PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842645

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842645

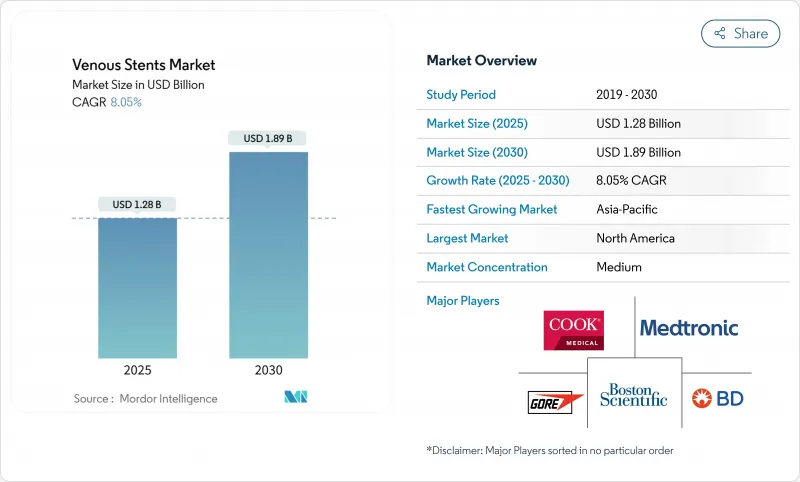

Venous Stents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The venous stents market stands at USD 1.28 billion in 2025 and is forecast to reach USD 1.89 billion by 2030, translating into an 8.05% CAGR over the period.

Robust demand comes from growing recognition that dedicated venous stents deliver better long-term patency than balloon angioplasty, especially in chronic deep vein obstruction. Market momentum is reinforced by higher disease prevalence in aging populations, steady regulatory approvals for nitinol-based devices, and payers embracing outpatient venous procedures. Clinical data showing 84.0% three-year primary patency with modern stents continues to drive physician confidence. On the supply side, manufacturers are mitigating raw-material risks through diversified nitinol sourcing while accelerating innovation in drug-eluting and polymer-coated platforms to maintain competitive differentiation.

Global Venous Stents Market Trends and Insights

Rising Prevalence of Chronic Symptomatic Venous Diseases

Post-thrombotic syndrome affects up to 50% of patients after deep vein thrombosis, and earlier detection is funneling more candidates toward intervention. The VERNACULAR study reported 84.0% primary patency at 36 months for modern stents, underscoring their value in difficult cases. Growing awareness of May-Thurner syndrome among younger adults is widening the treated population. These epidemiologic shifts are most evident in markets with robust vascular specialization and aging demographics. As a result, the venous stents market is poised to benefit from sustained procedure growth over the forecast horizon.

Ageing Population Boosting Venous Interventions

Populations aged 65+ experience higher chronic venous insufficiency, prompting guideline updates that advocate earlier stenting when conservative therapy fails. Geriatric patients often present with multimorbidity, so devices designed for shorter procedure times and lower anticoagulation needs are gaining favor. Japan and Western Europe exemplify how super-aged societies accelerate adoption of minimally invasive venous treatments. These macro-demographics give the venous stents market a durable, long-term growth underpinning.

High Procedure Cost & Limited Patient Awareness

Total treatment cost can exceed USD 15,000 in systems without strong coverage, limiting access in lower-income regions. Many patients remain unaware that minimally invasive venous therapies exist, and community clinics often lack the imaging needed for diagnosis. Education campaigns aimed at primary care and the public are critical to expanding the venous stents market. Without them, underdiagnosis will continue to suppress demand despite clinical efficacy.

Other drivers and restraints analyzed in the detailed report include:

- Dedicated Nitinol Venous Stents Gaining Regulatory Approvals

- Favourable Reimbursement for Outpatient Venous Procedures

- In-Stent Restenosis / Re-Occlusion Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Leg interventions generated the largest revenue in 2024, capturing 43.56% of the venous stents market size because post-thrombotic iliofemoral obstruction remains the most common indication. Pelvic procedures, fueled by heightened recognition of May-Thurner syndrome, will outpace all other segments at a 12.46% CAGR. TOPOS trial data showing 90% 12-month patency for oblique nitinol stents in common iliac compression underpin this momentum.Emergence of dedicated protocols for chronic pelvic pain is channeling younger patients toward intervention, expanding total addressable volume.

Rising use of IVUS and venography in office-based labs elevates diagnostic accuracy for pelvic lesions, improving patient selection and outcomes. ASCs leverage shorter recovery times to attract these cases, supporting outpatient expansion within the venous stents market. Meanwhile, abdominal IVC and renal vein work remains niche, and chest interventions for superior vena cava syndrome are largely confined to tertiary centers. Collectively, these trends diversify procedural mix and reinforce long-term market vitality.

Chronic deep vein thrombosis retained 39.65% venous stents market share in 2024, but non-thrombotic iliac vein lesions will log an 11.34% CAGR through 2030 as clinicians diagnose compression earlier. Abre stent data revealing 97.1% three-year patency in NIVL patients bolsters confidence. Post-thrombotic syndrome, with its collateral burden, still commands large volumes, yet improved algorithms segregate thrombotic from non-thrombotic cases more effectively.

Expanding indications now include venous claudication and chronic pelvic pain, broadening the candidate pool. Acute DVT cases increasingly see adjunctive stenting following thrombectomy to maintain flow. Future growth will depend on payer recognition of these new indications and continued performance of dedicated devices across lesion types.

Venous Stents Market Report is Segmented by Application (Leg, Pelvic, Abdomen, Chest and Others), Disease (Chronic Deep Vein Thrombosis, Post-Thrombotic Syndrome and More), Stent Type (Self-Expanding Nitinol Stents, Balloon-Expandable Stents and More), Material (Nitinol, Stainless Steel and More), End User (Hospitals, Ambulatory Surgical Centres and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.72% of 2024 revenue thanks to mature reimbursement, extensive ASC networks and rapid uptake of newly approved stents. Dedicated registries and post-market studies reinforce safety, encouraging early use in complex disease. Multidisciplinary vascular teams integrate stenting into comprehensive care pathways, supporting procedure volumes across both hospital and outpatient settings.

Europe contributes substantial scientific output and follows standardized treatment algorithms laid out by the 2024 ESVS guidelines. Country-level reimbursement disparities, however, create uneven adoption. Germany and the United Kingdom spearhead clinical research, influencing neighboring markets. Brexit-related regulatory divergence introduces some approval uncertainty, yet demographic drivers and robust evidence maintain steady growth.

Asia-Pacific will post the fastest 11.46% CAGR as infrastructure improves and awareness rises. China's insurance reforms and Japan's aging demographic are key catalysts, though limited specialist density restrains some local uptake. International manufacturers are investing in physician education and localized production to navigate complex regulatory pathways. India and Southeast Asia represent longer-term opportunities once procedural capacity broadens.

- Abbott Laboratories

- Beckton Dickinson

- Bentley InnoMed GmbH

- Boston Scientific

- Cook Group

- Cordis

- W. L. Gore & Associates

- plus medica GmbH & Co. KG

- Medtronic

- MicroPort

- Optimed Medizinische Instrumente GmbH

- Koninklijke Philips

- Sinomed

- Terumo Corp.

- Zinas Medical

- Zylox-Tonbridge

- Merit Medical Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Symptomatic Venous Diseases

- 4.2.2 Ageing Population Boosting Venous Interventions

- 4.2.3 Dedicated Nitinol Venous Stents Gaining Regulatory Approvals

- 4.2.4 Favourable Reimbursement For Outpatient Venous Procedures

- 4.2.5 IVUS-Guided Sizing Improving Primary Patency

- 4.2.6 Surge In Ambulatory Vascular Centres

- 4.3 Market Restraints

- 4.3.1 High Procedure Cost & Limited Patient Awareness

- 4.3.2 In-Stent Restenosis / Re-Occlusion Risk

- 4.3.3 Nitinol Supply-Chain Disruptions (Geo-Political)

- 4.3.4 Early Product Recalls Dampening Clinician Confidence

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Application

- 5.1.1 Leg (Ilio-femoral)

- 5.1.2 Pelvic

- 5.1.3 Abdomen (IVC / Renal)

- 5.1.4 Chest (SVC)

- 5.1.5 Others

- 5.2 By Disease

- 5.2.1 Chronic Deep Vein Thrombosis

- 5.2.2 Post-Thrombotic Syndrome

- 5.2.3 Non-Thrombotic Iliac Vein Lesion / May-Thurner

- 5.2.4 Acute DVT

- 5.2.5 Others

- 5.3 By Stent Type

- 5.3.1 Self-expanding Nitinol Stents

- 5.3.2 Balloon-expandable Stents

- 5.3.3 Covered Stents

- 5.3.4 Drug-eluting Stents

- 5.3.5 Bioresorbable Scaffolds

- 5.3.6 Others

- 5.4 By Material

- 5.4.1 Nitinol

- 5.4.2 Elgiloy / Co-Cr Alloy

- 5.4.3 Stainless Steel

- 5.4.4 Polymer-based

- 5.4.5 Others

- 5.5 By End-user

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centres

- 5.5.3 Specialty Vein Clinics

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Bentley InnoMed GmbH

- 6.3.4 Boston Scientific Corporation

- 6.3.5 Cook Medical

- 6.3.6 Cordis Inc.

- 6.3.7 W. L. Gore & Associates

- 6.3.8 plus medica GmbH & Co. KG

- 6.3.9 Medtronic plc

- 6.3.10 MicroPort Scientific Corporation

- 6.3.11 Optimed Medizinische Instrumente GmbH

- 6.3.12 Koninklijke Philips N.V.,

- 6.3.13 Sinomed

- 6.3.14 Terumo Corp.

- 6.3.15 Zinas Medical

- 6.3.16 Zylox-Tonbridge

- 6.3.17 Merit Medical Systems

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment