PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1938977

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1938977

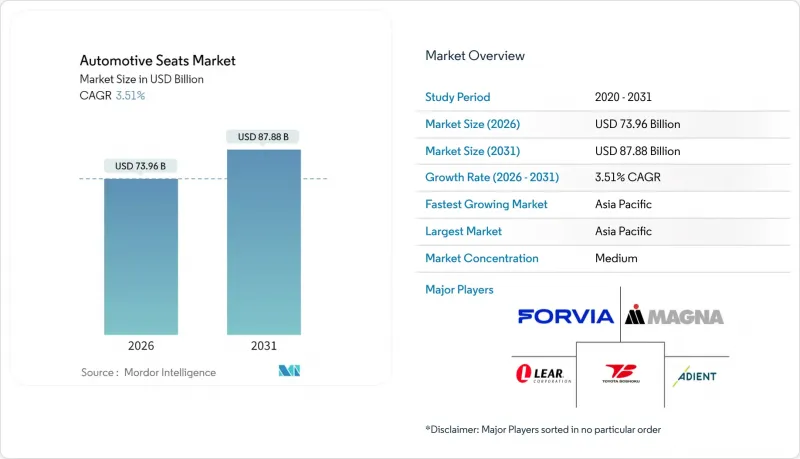

Automotive Seats - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The automotive seat market size in 2026 is estimated at USD 73.96 billion, growing from 2025 value of USD 71.45 billion with 2031 projections showing USD 87.88 billion, growing at 3.51% CAGR over 2026-2031.

Growth stays positive as electrification, autonomous driving features, and a rising preference for premium comfort push redesigns of seat frames, cushions, and electronics. Automakers continue to specify lighter structures to compensate for battery weight, while consumers favor powered, ventilated, and massage functions that lift average selling prices. Raw-material volatility and stringent safety rules place cost pressure across the value chain, yet Tier-1 suppliers maintain pricing leverage because of their deep integration with vehicle programs. Asia Pacific leads volume demand and technology adoption as Chinese, Indian, and Japanese plants expand capacity for both internal-combustion and electric platforms.

Global Automotive Seats Market Trends and Insights

Rising Global Light-Vehicle Production, Especially SUVs

SUVs reached 54% of global car sales in 2024, increasing seat content per vehicle and lifting demand for reinforced side bolsters, multi-row configurations, and premium trim. Asia Pacific manufacturers benefit as disposable income and urbanization lift SUV penetration. Electric SUVs draw further momentum; 20% of 2023 SUV sales were fully electric, triggering new orders for lightweight frames and integrated thermal management that offset battery mass. The International Energy Agency reports that most SUVs still run on fossil fuel, leaving substantial potential for electrified seat innovation that integrates active cooling, heating, and weight-optimized shells .

Growing Consumer Demand for Powered, Ventilated & Massage Seats

Premium features once limited to luxury brands increasingly appear in mid-segment models. Lear Corporation's ComfortMax platform cuts heating and ventilation response times by 40% and halves assembly complexity, enabling OEM rollouts at scale . Ventilated seats represent the fastest-growing technology slice at 6.12% CAGR because thermal comfort helps EVs preserve driving range. Massage systems now incorporate biometric feedback to reduce occupant stress, transforming seats into wellness hubs and opening recurring revenue through software-enabled upgrades.

Volatile Prices of Leather, Foam & Advanced Polymers

Steel prices more than doubled between 2020 and 2021, and raw-material content per vehicle rose from USD 2,200 to USD 4,125, compressing margins for seat suppliers. Polyurethane foam, covering more than 90% of seat cushions, tracks oil price swings, exposing manufacturers to cost spikes that are difficult to pass through mid-program. Suppliers respond by redesigning cushion geometries to reduce foam volume and by qualifying recycled polymer blends.

Other drivers and restraints analyzed in the detailed report include:

- Automaker Push for Lightweight Seats to Meet CO2 Targets

- Electrified Skateboard Platforms Enabling Flexible Cabin Layouts

- Stringent Safety & Homologation Testing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic leather held 48.20% of the automotive seat market share in 2025 and is projected to grow at a 5.35% CAGR, underscoring its dual appeal of affordability and premium look. Original-equipment programs value their consistent grain, stain resistance, and simplified cleaning, which lowers warranty claims in fleet service. Fabric remains entrenched in entry models, whereas genuine leather persists at the top end but faces sustainability concerns and sourcing volatility. Natural fibers such as flax and hemp enter seat backs and cushion reinforcements as OEMs pursue circular materials, but price premiums still limit volume deployment.

Toyota's SofTex trim produces 85% lower CO2 during manufacture than genuine leather, helping the company align with fleet-average emissions goals. Continental and Magna prototype bio-foam pads that ease recycling by eliminating mixed material adhesives. Such developments signal a shift toward mono-material cushions designed for straightforward disassembly at vehicle end-of-life to meet European circular-economy directives.

Manual adjusters still anchor 57.80% of global share in 2025, reflecting cost sensitivity in emerging markets and base trims. Ventilated variants, however, post a 5.89% CAGR, showing how buyers reward thermal comfort in both hot and cold climates. Heated options remain a staple in North America, while power adjusters form a bridge between economy and luxury lines, offering memory profiles and lumbar modules without complex HVAC integration.

Smart seats that track posture and vital signs are advancing quickly in premium EVs. Hyundai Transys packages low-energy carbon-fiber heaters, dynamic body-care algorithms, and tilt-away walk-in functions within the Kia EV9, proving a mass-production path for fully software-defined comfort. Suppliers are also embedding over-the-air-enabled control units, allowing future features unlock that spread revenue beyond the point of sale.

The Automotive Seat Market Report is Segmented by Material Type (Synthetic Leather, Fabric, and More), Technology (Standard (Manual) Seats, Powered Seats, and More), Sales Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Seat Type (Bench/Split-Bench Seats, Bucket Seats, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific leads with 46.40% revenue and a 3.69% CAGR outlook, fueled by China's electric-vehicle boom, India's fast-growing compact-SUV segment, and Japan's sustained investment in seat electronics. China is forecast to reach 45% EV penetration in new-car sales in 2025, keeping seat suppliers busy with lighter frames and integrated cooling designs. Indian policies that subsidize electric three-wheelers and delivery vans accelerate demand for durable, low-maintenance trim suited to high-usage duty cycles. Japanese innovators such as Toyota Boshoku unveil relaxation seats with swing-chair motion and personalized audio, demonstrating the region's push toward holistic passenger comfort.

Europe focuses on emissions reduction and recyclability. Regulations tighten material traceability and lifecycle carbon accounting, encouraging seats built from bio-based foams and easily separable covers. FORVIA's truck seat platform claims 40% lower CO2 than conventional designs, proving compliance can coexist with driver comfort. North America, characterized by high pickup and SUV share, shows rising standardization of ventilated and heated seats in mid-trim models. Suppliers leverage proximity to Detroit and Mexico fabrication hubs to localize metal stamping and cushion production, reducing logistics risk and meeting US-MCA regional-content rules.

The Middle East, Africa, and South America provide long-run expansion potential. Governments support local assembly to develop automotive ecosystems, creating opportunities for simplified, cost-efficient bench and jump seats that meet rugged-road requirements. Fleet purchases in ride-hailing and mini-bus sectors open demand for easy-clean synthetic leather and quick-swap seat modules that preserve uptime in environments with limited-service infrastructure.

- Adient PLC

- Lear Corporation

- Forvia SE

- Toyota Boshoku Corporation

- Magna International Inc.

- NHK Spring Co. Ltd

- Recaro Holding GmbH

- TS Tech Co. Ltd

- Tachi-S Co. Ltd

- Yanfeng Seating

- Hyundai Transys

- Gentherm Inc.

- Martur Fompak

- Grammer AG

- Freedman Seating

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global light-vehicle production, especially SUVs

- 4.2.2 Growing consumer demand for powered, ventilated & massage seats

- 4.2.3 Automaker push for lightweight seats to meet CO2 targets

- 4.2.4 Electrified skateboard platforms enabling flexible cabin layouts

- 4.2.5 Mobility-as-a-Service fleets needing easy-clean, high-durability trim

- 4.2.6 AI-driven occupant-monitoring systems requiring smart sensor-laden seats

- 4.3 Market Restraints

- 4.3.1 Volatile prices of leather, foam & advanced polymers

- 4.3.2 Stringent safety & homologation testing costs

- 4.3.3 Slow refresh cycles for seat architectures at legacy OEMs

- 4.3.4 Rise of alternative comfort systems reducing demand for premium seats

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Material Type

- 5.1.1 Synthetic Leather

- 5.1.2 Genuine Leather

- 5.1.3 Fabric

- 5.1.4 Natural Fiber and Others

- 5.2 By Technology

- 5.2.1 Standard (Manual) Seats

- 5.2.2 Powered Seats

- 5.2.3 Ventilated Seats

- 5.2.4 Heated Seats

- 5.2.5 Massage Seats

- 5.2.6 Smart / AI-Integrated Seats

- 5.3 By Sales Channel

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.4.4 Two-Wheelers and Three-Wheelers

- 5.5 By Seat Type

- 5.5.1 Bench / Split-Bench Seats

- 5.5.2 Bucket Seats

- 5.5.3 Captain / Individual Seats

- 5.5.4 Child Safety Seats

- 5.5.5 Folding / Jump Seats

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Adient PLC

- 6.4.2 Lear Corporation

- 6.4.3 Forvia SE

- 6.4.4 Toyota Boshoku Corporation

- 6.4.5 Magna International Inc.

- 6.4.6 NHK Spring Co. Ltd

- 6.4.7 Recaro Holding GmbH

- 6.4.8 TS Tech Co. Ltd

- 6.4.9 Tachi-S Co. Ltd

- 6.4.10 Yanfeng Seating

- 6.4.11 Hyundai Transys

- 6.4.12 Gentherm Inc.

- 6.4.13 Martur Fompak

- 6.4.14 Grammer AG

- 6.4.15 Freedman Seating

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment