PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842693

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842693

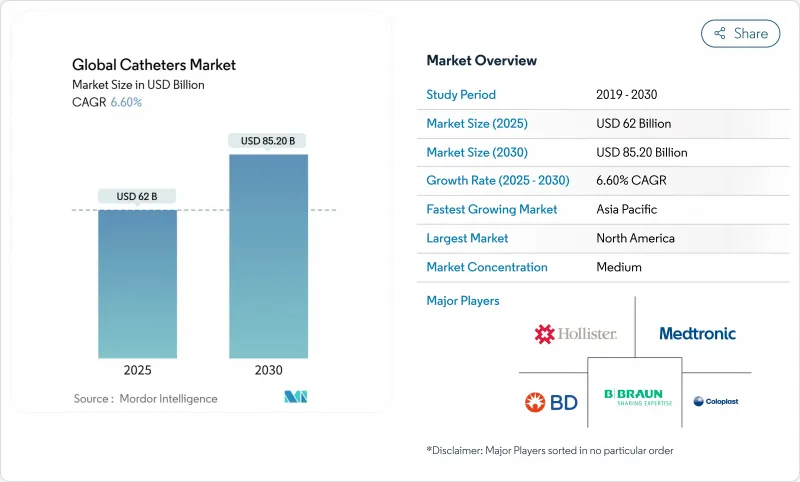

Global Catheters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The catheters market stood at USD 62.0 billion in 2025 and is forecast to reach USD 85.2 billion by 2030, advancing at a 6.6% CAGR.

Demographic aging, a rising burden of chronic cardiovascular and renal disease, and broader acceptance of minimally invasive procedures continue to stimulate demand. Technology cycles that deliver smarter coatings, embedded sensors, and AI-aided designs further widen the clinical utility of catheter products. At the same time, supply-chain re-engineering for specialty polymers and silicone has become a strategic focus as manufacturers strive to maintain consistent quality and pricing. Competitive positioning pivots on innovation pipelines, as firms look to consolidate fragmented product niches and defend intellectual property. Opportunities remain strong in home-based self-care, where supportive reimbursement and telehealth services enable non-institutional treatment pathways, extending the addressable catheters market well beyond traditional hospital settings.

Global Catheters Market Trends and Insights

Rising Prevalence of Cardiovascular, Neurological & Urological Disorders

Cardiovascular disease now affects 655 million individuals, while stroke incidence climbed 15% from 2019-2024, driving adoption of neurovascular catheters for thrombectomy procedures . Chronic kidney disease impacts 850 million people and lifts demand for dialysis access catheters as hemodialysis populations in developed regions expand 6% annually. This epidemiological momentum makes catheter volumes less sensitive to economic cycles and underscores their role as essential care tools within the broader catheters market.

Increasing Uptake of Minimally Invasive Interventions

Catheter-based techniques represent 75% of cardiovascular procedures in developed healthcare systems, up from 45% ten years ago. Medtronic's PulseSelect pulsed-field ablation platform posted 30% revenue growth in 2024, reflecting a system-wide push to lower hospital stays and improve outcomes . Robotic navigation solutions such as Stereotaxis EMAGIN also enhance precision while curbing radiation exposure. These dynamics reinforce sustained demand across the catheters market as payers seek greater procedural efficiency.

Catheter-Associated Infections & Biofilm Formation

Indwelling catheter infection rates touch 25% in some settings, with catheter-related bloodstream infections carrying mortality rates up to 25%. As regulators tighten infection control protocols, device dwell time restrictions and more frequent replacements raise costs and complicate clinical workflows, curbing short-term momentum in the catheters market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Demand for Antimicrobial & Hydrophilic-Coated Catheters

- Rapid Adoption of Home-Based Self-Catheterization

- Polymer & Silicone Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cardiovascular catheters delivered 28.7% of the catheters market in 2024, supported by entrenched clinical protocols across angiography, ablation, and electrophysiology. This maturity ensures stable volumes as hospitals routinely stock multiple sizes and configurations. The catheters market size for cardiovascular interventions is projected to widen at a steady clip in line with coronary disease prevalence. Neurovascular catheters, while still smaller by revenue, advance at a 7.3% CAGR as stroke centers expand and mechanical thrombectomy devices prove efficacy. Stanford's milli-spinner technique posts 90% success versus 50% for legacy systems, underscoring technology-led upside.

Innovation pipelines remain active. Steerable tips, refined braiding, and softer polymers elevate neurovascular navigation, narrowing risk profiles and opening new procedural indications. Intravenous catheters stay the highest-volume consumable in hospital supply chains, but margin pressures persist given commoditized pricing. Specialty designs-ranging from occlusion balloons to drug-eluting configurations-command premium pricing and cushion profitability. Across categories, clinical evidence, reimbursement clarity, and material availability shape share shifts inside the broader catheters market.

The Catheters Market Report Segments the Industry Into by Product (Cardiovascular Catheters, Urology Catheters, Intravenous Catheters, Neurovascular Catheters, Other Products), by End User (Hospitals, Long Term Care Facilities, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, South America). Get Five Years of Historical Trends Plus Forecasts for the Next Five Years.

Geography Analysis

North America retained 43.3% of global revenue in 2024, underpinned by advanced hospital networks, early technology adoption, and favorable reimbursement. The FDA's breakthrough-device pathway has quickened market entry for novel catheters, while Medicare coverage expansions offer tailwinds for high-value devices. Even so, mature-market price compression and hospital budget scrutiny put a ceiling on volume growth. Regulatory stability and predictable payment landscape still make the region a testing ground for premium catheter technologies, cementing its influence on the catheters market.

Europe stands as the second-largest cluster, shaped by the Medical Device Regulation. Stringent technical documentation and post-market surveillance raise compliance costs, especially for small firms, potentially consolidating supplier bases. Infection-prevention priorities and antimicrobial stewardship stimulate demand for coated and single-use devices. Brexit-related logistics challenges and shifts in public-tender rules, including moves to exclude certain foreign suppliers, complicate supply-chain planning yet may favor local manufacturing. The net impact is a cautious but quality-focused European catheters market.

Asia-Pacific is the fastest-growing theater, expanding at an 8.3% CAGR through 2030. Health-system modernization, rising surgical volumes, and government investment in universal care strengthen underlying demand. The region's medical-technology spending is projected to hit USD 225 billion by 2030. Local manufacturing incentives, technology-transfer agreements, and a burgeoning private-hospital segment in India and Southeast Asia lower entry barriers. Nevertheless, heterogeneous regulatory regimes and price-cap policies require nuanced go-to-market strategies for firms seeking to scale in the APAC catheters market.

- Abbott Laboratories

- B. Braun

- Becton, Dickinson & Co. (C. R. Bard)

- Boston Scientific

- Coloplast

- Convatec

- Edwards Lifesciences Corp.

- Hollister

- Johnson & Johnson

- Medtronic

- Teleflex

- Terumo Corp.

- BIOTRONIK

- Cook Group

- Smiths Group

- Cardinal Health

- Merit Medical Systems

- Penumbra

- AngioDynamics

- Amsino International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of cardiovascular, neurological & urological disorders

- 4.2.2 Increasing uptake of minimally invasive interventions

- 4.2.3 Surge in demand for antimicrobial & hydrophilic-coated catheters

- 4.2.4 Rapid adoption of home-based self-catheterisation (under-reported)

- 4.2.5 Integration of smart/connected sensor catheters for real-time monitoring (under-reported)

- 4.2.6 Growth of ambulatory surgical centres in emerging markets (under-reported)

- 4.3 Market Restraints

- 4.3.1 Catheter-associated infections & biofilm formation

- 4.3.2 Availability of non-catheter substitutes (e.g., drug pumps, stents)

- 4.3.3 Polymer & silicone supply-chain volatility (under-reported)

- 4.3.4 Reimbursement pressure in mature markets (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Cardiovascular Catheters

- 5.1.2 Urology Catheters

- 5.1.3 Intravenous Catheters

- 5.1.4 Neurovascular Catheters

- 5.1.5 Specialty / Other Catheters

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centres

- 5.2.3 Home-care Settings

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Cardiovascular Procedures

- 5.3.2 Urinary Incontinence & Retention

- 5.3.3 Dialysis & Renal Disorders

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Becton, Dickinson & Co. (C. R. Bard)

- 6.3.4 Boston Scientific Corp.

- 6.3.5 Coloplast A/S

- 6.3.6 ConvaTec Group PLC

- 6.3.7 Edwards Lifesciences Corp.

- 6.3.8 Hollister Incorporated

- 6.3.9 Johnson & Johnson (DePuy Synthes)

- 6.3.10 Medtronic PLC

- 6.3.11 Teleflex Inc.

- 6.3.12 Terumo Corp.

- 6.3.13 Biotronik SE & Co. KG

- 6.3.14 Cook Medical

- 6.3.15 Smiths Medical

- 6.3.16 Cardinal Health

- 6.3.17 Merit Medical Systems

- 6.3.18 Penumbra Inc.

- 6.3.19 AngioDynamics Inc.

- 6.3.20 Amsino International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment