PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842661

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842661

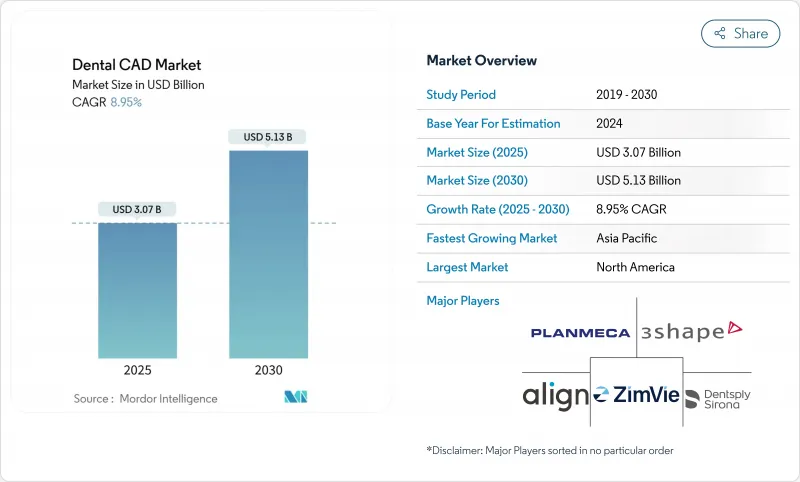

Dental CAD - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Dental CAD market is valued at USD 3.07 billion in 2025 and is on course to reach USD 5.13 billion by 2030, expanding at an 8.95% CAGR.

Growth rests on the accelerating shift from analog laboratories to end-to-end digital workflows that shorten crown design-to-delivery cycles from hours to minutes while preserving micrometer-level accuracy. Artificial-intelligence (AI) layers now automate restoration design, suggesting connectors, emergence profiles, and occlusal contacts in real time and trimming two-thirds of manual CAD time per case. Hardware commoditization is nudging competitive advantage toward software ecosystems that unify intraoral scanners, cloud collaboration portals, and chairside milling units. Demographic aging, rising implant acceptance, and global DSO consolidation further anchor long-range growth as large practice networks standardize procurement and training across hundreds of sites. Europe maintains leadership through stringent quality standards and early digital adoption, yet Asia-Pacific shows the steepest curve as healthcare infrastructure investment coincides with growing patient spending power.

Global Dental CAD Market Trends and Insights

Increasing Adoption of Chairside Digital Workflows

Same-day dentistry is now tangible because chairside systems link intraoral scanners, AI-enabled CAD engines, and four-axis mills in a single appointment window. Practices deploying a second mill report 145% production lifts within four months as average monthly units jump from 13.3 to 27.5. Patients show strong preference for single-visit crowns, with 85% valuing convenience and half agreeing to premium pricing. Scanner refresh rates of 1.3 seconds and 94% acceptance rates for AI-proposed designs further compress clinical bottlenecks. Nevertheless, offices must synchronize scanning, design, nesting, and milling while adhering to infection-control protocols and insurance coding.

Rising Prevalence of Restorative & Prosthetic Procedures

The proportion of adults aged 65+ is swelling in every major economy, raising restorative workloads that reward CAD precision. Full-arch implant plans merge cone-beam CT with parametric libraries to place fixtures within +-50 µm of intended axes. Surgeons increasingly deploy 3-D-printed titanium meshes shaped by CAD to steer guided bone regeneration, customizing pore width to vascularization requirements and lowering bill-of-materials versus machined alternatives. Digital smile-design modules overlay facial scans on intraoral data, allowing shade simulation and occlusal mapping before irreversible drilling. Integration of photogrammetry devices further expands data richness, enabling bite capture during open-tray impressions without splints.

High Upfront Capital Expenditure

A premium chairside package can top USD 150,000 and depreciates over three to five years, forcing smaller offices to weigh loan payments against fluctuating case volumes. Annual service contracts and software subscriptions tack on 20-30% of list prices, while frequent firmware updates can mandate hardware upgrades. Leasing, revenue-share agreements, and design-as-a-service portals have emerged to cushion the blow, but each model imposes its own margin erosion and data-sovereignty questions.

Other drivers and restraints analyzed in the detailed report include:

- Cost- & Time-Efficiency Versus Conventional Techniques

- AI-Driven Generative Design for Complex Restorations

- Limited Reimbursement for CAD/CAM Restorations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Milling units held 63.70% of the Dental CAD market share in 2024, underscoring the indispensability of subtractive workflows for final zirconia and hybrid ceramic restorations. Entry-level mills list at USD 20,000-50,000, mid-range at USD 50,000-100,000, and flagship five-axis systems at USD 100,000-150,000, allowing clinicians to scale capacity to patient throughput. Scanner throughput leapt 53% over the last hardware generation, capturing full-arch data in under 40 seconds and pre-segmenting margin lines via embedded AI.

Software, however, is the fastest climbing component at 9.98% CAGR. Vendors are pivoting to subscription and cloud license bundles that smooth cashflows while continuously feeding AI model updates. Exocad's DentalCAD 3.2 shipped AI Design to auto-generate crown libraries, whereas 3Shape Automate now closes roughly 94% of crown designs without technician touch-ups. Beyond design, platforms integrate case tracking, remote approval, and KPI dashboards, letting multi-site groups compare rounding errors and turnaround-time deltas. Open API philosophies are likewise proliferating to court niche startups that supply AI margin detection or shade-matching algorithms, deepening ecosystem stickiness.

The Dental CAD Market is Segmented by Component (Scanners, Milling Machines, Software, and Other Components), by Application (Crowns & Bridges, Dentures and More), by End User ( Dental Laboratories, Dental Clinics & Hospitals and More) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 32.68% of Dental CAD market revenue in 2024 thanks to strong reimbursement, rigorous CE marking discipline, and early adoption of intraoral scanners across Germany, the United Kingdom, and France. CE compliance routines drive continuous software validation cycles, compelling vendors to roll out iterative updates and data-protection safeguards. Consolidation among continental laboratories fosters standardized production pipelines that tap five-axis mills and multi-chamber sintering furnaces, reducing per-unit labor overhead. Aging populations are pushing prosthetic demand higher, cementing long-term volume growth.

Asia-Pacific is the sprint leader, forecast at an 11.56% CAGR through 2030. China and India pour capital into community oral-health clinics while large private chains open implant-focused centers that advertise same-day crowns. Domestic hardware manufacturers now supply mid-range scanners and mills at 20-30% lower price points than European imports, augmenting affordability without sacrificing baseline precision. Governments in Japan and South Korea subsidize AI-driven diagnostic projects, enabling hybrid cloud architectures that meet stringent patient-data localization laws. Training remains a chokepoint, so vendors host certified academies in Bangkok and Shenzhen to accelerate clinician onboarding.

North America presents a mature but still dynamic landscape. DSOs consolidate purchasing power, forcing vendors into national tender contracts that bundle hardware, license seats, and service SLAs. FDA clearances for AI design and diagnostic modules gather pace, but reimbursement frameworks lag, prompting practices to market CAD crowns as premium elective offerings. Data-security compliance under HIPAA and state data-breach statutes compels cloud providers to employ zero-knowledge encryption and redundant backups within continental borders. Market focal points have therefore moved from raw adoption to interoperability, uptime, and analytics-rooted ROI metrics.

- Market Overview

- Market Drivers

- Market Restraints

- Value / Supply-Chain Analysis

- Regulatory Landscape

- Technological Outlook

- Porter's Five Forces

- Market Concentration

- Market Share Analysis

- Dentsply Sirona

- Align Technology (exocad GmbH)

- 3 Shape

- Planmeca

- Ivoclar Vivadent

- Straumann Group

- Amann Girrbach

- Zirkonzahn GmbH

- Dental Wings Inc.

- Carestream Dental

- Roland DG Corp. (DGSHAPE)

- Shining 3D Tech Co., Ltd.

- Renishaw plc

- vhf camfacture AG

- Vatech Co., Ltd.

- Medit Corp.

- Kulzer

- 3M Company (Oral Care)

- Bego GmbH & Co. KG

- Argen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing adoption of chairside digital workflows

- 4.2.2 Rising prevalence of restorative & prosthetic procedures

- 4.2.3 Cost- & time-efficiency versus conventional techniques

- 4.2.4 Integration with intraoral scanning & 3-D printing ecosystems

- 4.2.5 AI-driven generative design for complex restorations (under-radar)

- 4.2.6 DSO roll-outs of standardized CAD platforms (under-radar)

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Limited reimbursement for CAD/CAM restorations

- 4.3.3 Cyber-security & data-interoperability risks (under-radar)

- 4.3.4 Technician skills gap in parametric modelling (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component (Value)

- 5.1.1 Scanner

- 5.1.2 Milling Machines

- 5.1.3 Software

- 5.1.4 Other

- 5.2 By End User (Value)

- 5.2.1 Dental Laboratories

- 5.2.2 Dental Clinics & Hospitals

- 5.2.3 Academic & Research Institutes

- 5.3 By Application/ Indication (Value)

- 5.3.1 Crowns & Bridges

- 5.3.2 Dentures

- 5.3.3 Implants

- 5.3.4 Orthodontic Appliances

- 5.3.5 Others

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4 Dentsply Sirona

- 6.5 Align Technology (exocad GmbH)

- 6.6 3Shape A/S

- 6.7 Planmeca Oy

- 6.8 Ivoclar Vivadent AG

- 6.9 Straumann Group

- 6.10 Amann Girrbach AG

- 6.11 Zirkonzahn GmbH

- 6.12 Dental Wings Inc.

- 6.13 Carestream Dental LLC

- 6.14 Roland DG Corp. (DGSHAPE)

- 6.15 Shining 3D Tech Co., Ltd.

- 6.16 Renishaw plc

- 6.17 vhf camfacture AG

- 6.18 Vatech Co., Ltd.

- 6.19 Medit Corp.

- 6.20 Kulzer GmbH

- 6.21 3M Company (Oral Care)

- 6.22 Bego GmbH & Co. KG

- 6.23 Argen Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment