemplified by EVERY Co.'s launch of animal-free protein formulations for coffee products. Additionally, manufacturers are investing in research and development to create innovative protein-enriched products that meet consumer demands for taste, convenience, and nutritional value.

Rapid Adoption of Plant-Based Protein

Plant-based protein adoption increases as technological improvements address traditional taste and texture limitations, with manufacturers prioritizing quality enhancement over new protein source development. Roquette Freres S.A.'s NUTRALYS Fava S900M, containing 90% protein content, exemplifies the industry's shift toward higher-purity plant proteins. The FDA's GRAS certification for Axiom Foods' Oryzatein rice protein enables its use in mainstream food applications, providing an alternative to conventional soy and whey proteins. Hybrid protein formulations attract global consumers seeking nutritional balance and environmental sustainability, as manufacturers develop blended solutions that preserve familiar taste profiles while reducing ecological impact. The market also benefits from increasing consumer awareness of protein's role in maintaining health and wellness, driving demand across various applications. Additionally, ongoing research and development in protein extraction and processing technologies continue to improve product functionality and cost-effectiveness.

Allergen Concerns with Animal and Soy Proteins

Allergen concerns with animal and soy proteins significantly restrict the functional protein market's growth by limiting consumer adoption due to widespread allergic reactions to dairy, egg, or soy. This forces manufacturers to invest in costly reformulations using alternative proteins like pea or rice, which can compromise functionality and raise production costs. Heightened demand for allergen-free products also pushes companies to prioritize safety and comply with strict labeling regulations, slowing innovation. Moreover, the need for extensive allergen testing and certification adds to operational complexities and expenses. Consumer apprehension about cross-contamination risks further dampens market confidence, reducing demand for products containing these proteins. Lastly, the limited availability of scalable, cost-effective hypoallergenic protein sources hinders the market's ability to meet growing demand for functional foods.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Aging Population with Specific Dietary Needs

- Inclusion in Pet Food and Animal Nutrition

- Taste, Solubility and Texture Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal-based proteins commanded 63.12% market share in 2024, anchored by dairy proteins' superior functional properties and established supply chains. This growth is supported by Arla Foods Amba's FDA approval for whey protein hydrolysates in infant formula . Microbial proteins emerge as the fastest-growing source segment at 8.35% CAGR through 2030, driven by scalability breakthroughs and regulatory approvals. Plant-based proteins maintain steady growth through improved extraction technologies and hybrid formulations addressing taste limitations.

MicroHarvest's achievement of 15,000-ton annual production capacity by 2026 demonstrates microbial protein commercialization potential, with the company overcoming traditional scaling challenges through process stability optimization. Precision fermentation platforms enable animal-identical protein production without traditional agriculture constraints, as evidenced by Perfect Day's partnership with Zydus Lifesciences to establish Indian manufacturing capabilities. Animal-based proteins benefit from processing innovations like Arla's ultra-filtered milk technologies, which concentrate protein content while maintaining functionality. Plant-based sources gain momentum through novel extraction methods and sustainable sourcing, with the EU's approval of Lemna protein concentrate representing regulatory acceptance of aquatic plant proteins

The Functional Proteins Market is Segmented by Source (Animal-Based Protein, Plant-Based Protein, and Microbial Protein), Category (Conventional, and Organic), Application (Food and Beverages, Supplements, Animal Feed and Pet Nutrition, and Cosmetics and Personal Care), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 36.21% revenue in 2024, reflecting large populations, rising middle-class incomes, and higher urbanization. Plant proteins sourced from soy, rice, and pea resonate with traditional cuisines, facilitating homegrown product development. Government programs promoting food security and value addition encourage investments in modern fractionation lines, supporting local supply sufficiency. Dairy-derived ingredients such as whey permeate also gain ground in sports powders sold via cross-border e-commerce, illustrating import complementarities. The protein market share attributed to North America is bolstered by dedicated distribution infrastructure, enabling rapid rollouts across health food stores, gyms, and mainstream retailers.

Europe exhibits strong momentum in organic and sustainable offerings, underpinned by stringent labeling regulations and institutional commitments to greenhouse-gas reduction. Retailers prioritize products featuring cleaner ingredient decks, supporting premiumization. The Middle East and Africa, while currently representing a smaller portion of global sales, is forecast to register the highest regional CAGR of 9.48% between 2025 and 2030. Demographic youth bulges, rising fitness club memberships, and expatriate influence favor sports powders and ready-to-drink shakes. Investments in aquaculture feed also heighten protein ingredient demand, with local governments encouraging private-sector participation.

Latin America leverages abundant crop availability to support soy and pea extraction facilities, supplying both domestic and export clients. Economic volatility occasionally constrains discretionary purchases, but demand for affordable nutrition maintains baseline stability. The region's established agricultural infrastructure and favorable climate conditions enable year-round production capabilities, creating a competitive advantage in the global protein market. Strategic investments in processing technology and facility expansion continue to enhance production efficiency and output capacity. Local governments are implementing supportive policies to strengthen the protein processing sector, aiming to capture greater value from agricultural resources. Overall, each region contributes distinct growth vectors that reinforce the diversified outlook for the protein market.

- Kerry Group plc.

- Sensient Technologies Corporation

- DSM-Firmenich

- Corbion

- Cargill, Incorporated.

- Agthia Group PJSC

- Glanbia, plc

- FrieslandCampina Ingredients

- Fonterra Co-Operative Group Limited

- International Flavors and Fragrances, Inc.

- Lallemand Inc.

- AngelYeast Co., Ltd.

- Sensient Technologies Corporation

- Alver World SA

- Enifer

- Zilor (Biorigin)

- Secil (Allmicroalgae)

- Sophie's Bionutrients

- NovoNutrients.

- Roquette Freres S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Protein-Enriched Functional Food and Beverages

- 4.2.2 Rapid Adoption of Plant-Based Protein

- 4.2.3 Advancements in Protein Extraction and Processing Technologies

- 4.2.4 Growing Demand for Sports and Performance Nutrition

- 4.2.5 Expanding aging population with specific dietary needs

- 4.2.6 Inclusion in pet food and animal nutrition

- 4.3 Market Restraints

- 4.3.1 Allergen Concerns with Animal and Soy Proteins

- 4.3.2 Taste, Solubility and Texture Challenges

- 4.3.3 Competition from conventional proteins

- 4.3.4 Regulatory hurdles and compliance issues

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Source

- 5.1.1 Animal-Based Protein

- 5.1.1.1 Dairy

- 5.1.1.1.1 Milk

- 5.1.1.1.2 Whey

- 5.1.1.1.3 Casein and Caseinates

- 5.1.1.2 Egg Protein

- 5.1.1.3 Others

- 5.1.2 Plant-Based Protein

- 5.1.2.1 Soy

- 5.1.2.2 Pea

- 5.1.2.3 Oat

- 5.1.2.4 Rice

- 5.1.2.5 Wheat

- 5.1.2.6 Others

- 5.1.3 Microbial Protein

- 5.1.1 Animal-Based Protein

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.1.1 Bakery and Confectionery

- 5.3.1.2 Infant Formula

- 5.3.1.3 Beverages

- 5.3.1.4 Dairy and Dairy Alternatives

- 5.3.1.5 Meat Analogues

- 5.3.2 Supplements

- 5.3.2.1 Sport/Performance Nutrition

- 5.3.2.2 Elderly Nutrition and Medical Nutrition

- 5.3.3 Animal Feed and Pet Nutrition

- 5.3.4 Cosmetics and Personal Care

- 5.3.1 Food and Beverages

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Kerry Group plc.

- 6.4.2 Sensient Technologies Corporation

- 6.4.3 DSM-Firmenich

- 6.4.4 Corbion

- 6.4.5 Cargill, Incorporated.

- 6.4.6 Agthia Group PJSC

- 6.4.7 Glanbia, plc

- 6.4.8 FrieslandCampina Ingredients

- 6.4.9 Fonterra Co-Operative Group Limited

- 6.4.10 International Flavors and Fragrances, Inc.

- 6.4.11 Lallemand Inc.

- 6.4.12 AngelYeast Co., Ltd.

- 6.4.13 Sensient Technologies Corporation

- 6.4.14 Alver World SA

- 6.4.15 Enifer

- 6.4.16 Zilor (Biorigin)

- 6.4.17 Secil (Allmicroalgae)

- 6.4.18 Sophie's Bionutrients

- 6.4.19 NovoNutrients.

- 6.4.20 Roquette Freres S.A.

7 Market Opportunities and Future Outlook