PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842673

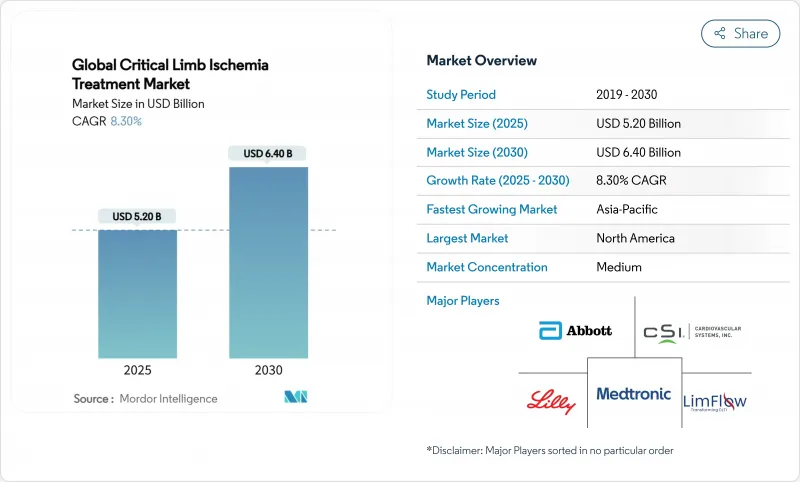

Global Critical Limb Ischemia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The critical limb ischemia treatment market stood at USD 5.2 billion in 2025 and is expected to reach USD 6.4 billion by 2030, reflecting a 7.5% CAGR over the forecast period.

Growing life expectancy, the sharp rise in diabetes prevalence, and rapid clinical adoption of advanced below-the-knee (BTK) endovascular technologies underpin this expansion. Health-system priorities are also shifting: hospital programs increasingly emphasize limb preservation rather than amputation because multidisciplinary salvage pathways show lower long-term costs and superior quality-of-life outcomes. Breakthrough regulatory approvals such as Abbott's Esprit BTK resorbable scaffold, which lowered reintervention rates by 48% versus balloon angioplasty, have raised physician confidence in novel devices and opened sizable addressable patient pools. Parallel progress in gene, cell, and GLP-1-based pharmacotherapies signals an emerging therapeutic toolbox that aims to reverse microvascular pathology rather than merely reopen occluded arteries, further broadening clinical options for patients once considered no-option candidates.

Global Critical Limb Ischemia Treatment Market Trends and Insights

Rising Diabetes-Linked CLI Prevalence

Escalating global diabetes incidence propels critical limb ischemia case volumes because metabolic dysfunction accelerates arterial calcification and microvascular compromise. Recent cohort studies recorded 21.7% amputation rates among diabetic CLI patients despite guideline-directed revascularization, while 96.9% of those patients reported severe quality-of-life impairment.These findings intensify demand for more durable BTK solutions such as Abbott's Esprit BTK scaffold, which achieved 74% composite efficacy versus 44% with plain angioplasty. Diabetes also heightens interest in dual-benefit pharmacology: the STRIDE trial showed semaglutide improving 6-minute walk distance by 26 m in this cohort and lowering cardiovascular events, suggesting metabolic modulation can postpone progression to major amputation. As a result, integrated vascular-endocrine programs are proliferating within limb-preservation centers worldwide.

Rapid Uptake of Drug-Coated Balloons & Stents

Drug-eluting technologies continue to displace plain angioplasty in below-the-knee lesions. Boston Scientific's AGENT balloon, granted Medicare Transitional Pass-Through status from January 2025, cut target lesion revascularization risk by 50% in BTK disease. A contemporaneous FDA meta-analysis resolved earlier paclitaxel-safety concerns, reopening the reimbursement pathway for CLI indications. Five-year IN.PACT Global data have since shown 69.4% freedom from clinically driven revascularization, consolidating real-world evidence for drug coating durability in complex anatomy. Market competition is now centered on next-generation formulations that deliver equivalent efficacy with lower drug doses, exemplified by Surmodics' Sundance platform that targets 56% drug-dose reduction while preserving patency. Collectively, these factors continue to expand the critical limb ischemia treatment market by widening physician uptake in community hospitals previously deterred by safety overhang.

Stringent Device Recalls & FDA Scrutiny

Consecutive Class I recalls involving CLI devices-such as Inari's ClotTriever XL linked to 6 deaths and Philips' Tack system pulled after 20 injuries-have heightened regulatory caution. The U.S. FDA now requires richer BTK-specific safety datasets, prolonging approval timelines and elevating trial expense, especially for small innovators specializing in limb salvage. Hospitals also respond by tightening product-evaluation committees, sometimes deferring new technology uptake until extensive post-market surveillance emerges. While these protections ultimately benefit patients, near-term commercial adoption curves flatten, tempering overall critical limb ischemia treatment market growth during the review window.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Reimbursement & Limb-Salvage Mandates

- Shift to Minimally Invasive Endovascular Care

- High Restenosis / Repeat-Procedure Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices commanded 69.8% of the critical limb ischemia treatment market in 2024, anchored by drug-coated balloons (DCBs), drug-eluting stents (DES), intravascular lithotripsy systems, and resorbable scaffolds designed for fragile BTK vessels. DCBs and DES together generated more than USD 2.8 billion, buoyed by reinstated U.S. coverage and robust evidence for reduced reintervention. Intravascular lithotripsy is the fastest-penetrating subsegment; Shockwave's platform alone posted 75% year-on-year sales growth after securing Japanese reimbursement in late 2024. Embolic-protection filters also gain importance as operators tackle long chronic total occlusions (CTOs) where distal runoff is limited. With these dynamics, the critical limb ischemia treatment market size attributed to device therapy is forecast to expand from USD 3.6 billion in 2025 to USD 4.6 billion in 2030, representing a 5.0% device-specific CAGR.

Surgical grafts and hybrid operating suites nonetheless retain clinical relevance for multilevel disease. Autologous vein remains gold standard for femorotibial bypass, but registry data show HePTFE's limb-salvage equivalence when vein quality is poor, sustaining modest graft demand despite PFAS-related headwinds. Regenerative approaches deliver the most compelling long-term upside: XyloCor's XC001 angiogenic gene therapy improved peak treadmill time by 109 seconds at 12 months in no-option CLI, while Phase 2 stem-cell trials reported 36% greater perfusion index versus placebo. These studies support a 17.5% CAGR for gene- and cell-therapy revenue through 2030, albeit from a low base. Pharmaceuticals re-emerge as an adjunct: semaglutide's STRIDE and rivaroxaban's recent generic approval broaden systemic therapy use, generating a projected USD 900 million in drug sales by 2030. Collectively, these developments indicate the critical limb ischemia treatment industry is steadily migrating from device-centric rescue toward integrated, biologically informed care pathways.

The Critical Limb Ischemia Treatment Market is Segmented by Treatment Type, Including Devices (Embolic Protection Devices, Peripheral Dilatation Systems, and More), Drugs (Antiplatelet Drugs, Antihypertensive Agents, Lipid-Lowering Agents, and More), and Surgery (Bypass Surgery and Amputation), Along With Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific contributed 21.3% of global revenue in 2024 and is forecast to grow at a 9.1% CAGR, the fastest regional trajectory worldwide. China registered more than 1.1 million new peripheral artery disease admissions in 2024, 23% of whom presented with tissue loss, underscoring substantial unmet need. Over 60 home-grown peripheral devices obtained National Medical Products Administration clearance in 2024, and the critical limb ischemia treatment market size for China alone is expected to reach USD 1.2 billion by 2030, expanding 10.4% annually. Simultaneously, India's device-rule harmonization with EU MDR catalyzes foreign direct investment in cath-lab infrastructure; secondary-city hospitals are now equipped for DCB procedures that were previously limited to tertiary centers.

North America retained 46.4% of global revenue in 2024 due to favorable reimbursement, mature limb-salvage networks, and early adoption of breakthrough platforms such as LimFlow's arterialization and AI triage algorithms. The region will continue to expand at 6.4% CAGR as Medicare's bundled payment models reward long-term amputation-free survival-metrics strongly correlated with high-cost device utilization. European markets are navigating regulatory turbulence: PFAS restrictions could contract supply of vascular grafts, but the EU's fast-track designation for resorbable polymers may mitigate long-term disruption. Nonetheless, price-control policies in France and Germany dampen ASP expansion, capping European CAGR at 4.2%. Elsewhere, Latin America and the Middle East & Africa remain early-stage; Brazil's public-hospital procurement now authorizes DCBs in 10 states, while Gulf Cooperation Council tenders increasingly bundle IVL and wound-care consumables, signaling gradual diversification away from amputation-dominant paradigms.

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Terumo

- Cook Group

- Beckton Dickinson

- Philips (Spectranetics)

- W. L. Gore & Associates

- Inari Medical Inc.

- Shockwave Medical Inc.

- AngioDynamics

- Cardiovascular Systems

- LimFlow

- Cynata Therapeutics

- Rexgenero Ltd

- LimFlow S

- Micro Medical Solutions

- Bayer

- Shockwave Medical Inc.

- BIOTRONIK

- Bentley InnoMed GmbH

- Getinge

- Penumbra

- Endologix LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes-Linked PAD Prevalence

- 4.2.2 Rapid Uptake Of Drug-Coated Balloons & Stents

- 4.2.3 Favorable Reimbursement & Limb-Salvage Mandates

- 4.2.4 Shift To Minimally-Invasive Endovascular Care

- 4.2.5 Emerging Intravascular Lithotripsy Adoption

- 4.2.6 AI-Driven Limb-Preservation Centers

- 4.3 Market Restraints

- 4.3.1 Stringent Device Recalls & FDA Scrutiny

- 4.3.2 High Restenosis / Repeat-Procedure Burden

- 4.3.3 Late Diagnosis & Low Primary-Care Awareness

- 4.3.4 HePTFE Graft Supply-Chain Bottlenecks

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Treatment Type

- 5.1.1 Devices

- 5.1.1.1 Embolic Protection Devices

- 5.1.1.2 Peripheral Dilatation Systems

- 5.1.1.3 Drug-Coated Balloons

- 5.1.1.4 Drug-Eluting Stents

- 5.1.1.5 Intravascular Lithotripsy Systems

- 5.1.2 Drugs

- 5.1.2.1 Antiplatelet Drugs

- 5.1.2.2 Antihypertensive Agents

- 5.1.2.3 Lipid-Lowering Agents

- 5.1.2.4 Novel Gene & Cell Therapies

- 5.1.3 Surgery

- 5.1.3.1 Bypass Surgery

- 5.1.3.2 Amputation (Last Resort)

- 5.1.1 Devices

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia Pacific

- 5.2.4 Middle East & Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.2.1 GCC

- 5.2.4.3 Rest of Middle East & Africa

- 5.2.4.3.1 Turkey

- 5.2.5 South America

- 5.2.5.1 Rest of Middle East

- 5.2.5.2 Brazil

- 5.2.5.3 Argentina

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corp.

- 6.3.4 Terumo Corporation

- 6.3.5 Cook Medical LLC

- 6.3.6 Becton, Dickinson & Co.

- 6.3.7 Philips (Spectranetics)

- 6.3.8 W. L. Gore & Associates

- 6.3.9 Inari Medical Inc.

- 6.3.10 Shockwave Medical Inc.

- 6.3.11 AngioDynamics Inc.

- 6.3.12 Cardiovascular Systems Inc.

- 6.3.13 LimFlow SA

- 6.3.14 Cynata Therapeutics Ltd

- 6.3.15 Rexgenero Ltd

- 6.3.16 LimFlow S

- 6.3.17 Micro Medical Solutions

- 6.3.18 Bayer AG

- 6.3.19 Shockwave Medical Inc.

- 6.3.20 Biotronik SE & Co. KG

- 6.3.21 Bentley InnoMed GmbH

- 6.3.22 Getinge AB

- 6.3.23 Penumbra Inc.

- 6.3.24 Endologix LLC

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment